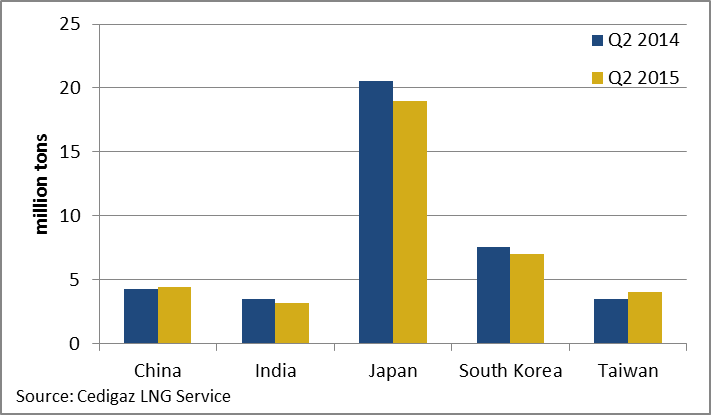

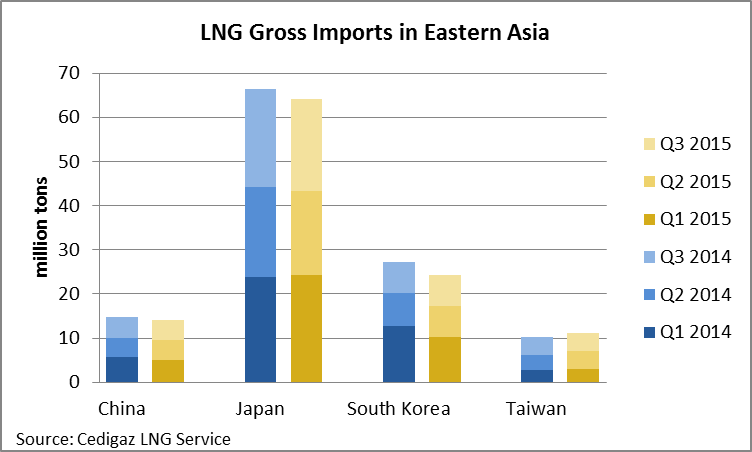

Eastern Asian LNG imports dropped by 4.2% year-on-year in Q3 2015

In Q3 2015, LNG gross imports dropped by 4.2 % year-on-year in Eastern Asia. In Japan, South Korea, China and Taiwan, LNG imports declined by 1.6 million tons from 38.1 million tons in Q3 2014 to 36.5 million tons in Q3 2015. In Japan, LNG imports were cut by 5.6% down to 20.9 million tons, as inventories were high and demand from the power sector weaker than a year ago. The latter was explained by lower than average temperatures in July and September, reducing the need for air-conditioning, and the restart of Sendai’s first reactor, even though it accounted for only 0.5% of the electricity generated by the 10 major producers.

In China, LNG imports decreased by 3.5% year-on-year in Q3, from 4.8 million tons in Q3 2014 to 4.6 million tons in Q3 2015. Over the first nine months of the year, LNG imports reached 14.1 million tons compared to 14.7 million tons over the same period last year (-3.7% year-on-year), while imports by pipeline grew to 11.7 bcm (+68.3% year-on-year in the first nine months). While high wholesale gas prices reduced the competitiveness of natural gas in the first half of the year and limited the growth of demand, LNG demand in recent months was affected by uncertainties over these prices, which could be cut by the government soon. Gas distributors seem to have anticipated such a drop and held back stock building to avoid a devaluation of their inventories.

In Taiwan, LNG imports dwindled by 5.4% year-on-year in Q3 2015, to 3.9 million tons. Despite the drop, Taiwanese imports grew by 7.1% year-on-year in the first nine months of the year, from 10.3 million tons to 11 million tons.

After two quarters of decrease, LNG imports were flat in Q3 2015 in South Korea. The second largest importer in the world received 7 million tons in Q3 2015 against 6.98 million tons in Q3 2014. In August, the country imported 15.6% less LNG than in August 2014, but higher demand during this same month from the power sector caused by above average temperatures contributed to increase imports in September (+13.3% year-on-year).

