NBP: down next summer

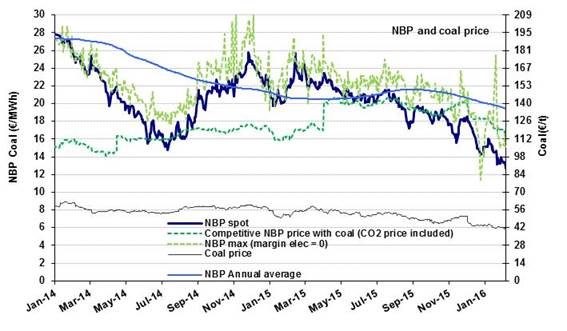

In the first few days of March, the NBP was quoting at about €13/MWh ($4.2/MBtu), close to the previous month’s average. These levels are extremely low. Not since April 2010 (euro prices) and October 2009 (dollar prices) have such low numbers been recorded. The monthly average hit rock bottom at €7.6/MWh ($3.3/MBtu) in September 2009. The markets are not anticipating prices to drop that much next summer, but a series of decreases from the current levels to the vicinity of €11.8/MWh ($3.9/MBtu). For next winter, the NBP is expected to reach $14-15/MWh ($4.6-5.0/MBtu), in line with contracts 100% indexed to oil. This convergence indicates that the market deems $4.6-5/MBtu to be the lowest equilibrium threshold tenable in an average winter.

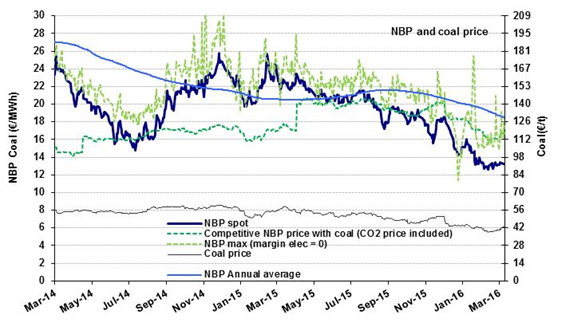

In the first few days of March, the NBP was quoting at about €13/MWh ($4.2/MBtu), close to the previous month’s average. These levels are extremely low. Not since April 2010 (euro prices) and October 2009 (dollar prices) have such low numbers been recorded. The monthly average hit rock bottom at €7.6/MWh ($3.3/MBtu) in September 2009. The markets are not anticipating prices to drop that much next summer, but a series of decreases from the current levels to the vicinity of €11.8/MWh ($3.9/MBtu). For next winter, the NBP is expected to reach $14-15/MWh ($4.6-5.0/MBtu), in line with contracts 100% indexed to oil. This convergence indicates that the market deems $4.6-5/MBtu to be the lowest equilibrium threshold tenable in an average winter.