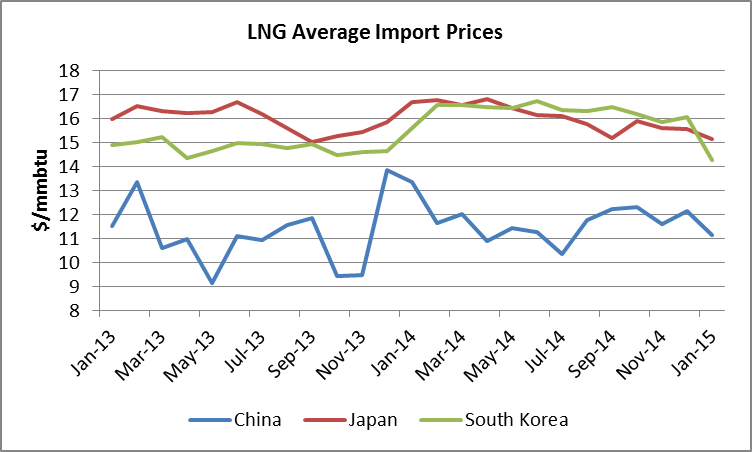

In January 2015, LNG imports in Japan, South Korea and China grew by 0.8% compared to December 2014. Imports reached 14.7 million tons which is though 3.9% lower than January 2014 levels. January showed the first impacts of decreasing oil prices on LNG prices, as oil-linked contracts usually include a six-month lag. In Japan, the average import price decreased to its lowest point since September 2013 at $15.15/mmbtu in January, while it averaged $16.14/mmbtu in 2014. South Korean price dropped sharply, from $16.07/mmbtu in December (and $16.31/mmbtu on average in 2014) to $14.27/mmbtu in January.

Asia: overall year-on-year stagnation amid weaker growth in China

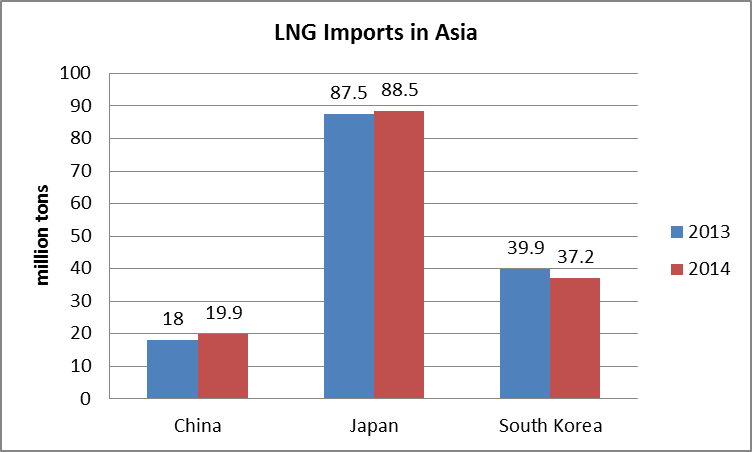

In Asia, the volume of LNG imported by the three largest consumers – Japan, South Korea and China – has stagnated overall, from 145.4 million tons in 2013 to 145.6 million tons in 2014. Japan imported 88.5 million tons in 2014 versus 87.5 million tons in the previous year, while South Korean imports decreased by 6.8% down to 37.2 million tons due to the restart of some nuclear plants, strong competition from coal and mild temperatures. Chinese imports growth has markedly decelerated to 10.4% versus 23% in 2013 and 20.3% in 2012.