The drop in LNG average import prices temporary on hold

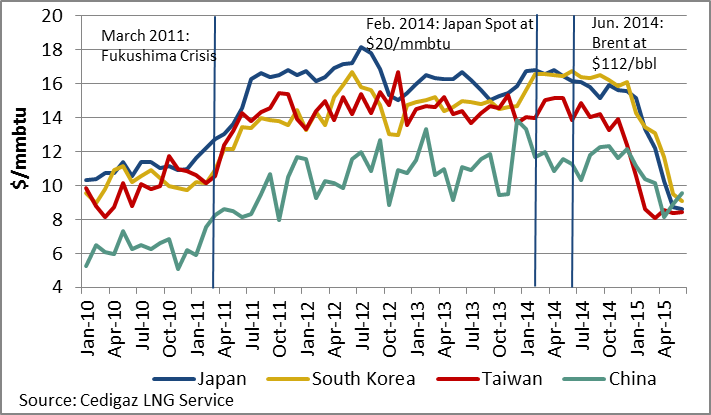

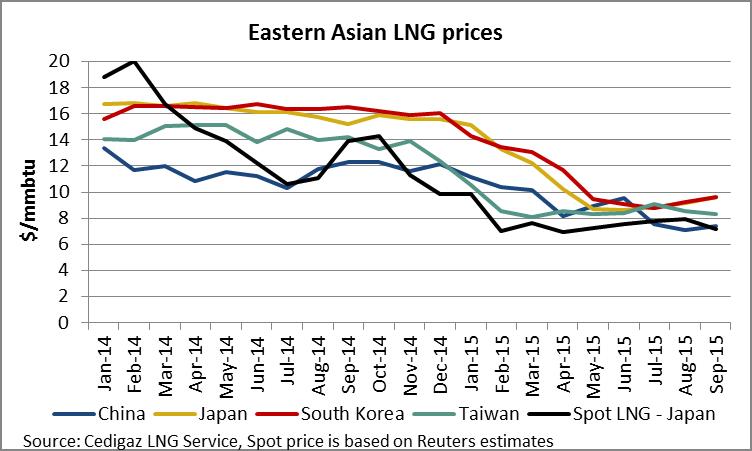

In Eastern Asian countries, the continuous drop in LNG prices was somehow put on hold over Q3 2015 as a consequence of the slight rebound in crude oil prices which occurred in May and June. In Japan, where long-term contracts prices are typically indexed on JCC price and include a 3-month lag, average import price grew from $8.61/mmbtu in June to $9.65/mmbtu in September. Similarly, average import price in South Korea grew from $9.11/mmbtu to $9.61 over the same period. In China and Taiwan, the higher share of spot purchases and the use of different prices formula for long-term contracts explain the different trends.

On the spot market, LNG price decreased over the summer. While Japan LNG spot price averaged $7.58/mmbtu in June, it increased in July and August when it peaked at $7.97/mmbtu, its highest level since January 2015. However, low demand in Asia and the ramp-up of new facilities in Australia and Indonesia drove spot prices down to $7.21/mmbtu in September.

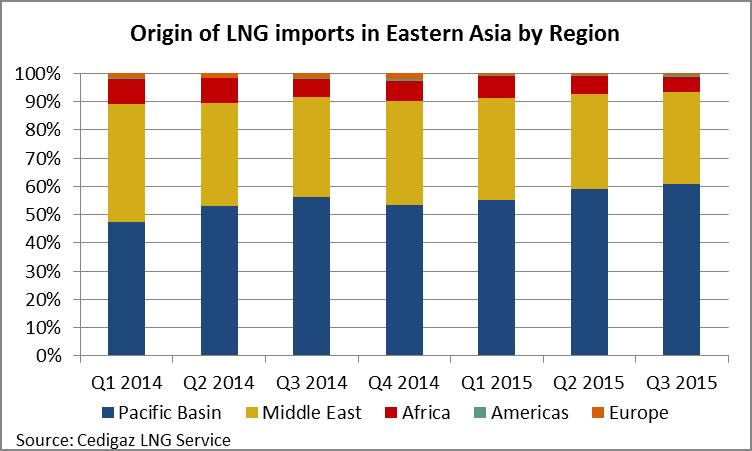

Market share of Pacific Basin producers above 60%

In the third quarter of the year, the share of LNG produced in the Pacific Basin region (including Asia Oceania and Russia) continued to grow and reached 60.9% against 59% in Q2 2015 and an average of 52.4% during the whole year 2014. On the opposite, the share of supply from the Middle East decreased to 32.4% in Q3 2015 against 33.8% in Q2 2015 and a 37.8% average in 2014.

Such a trend, which started in 2013, intensified in 2015 as consequence of the ramp up of new regional producers and diminished or diverted production from the Middle East. In the first nine months of 2015, Eastern Asian countries imported 19.1 million tons of LNG from Australia against 17.6 million tons over the same period in 2014 (+8.8%). Similarly, imports from Papua New Guinea reached 5.3 million tons from January to September 2015 (+199.7% year-on-year).

