For years, discussions about Russia’s LNG future have focused on liquefaction capacity. How many trains could be built? How quickly could new projects come online? Could Russia achieve its ambition of becoming one of the world’s largest LNG exporters?

Today, those questions remain relevant, but they are no longer the most important ones.

Russia’s ability to increase LNG exports is increasingly determined not by liquefaction capacity, but by the logistical and technological constraints that connect liquefaction plants to end-users. In other words, the bottleneck has shifted downstream.

China adopted a new gas storage policy in 2018, mandating minimum stock levels for market participants. The government requires gas suppliers, urban gas distributors, and local governments to have storage capacity equal to 10%, 5%, and 3 days of their annual sales/demand. In 2021, the government issued an implementation plan to accelerate the construction of storage capacity (both underground gas storage (UGS) and liquefied natural gas (LNG) reserves). The plan requires that the total gas storage capacity reaches 55 billion cubic meters (bcm) to 60 bcm in 2025, representing around 13% of the expected natural gas demand. In addition, since the global energy crisis, the new watchword has been to “store as much as possible”. These policies have triggered massive development in gas storage, both in UGS and LNG storage tanks.

In an era marked by fluctuating energy markets and geopolitical tensions, the importance of underground gas storage (UGS) has never been more pronounced. As the backbone of global gas security, UGS facilities play a critical role in balancing supply and demand, mitigating price volatility, and ensuring a stable energy supply during peak consumption periods. The recent global gas crisis has thrust UGS into the spotlight, prompting accelerated growth and renewed investment in this vital infrastructure.

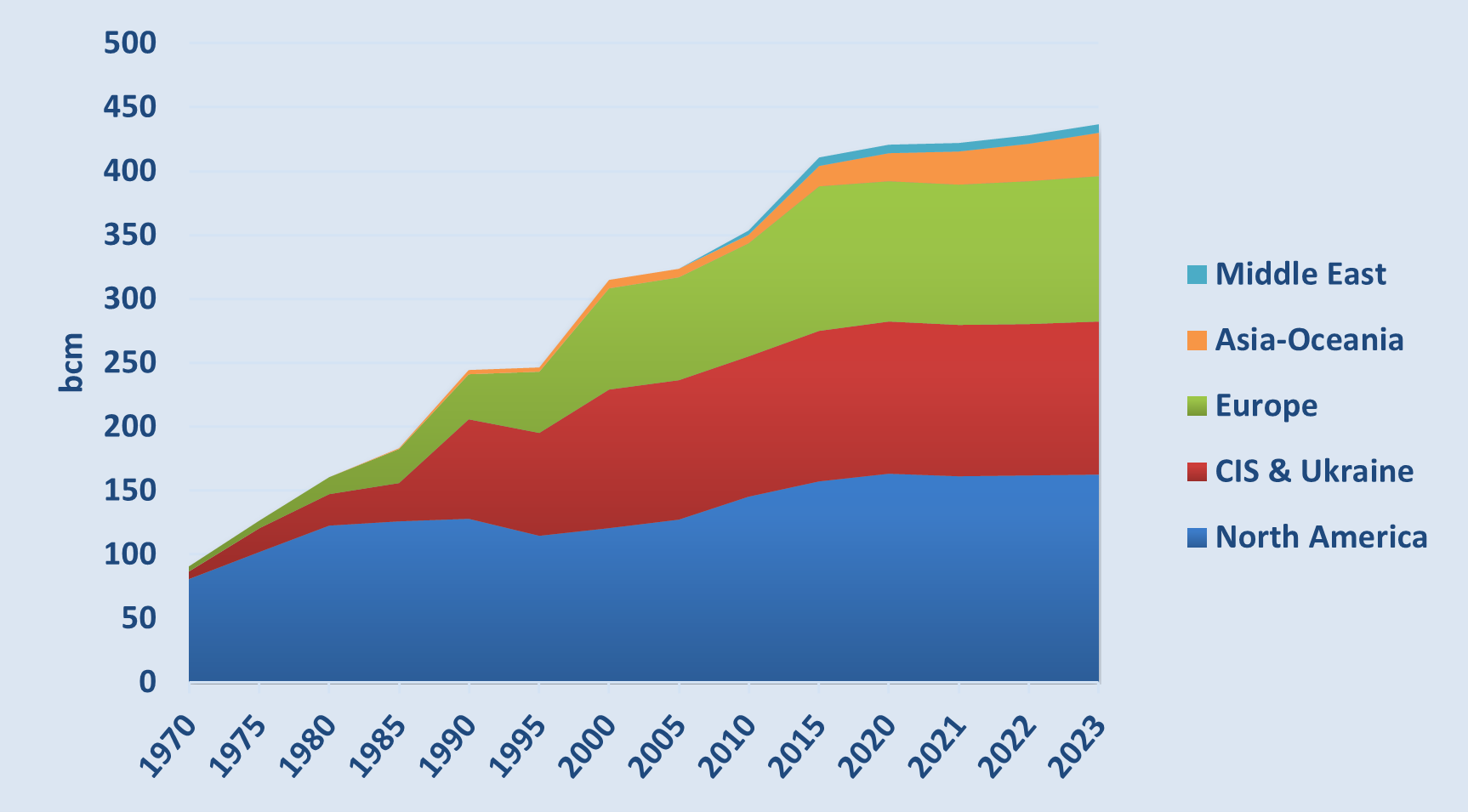

Accelerated Growth of Underground Gas Storage

By the end of 2023, the global working gas capacity of UGS reached 437 billion cubic meters (bcm), a 2% year-on-year increase—the largest since 2015. This surge is primarily due to significant capacity expansions in China, with additional contributions from Europe, Kazakhstan, and Canada. The number of operational UGS facilities globally stood at 681, with China commissioning five new facilities and Saudi Arabia adding its first. The global peak withdrawal rate also increased by 1.6% to 7,516 million cubic meters per day (mcm/d).

Evolution of Global Working Gas Capacity (2023-2024)

Source: CEDIGAZ – Country indicators database, UGS database