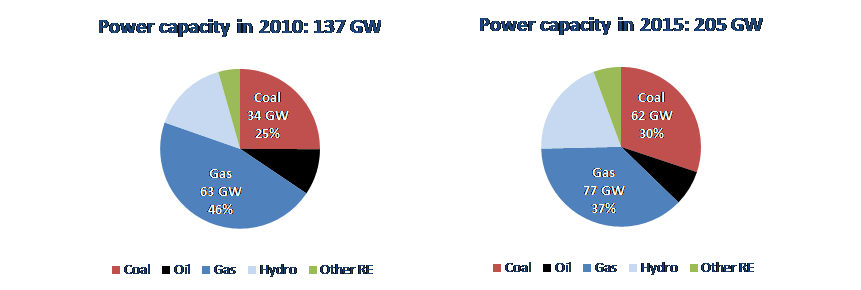

Today, Southeast Asia is again in front of great changes in its energy mix. To meet surging demand, the region must secure a reliable and affordable energy supply. It must also limit the environmental pressures associated with energy consumption. The power sector is fundamental to these changes. Driven by rapid economic growth, demographic and urbanization trends, and the extension of access to modern electricity to larger segments of rural populations, electricity demand is expected to almost triple by 2040.  While natural gas still dominates the regional electricity mix, a shift to coal has been observed since the end of the 2000s driven by the availability of coal in the region and its lower cost than competing fuels. In the short to medium term, this trend is going to continue: there are around 35 GW of coal-based capacity under construction in the region, most of them to be completed by 2020. In addition, there is a huge number of permitted and announced coal-fired power plants in the pipeline, which means that the dominance of coal may continue well after 2020. In the World Energy Outlook 2016 of the International Energy Agency (New Policies Scenario), coal becomes the first source of electricity generation by 2040, despite the increase in electricity generation from renewables. In contrast, the contribution of gas to electricity generation falls by 2040.

While natural gas still dominates the regional electricity mix, a shift to coal has been observed since the end of the 2000s driven by the availability of coal in the region and its lower cost than competing fuels. In the short to medium term, this trend is going to continue: there are around 35 GW of coal-based capacity under construction in the region, most of them to be completed by 2020. In addition, there is a huge number of permitted and announced coal-fired power plants in the pipeline, which means that the dominance of coal may continue well after 2020. In the World Energy Outlook 2016 of the International Energy Agency (New Policies Scenario), coal becomes the first source of electricity generation by 2040, despite the increase in electricity generation from renewables. In contrast, the contribution of gas to electricity generation falls by 2040.

Energy Transition - Page 4

Natural Gas Will Play a Growing Role in a Gradually Decarbonising Energy System But Strong Political Action Is Currently Needed To Promote Coal-To-Gas Switching Worldwide

CEDIGAZ, the International Association for Natural Gas Information, has just released its « Medium and Long Term Natural Gas Outlook 2016 ». This scenario, which incorporates key objectives of current and also planned national energy policies, highlights the growing role of natural gas as a bridge fuel towards a long-term increasingly renewable-based, efficient and sustainable energy system. Given the vast low-cost coal resources, the future expansion of natural gas in the global energy mix will be driven by the implementation of energy and environmental policies aiming to shift away from coal and oil to cleaner fuels within the context of a gradually decarbonising electricity system. In this scenario, the future global natural gas expansion is supported by strong supply growth, particularly of unconventional gas and LNG, in a context of rising prices as energy markets re-balance. CEDIGAZ Scenario’s trajectory is on a 3°C path, with energy-related CO2 emissions increasing by 0.3%/year on average, reaching almost 35 Gt over the 2030-2035 period.

With the first deliveries of Liquefied Natural Gas (LNG) from the US, let’s take a look at the fast changing energy landscape

US shale gas: the first of five revolutions at the beginning of the XXI century

Three revolutions on the supply side: US shale gas, US shale oil and worldwide renewable

The US shale gas revolution is only the first (and most documented) of three revolutions that happened since the beginning of this century on the supply side. The world has changed thanks to the US shale revolutions (gas first and then oil) and a global quest for renewable. Those revolutions took over a decade but will shape the XXI century. Australia followed producing unconventional gas and is now also exporting it. It should take some time for unconventional oil and gas production to materialize in other places where the resource is available[1] (Argentina, Canada, China, Mexico, Russia, South Africa, etc.) but the US shale revolutions should be exported in a few other countries.