On the contrary, exports from the Middle East to these four Asian countries have reduced for various reasons. In Yemen, the collapse of LNG exports from 3.6 million tons in the first nine months of 2014 to 1 million tons in 2015 is due to the shut down of the Yemen LNG plant in February. As for Qatar, supply to Eastern Asia dropped by 8.4% year-on-year from January to September as a consequence of the diversion of flexible LNG to Europe and exports to new importing countries (Egypt, Pakistan, Jordan). Imports from the United Arab Emirates decreased because of maintenance work at the Adgas plant in March 2015. Last, but not least, imports from Oman dropped by 15% from 5.6 million tons in the first nine months of 2014 to 4.8 million in the first nine months of 2015 as growing domestic demand for natural gas (+5.5% or 1.55 Bcm over the period) reduced available feedgas for the Oman LNG plant.

In the first quarter of 2015, first estimates of global LNG market announced changing dynamics compared to the previous year. Second quarter estimates confirm this trend as the Asian market remains soft with lower demand and increased output in the Pacific Basin. In Europe, Q2 saw net imports grow as gross imports increased and re-exports collapsed. New players such Egypt, Pakistan and Jordan are now integrated in the market while in the United States, Q2 seemed to mark the beginning of the end of the LNG rush. Overall, first outlook for 2015 sees a 2.1% to 2.5% growth year-on-year of the global LNG market to 240-241 million tons.

The Asian market remains soft

In Q1 2015, following the collapse of oil prices and under the influence of softening market conditions, LNG average import prices declined significantly in Asia. In Japan, prices plummeted by 19.4% from January to March and in South Korea, prices fell by 8.4% over the same period.

In the course of Q2, prices kept dwindling but the drop substantially slowed down from May to June as the collapse in oil prices had eased off during the previous months. In June 2015, prices stood at $8.61/mmbtu in Japan, $9.11/mmbtu in South Korea and $9.57/mmbtu in China. From January to June, prices fell respectively 43.2%, 36.2% and 14.2% in these three countries.

LNG Average Import Prices in Asia

Considering the traditional weight of oil-indexed volumes in the imports of Asian largest buyers, the recent trends of oil prices explain most of the evolution of average import prices in Asia. While spot or short-term based deliveries represented about 29% of imports in Japan, 24% in South Korea, 21% in China and 19% in Taiwan in 2014 according to GIIGNL, these volumes are likely to have decreased in the first half of 2015, according to market sources. In May, the Japanese Ministry of Economy could not publish any LNG spot price as its methodology requires at least two trades to compute an average and it was reported that Kogas, South Korean major importer, stayed on the spot market sidelines in the first half of the year.

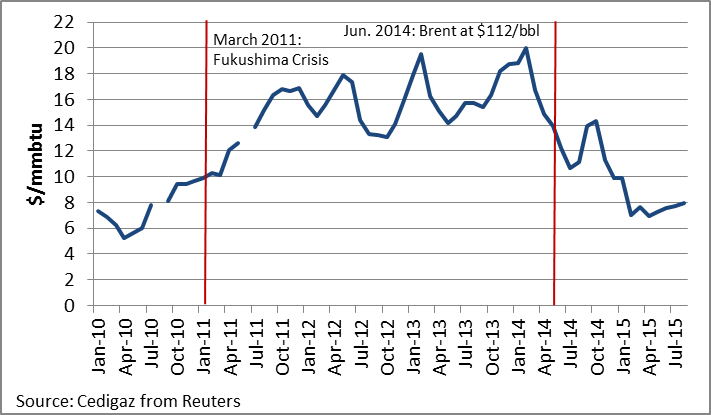

As a consequence of softer demand and increased available supply in the Pacific Basin, spot prices stayed low in Q2 2015 in Asia. According to Reuters’ assessments, the price of LNG delivered to Japan on a spot basis averaged $7.3/mmbtu, against $8/mmbtu in Q1 2015. In June, Japan spot price stood at the same level as it was in March 2015 at around $7.6/mmbtu. In August 2015, spot price rose to $8/mmbtu but it is likely to stay below $7.5/mmbtu on average in September 2015.