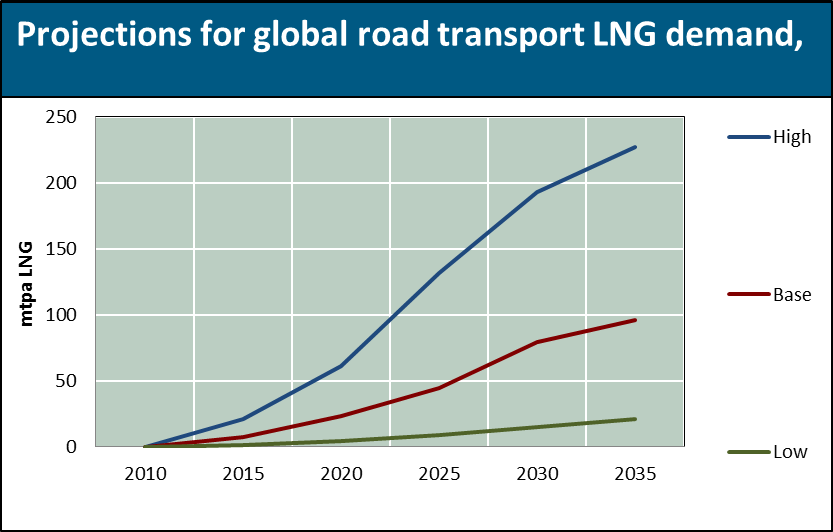

According to a new report by CEDIGAZ, the International Center for Natural Gas Information, LNG as a fuel will capture a significant market share in the transport sector by 2035. The greatest potential is seen in road transport, were annual demand is projected to reach 96 million tons per year (mtpa) in CEDIGAZ’ base scenario while demand in the marine sector could grow to an estimated 77 mtpa. The rail sector could add another 6 mtpa to global demand. However, the development of LNG as a transport fuel faces a number of challenges, and will have to go hand in hand with the development of fuelling infrastructure.

Fuel cost differentials will drive the growth in trucking sector

Use of LNG in land transport will be largely limited to heavy duty vehicles (HDV) and will essentially be driven by the difference between the price of diesel and that of LNG. In contrast with the marine sector, environmental legislation is unlikely to play a major role in triggering the adoption of LNG as a fuel for land transportation, as traditional fuels and technologies will be able to comply with the gradual tightening of emissions standards. However, the cost advantage of LNG relative to diesel currently provides a strong economic incentive in the trucking industry. In its base scenario, CEDIGAZ projects a worldwide demand of 45 mtpa in 2025 growing to 96 mtpa in 2035, with China representing almost half the global market. China has several features that combine to make it a prime candidate for the development of LNG in the road sector. The country has the world’s largest inland goods transport market and has already developed an extensive LNG supply infrastructure, initially as a means of transporting gas from remote fields or to consumers who were not connected to the pipeline supply network. With at least 100,000 LNG vehicles and 1,100 refuelling stations at the end of 2013, China already has a head start over the rest of the world in this nascent market. However, gas price reform in China may slow LNG growth there. LNG should also carve out a significant market share in the US, Europe and the rest of Asia.

In January 2015, LNG imports in Japan, South Korea and China grew by 0.8% compared to December 2014. Imports reached 14.7 million tons which is though 3.9% lower than January 2014 levels. January showed the first impacts of decreasing oil prices on LNG prices, as oil-linked contracts usually include a six-month lag. In Japan, the average import price decreased to its lowest point since September 2013 at $15.15/mmbtu in January, while it averaged $16.14/mmbtu in 2014. South Korean price dropped sharply, from $16.07/mmbtu in December (and $16.31/mmbtu on average in 2014) to $14.27/mmbtu in January.

In January 2015, LNG imports in Japan, South Korea and China grew by 0.8% compared to December 2014. Imports reached 14.7 million tons which is though 3.9% lower than January 2014 levels. January showed the first impacts of decreasing oil prices on LNG prices, as oil-linked contracts usually include a six-month lag. In Japan, the average import price decreased to its lowest point since September 2013 at $15.15/mmbtu in January, while it averaged $16.14/mmbtu in 2014. South Korean price dropped sharply, from $16.07/mmbtu in December (and $16.31/mmbtu on average in 2014) to $14.27/mmbtu in January.