Low storage inventories, combined with robust winter demand in both Asia and Europe kept spot prices relatively high in the first quarter 2021.

In the first half of January, Asian and European spot prices spiked to all-time highs as extremely cold weather coincided with tight supply. The Northeast Asian spot price peaked at $30/MBtu by mid-January, opening the widest premiums on record.

European and Asian spot prices retreated in the second half of January as buying focus shifted to the March and April shoulder months. Moreover, temperatures had warmed and nuclear availability improved in Japan, while supplies were creeping up in Asia.

The global oil and gas markets are going through an extraordinary period.

Crude oil and natural gas prices have fallen significantly since the beginning of 2020 to reach historically low levels at the end of March.

Before the spread of the 2019 novel coronavirus disease (COVID-19), spot gas prices were already at seasonal lows due to LNG oversupply, an unseasonably mild winter in the northern hemisphere, economic turmoil (trade war between the United States and China) and renewed confidence in future pipeline gas supply in Europe.

China’s gas demand slowed down at the start of the year as the coronavirus outbreak disrupted industrial output. This downturn has gradually compounded the LNG glut on the global spot market and has accentuated the decline in spot gas prices.

From mid-March, the decline in spot gas prices has been further accelerated by the impacts of the lockdowns which have ramped up around the world.

The impact of the recent slump in oil prices on oil-indexed LNG prices will not be seen until late in the April-June quarter because of the time lag between crude oil and LNG prices under long term contracts.

The COVID-19 has already had a devastating impact on global gas demand, which could continue for some time as the pandemic spreads across continents.

A number of LNG projects have already faced headwinds amid the coronavirus outbreak and current low oil prices environment. However, as of today, these projects’ delays do not alter Cedigaz’ view for a well-supplied LNG market by 2025/2026.

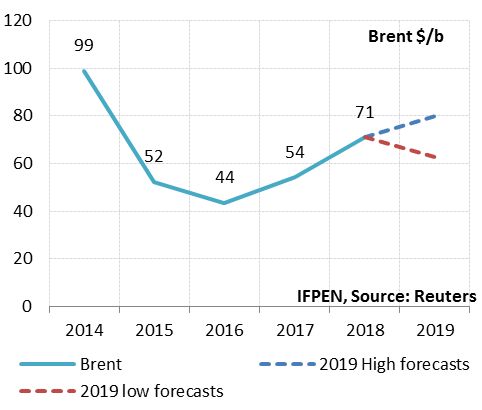

Brent: between $60 and $80/b in 2019 (2018: $71/b)

The oil price oscillated between $50 and $86/b in 2018, averaging $71/b (+31% compared to 2017). The volatility observed in 2018 was due in large part to uncertainty about supply and economic growth, but also to the U.S. sanctions against Iran. Initially announced as being extremely severe, the embargo was softened at the last minute by the American president when he realized the likely consequences of a rise in the price of oil products.

For 2019, the average Brent price is expected to be in the $60 to 80/b range. These expectations account for different scenarios for factors such as economic growth, the Iran embargo, OPEC’s management of supply and U.S. production.

NBP: €19-23/MWh in 2019 (€23.3/MWh; $8.1/MBtu in 2018)

Based on forward prices and expected oil prices, the average UK NBP price for 2019 could fall between €19 and 23/MWh ($6.5-7.8/MBtu) compared to €23,3/MWh ($8.1/MBtu) in 2018, representing a potential decrease of between 1 and 18%.