Spot LNG Price in Japan

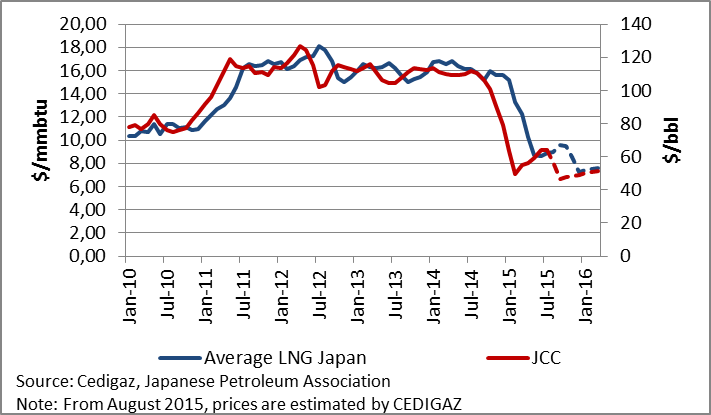

In Japan, assuming that most of the contracts include a 3-months lag with JCC price, long-term prices are expected to fall until December. Based on a typical 14.5% slope plus a fixed cost of $0.5/mmbtu and recent history in JCC and crude oil prices, long-term price is likely to decrease to $9.8/mmbtu in October and $7.2/mmbtu in December. Similarly, assuming that spot LNG will account for about 10% of LNG imports in Q4 2015 at an average price of $7.4/mmbtu, average import price in Japan could reach $8.5/mmbtu on average in Q4 2015.

Japan LNG Import Price vs. JCC Price

On the demand side, LNG purchases of the top-3 buyers in the region (Japan, South Korea and China) decreased by 6.2% year-on-year in the second quarter of 2015, from 32.4 million tons to 30.3 million tons. The drop was pulled by a 7.5% decrease in Japan (-1.5 million tons) while all nuclear plants were still offline. After a peak in imports in 2014, such a decrease can be explained by warmer than average temperatures in the winter which left stocks high, and below average temperatures at the beginning of the summer which resulted in lower demand from the power sector.In the first half of 2015, Japan’s imports decreased by 2.2% year-on-year.

The second largest decrease among Asian importers occurred in South Korea, where imports had already collapsed by 19% year-on-year in Q1. In Q2 2015, LNG imports dropped by 7.5%, from 7.5 million tons to 7 million tons year-on-year, due to above average temperatures which reduced demand in the domestic and commercial sector. The Asian economic turmoil affecting Korean industrial production and lower demand from the power sector also contributed to lower imports. The consumption of LNG by the power sector fell from 4.1 million tons in Q1 2014 to 2.4 million tons in Q1 2015, while coal consumption increased by 7.8%. Overall, the share of electricity generated by combined cycle plants in the electricity mix fell from 22.8% to 19.8% in the first five months of the year.

In China, after an 8.6% decline year-on-year in Q1 2015, LNG imports grew slightly by 2.5% year-on-year in Q2 2015, pulled by higher imports in April (+12.9%). In the first half of 2015, Chinese LNG imports decreased by 3.8% from 9.9 million tons to 9.5 million tons as a consequence of the slowdown of natural gas demand growth. While domestic natural gas output grew by 3% year-on-year in the first eight months of the year (against a 6.9% rise for all of 2014 and 11.5% for 2013) and pipeline imports rose by 14.8% year-on-year in the first half of 2015, LNG imports appear to support the brunt of the slowdown in natural gas demand. The drop was caused by the slowdown of the Chinese economy and the loss of competitiveness of natural gas against oil as Beijing did not cut oil-indexed city-gate and wholesale prices until April, which contributed to lower gas demand from industries like glass makers and chemical manufacturers.

LNG Imports by Main Asian Country in Q2 2015

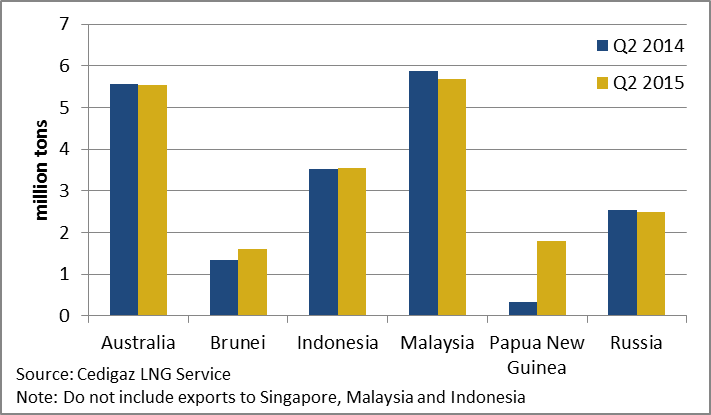

While demand from Asian countries continued to decrease, the available supply from producers in the Pacific Basin slightly increased year-on-year in Q2. Although no newly commissioned plant came on stream during the second quarter, good performance at operating plants enabled total output to increase. Supply growth was mainly driven by Brunei which produced 1.6 million tons (against 1.3 million tons in Q2 2014) and Papua New Guinea whose two 3.45 mmtpa trains have been running slightly above design capacity, producing 1.8 million tons in Q2 2015. In Australia, unplanned outage in May at North West Shelf LNG and a major turnaround at Pluto LNG caused the production to decrease in these two plants to 4.2 million tons in Q2 2015 against a combined output of 4.8 million tons in Q2 2014. The 13.5% decrease was offset by the good performance of the Darwin LNG plant which shipped 15 cargoes over the period and by the ramp up of the first train of QC LNG which shipped 16 cargoes in Q2 2015 against nine cargoes in the first quarter of 2015. In July, BG announced that train 1 was running at plateau, producing about five cargoes per months and that it had started operations at train 2.

Intra-regional exports in the Pacific Basin in Q2 2015

In the second half of 2015, spot LNG prices in Asia are expected to remain low because of an overall depressed regional demand and growing supply from the Pacific Basin. On the demand side, the drop in imports from South Korea, which had withdrawn from the spot market in 2015 may halt. As of September 2015, Kogas was taking delivery of annual contracted volumes without delaying as it previously did. In May 2015, natural gas stocks stood at 2.6 million tons, just above the level of May 2013 (2.4 million tons) but 19.9% below the level of May 2014 (3.3 million tons) and Kogas will need to replenish LNG stocks. In Japan, the restart of the first reactor of Kyushu’s Sendai nuclear plant (890MW) in September and the planned restart of Sendai’s reactor number 2 (890 MW) is expected to impact the demand for fuel oil in the coming months rather than LNG demand. The latter could decrease in the winter due to lower needs for power generation as the El Niño phenomenon, which usually brings above than average temperatures, tends to confirm in 2015.

On the production side, the second half of the year will see ramp up of the 2 mmpta Donggi-Senoro, which shipped its first cargo in August and of the second train of QC LNG. Gladstone LNG, which is targeting first shipment in October, is expected to produce five cargoes (0.3 million tons) to be sold on the spot market. The start-up of the first train of Australia Pacific LNG in October could also bring up to seven cargoes on the market while Sabine Pass LNG is expected to start operations in December, but its output is likely to be limited to one cargo in 2015. Overall, the commissioning of new plants/trains in H2 2015 is expected to add 2.8 million tons of LNG on the market over the period. In 2015, assuming there will be no major decrease in production of existing plants (excluding Yemen LNG), the global net LNG supply growth could be limited to 5 to 6 million tons (+2.1% to 2.5% year-on-year).

European rebound confirmed: net LNG imports grew by 16.8% year-on-year in Q2

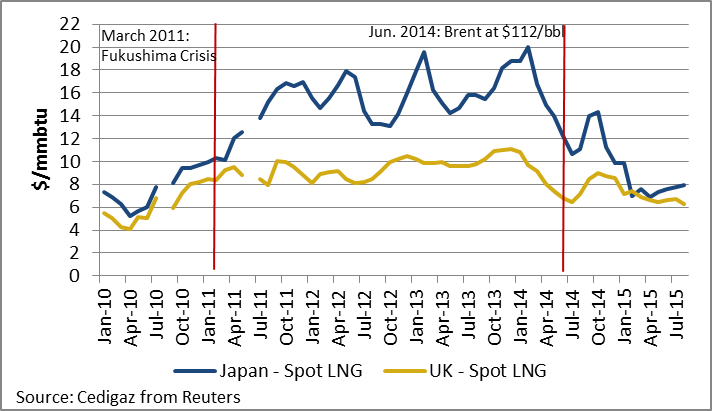

In Q1 2015, the softening of market conditions in Asia caused the gap between Asian and European LNG spot prices to narrow sharply, down to $0.83/mmbtu on average. In Q2 2015, the drop in the so-called Asian premium continued, oscillating between $1.45/mmbtu and $0.01/mmbtu and averaging $0.72/mmbtu. Overall, the Asian premium was at $0.77/mmbtu in H1 2015 against $7.4/mmbtu in H1 2014 which enabled European market to recover its attractiveness and absorb the diverted flexible LNG left available by Asian buyers.

UK Spot LNG vs. Japan Spot LNG

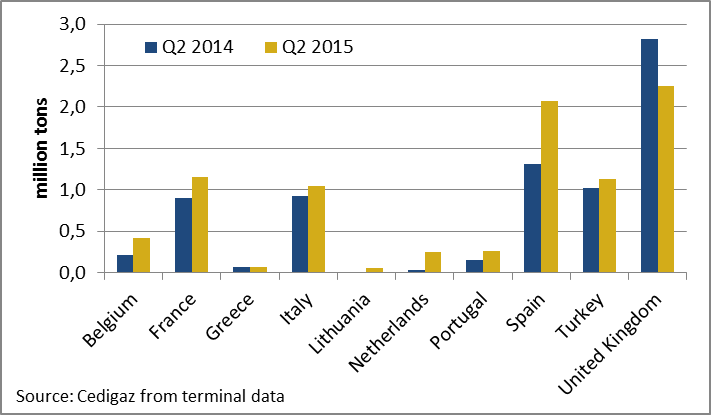

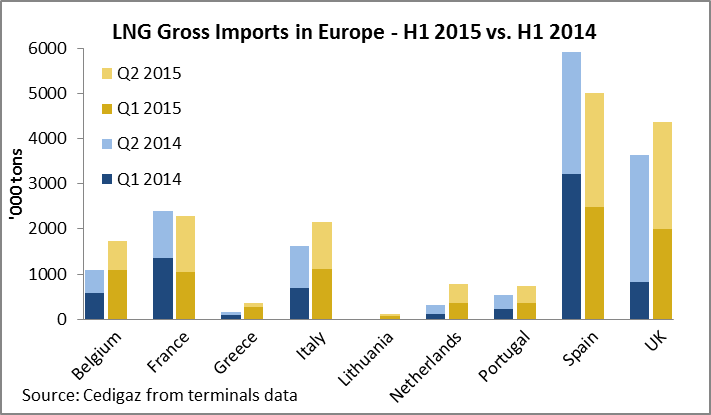

In Q2 2015, Europe saw a slowdown in the LNG imports rebound which started in Q1, even though it was still significant. In the region, LNG net imports grew by 16.8% year-on-year, from 7.46 million tons in Q2 2014 to 8.71 million tons in Q2 2015. Overall, LNG net imports increased by 26.4% in the first six months of 2015 compared to the same period last year. To a lower extent than in Q1, Northwest Europe liquids markets continued to absorb flexible LNG diverted from Asia in Q2 2015: over the period, LNG gross imports grew by 23.5% year-on-year in Belgium and by 123.7% year-on-year in Netherlands, which received 0.15 million tons of LNG from Qatar in Q2 2015, against none in Q2 2014. In the United Kingdom, where gross imports had grown by 143.3% in Q1 year-on-year, the second quarter of 2015 saw a 15.7% decrease, due to lower Qatari volumes. In the second quarter, Qatar had fewer flexible cargoes to be sent to Qatargas’ South Hook terminal in the UK, as demand from new importers (Pakistan, Egypt, Jordan) rose.

In Spain, LNG net imports rebounded significantly, from 1.31 million tons in Q2 2014 to 2.07 million tons in Q2 2015 (+57.9%), as reloaded volumes collapsed by 66.4%, from 1.4 million tons to 0.47 million tons and as natural gas consumption was boosted by the power sector. The latter consumed 33.3% more gas in Q1 2015 than in Q1 2014 and 19.4% more in Q2 because of water shortage which reduced the output of hydropower by 32.4% in the first half of 2015. In France, the growth in LNG net imports in Q2 2015 offset the decrease of Q1 so that the country’s net imports decreased by 1.5% year-on-year in H1 2015.

LNG Net Imports in Europe by Country in Q2 2015

In the rest of the world, new players are emerging ; the US LNG rush is coming to an end

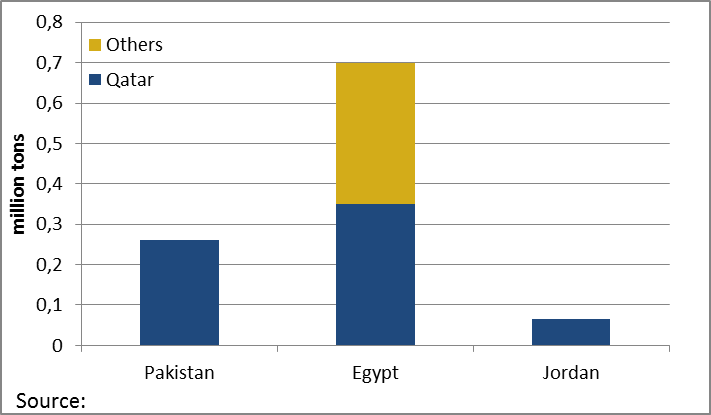

In the rest of the world, the weight of LNG new players has grown over the second quarter of 2015. During the period, the group of three new importers composed of Pakistan, Egypt and Jordan imported about 1 million tons of LNG, including about 0.68 million tons from Qatar, which finds there a new market for its production.

Pakistan, which imported its first LNG cargo in late March, handled four other shipments from Qatar in Q2, raising the total volume of imports to 0.32 million tons since the beginning of operations. Over the period, Egypt also became the first importer of LNG in Africa and received 10 cargoes (about 0.7 million tons), including 5 deliveries from Qatar (about 0.35 million tons). Due to rising domestic demand and lower-than-expected production, Egypt’s needs are high and the country has already ordered a second FSRU to be provided by BW Maritime and which could start receiving LNG in October. The country has announced plans for a third floating regasification unit to be located in Safaga with a targeted start-up in September 2016. In Jordan, Q2 imports were limited to a unique delivery from Qatar in May. After some delays during the commissioning phase, the terminal is now operating well.

LNG Imports in Pakistan, Egypt and Jordan in Q2 2015

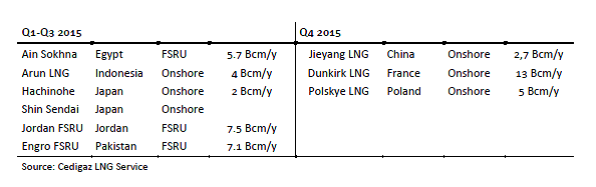

In Indonesia, the former liquefaction plant Arun LNG is now operating as an import terminal and received the commissioning cargo of the Donggi-Senoro LNG plant in early August. Since the beginning of the year, expansion work has been completed in the Chilean Quintero LNG and Spanish Bahía de Bizkaia Gas terminals and Sinopec recently announced its plan to expand the Qingdao terminal by 3 to 3,5 mmtpa of regasification capacity. The latter would take deliveries from Australia Pacific LNG until Guangxi LNG and Tianjin LNG terminals become operational, probably in early 2016. In China, CNOOC’s Jieyang LNG is still under construction and is scheduled to come on stream in late 2015. It was reported than work at CNOOC’s Diefu LNG terminal slowed down and that its commissioning might be delayed by two to three years. In Europe, the Dunkirk LNG and Polskie LNG terminals are on track to receive their first shipment of chilled gas by the end of the year, even though commercial operations are not expected to start until Q1 2016 in Poland. In Uruguay, the contract with the Engie-led consortium to build and operate the GNL del Plata terminal was revoked in September 2015 and the new target for start-up was pushed back to 2017.

Commissioning of Regasification Terminals in the World in 2015On the production side, Q2 2015 was mainly marked by the ramp up of Australian plants. In the Middle East, Yemen LNG declared force majeure in April and evacuated all of its staff after violence surged in the country. Since then, the plant has been shut down and will not re-open as long as the country faces fighting. In Algeria, after a 77-day shut-down for maintenance in Q1 2015, production resumed at the Skikda LNG plant. In Q2 2015, the country exported 2.84 million tons of LNG to Europe, slightly above its Q2 2014 output (2.78 million tons) and 44.6% above the Q1 2015 production.

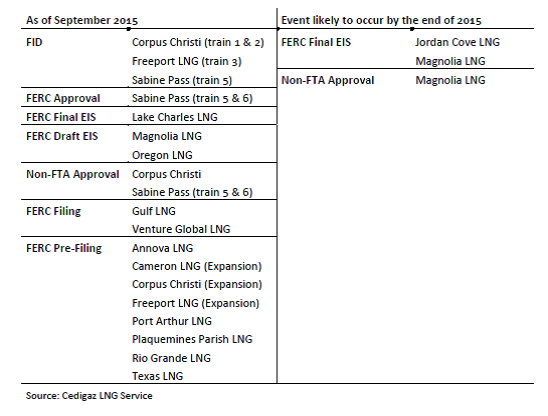

In the United States, the LNG rush is coming to an end as Q2 2015 was the first quarter since Q1 2011 without new project to apply for an export license to the Department of Energy. Corpus Christi LNG requested – and was granted – a license to export an additional 1.41 bcf/d to countries that have a Free-trade agreement with the United States. In Q2 2015, only one new project initiated the pre-filing process to the FERC and two others – Corpus Christi LNG and Freeport LNG – have requested an authorization to expand. Two other projects – Gulf LNG and Venture Global’s Calcasieu Pass – moved forward in the filing process respectively in June and September. In addition to the diminishing number of requests for various permits, the end of the rush was marked by delays in FID schedules (Elba Island LNG, Lake Charles LNG, Golden Pass LNG…) and the first withdrawal, as Excelerate Energy officially halted its project at Lavaca Bay, Texas.

European LNG net imports: + 27.8% year on year in H1 2015

LNG net imports increased significantly to 15.9 million tons in the first half of 2015 against 12.4 million tons in H1 2014 due to more deliveries and less reloads. Gross imports showed a two-digit growth rate or even more in all countries but France and Spain – where they decreased by 5% and 15.3% respectively – thanks to the capacity of liquid markets of Northwest Europe to absorb the LNG left available by Asian buyers. Overall, gross imports grew by 11.9%, mostly driven by imports in Belgium, the Netherlands and the United Kingdom. Together, these three countries received 6.88 million tons of LNG in H1 2015 against 5.04 million tons in H1 2014 (+36.7%), mostly from Qatar. The latter, which is diverting flexible LNG from Asia, exported 9.8 million tons of LNG to Europe in H1 2015 against 7.85 million tons in H1 2014 (+24.9%).

In Q3 2015, LNG gross imports dropped by 4.2 % year-on-year in Eastern Asia. In Japan, South Korea, China and Taiwan, LNG imports declined by 1.6 million tons from 38.1 million tons in Q3 2014 to 36.5 million tons in Q3 2015. In Japan, LNG imports were cut by 5.6% down to 20.9 million tons, as inventories were high and demand from the power sector weaker than a year ago. The latter was explained by lower than average temperatures in July and September, reducing the need for air-conditioning, and the restart of Sendai’s first reactor, even though it accounted for only 0.5% of the electricity generated by the 10 major producers.

In Q3 2015, LNG gross imports dropped by 4.2 % year-on-year in Eastern Asia. In Japan, South Korea, China and Taiwan, LNG imports declined by 1.6 million tons from 38.1 million tons in Q3 2014 to 36.5 million tons in Q3 2015. In Japan, LNG imports were cut by 5.6% down to 20.9 million tons, as inventories were high and demand from the power sector weaker than a year ago. The latter was explained by lower than average temperatures in July and September, reducing the need for air-conditioning, and the restart of Sendai’s first reactor, even though it accounted for only 0.5% of the electricity generated by the 10 major producers.  n countries, the continuous drop in LNG prices was somehow put on hold over Q3 2015 as a consequence of the slight rebound in crude oil prices which occurred in May and June. In Japan, where long-term contracts prices are typically indexed on JCC price and include a 3-month lag, average import price grew from $8.61/mmbtu in June to $9.65/mmbtu in September. Similarly, average import price in South Korea grew from $9.11/mmbtu to $9.61 over the same period. In China and Taiwan, the higher share of spot purchases and the use of different prices formula for long-term contracts explain the different trends.

n countries, the continuous drop in LNG prices was somehow put on hold over Q3 2015 as a consequence of the slight rebound in crude oil prices which occurred in May and June. In Japan, where long-term contracts prices are typically indexed on JCC price and include a 3-month lag, average import price grew from $8.61/mmbtu in June to $9.65/mmbtu in September. Similarly, average import price in South Korea grew from $9.11/mmbtu to $9.61 over the same period. In China and Taiwan, the higher share of spot purchases and the use of different prices formula for long-term contracts explain the different trends. In the third quarter of the year, the share of LNG produced in the Pacific Basin region (including Asia Oceania and Russia) continued to grow and reached 60.9% against 59% in Q2 2015 and an average of 52.4% during the whole year 2014. On the opposite, the share of supply from the Middle East decreased to 32.4% in Q3 2015 against 33.8% in Q2 2015 and a 37.8% average in 2014.

In the third quarter of the year, the share of LNG produced in the Pacific Basin region (including Asia Oceania and Russia) continued to grow and reached 60.9% against 59% in Q2 2015 and an average of 52.4% during the whole year 2014. On the opposite, the share of supply from the Middle East decreased to 32.4% in Q3 2015 against 33.8% in Q2 2015 and a 37.8% average in 2014.