Thanks to India’s rising economy and population, the country’s outlook for growth in energy demand is robust. The role of gas in the country’s energy mix, however, is hard to determine. Today, India’s primary energy mix is dominated by coal and oil. The role of natural gas is limited: only 6% in 2016. But the government wants to make India a gas-based economy and raise the share of natural gas in the energy mix to 15% by 2022, although the timing remains uncertain. This paper analyses gas demand trends in India by 2025-30 and draws on two reports recently published by the Oxford Institute for Energy Studies (OIES) and the Bureau of Economic Geology (BEG)/Centre for Energy Economics (CEE), University of Texas.

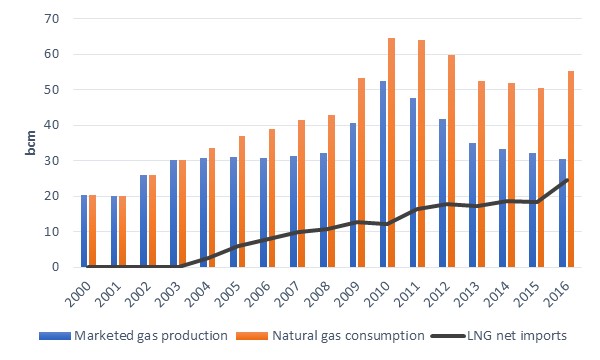

Natural gas production, consumption and LNG imports in India (2000-2016)

{kind=link}

Source: CEDIGAZ

Source: CEDIGAZ

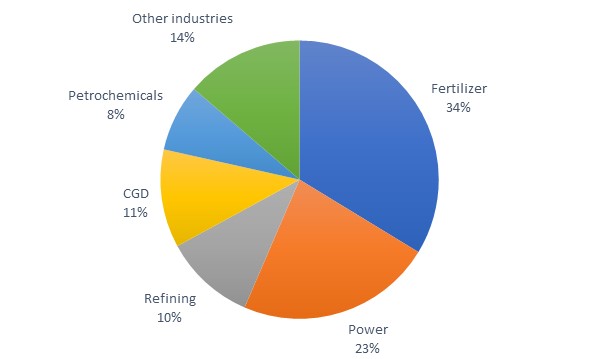

Gas consumption in India is driven by five sectors: fertilizer (34% of total gas demand in fiscal year 2015-16), electric power (23%), refining (11%), city gas distribution, including transport (11%), and petrochemical (8%) industries. In 2016, after five years of consecutive declines, gas consumption increased to 55 bcm, boosted by sales to city gas distribution mainly. The country faces a widening gap between indigenous gas production and demand, which is met by increasing Liquefied Natural Gas (LNG) imports. LNG imports surged by 34% over 2015 to 25 bcm in 2016, making India the fourth largest importer in the world.

Gas demand by sector in FY2015-16

{kind=link}

Source: Ministry of Petroleum and Natural Gas (MoPNG)

Source: Ministry of Petroleum and Natural Gas (MoPNG)

The gas market is characterized by two segments: one using gas at allocated government-controlled prices and the other paying market prices for imported LNG. The first segment, which includes city gas distribution, fertilizer plants, LPG plants and grid-connected power plants, accounts for about three quarters of total gas demand. This segment mainly relies on domestic gas production, complemented by LNG imports whose prices are subsidized by the government. The fertilizer industry, which receives heavily subsidized natural gas in order to support the farmers in India, dominates this segment. Since July 2014, the top gas utilization priority has been allocated to city gas distribution for households and transport, with the aim to significantly expand city gas distribution throughout India. The second segment includes other industrial users and merchant power plants. This segment mainly relies on imported LNG. Power generation from merchant power plants is often too expensive for the almost bankrupt local state electricity distribution companies to purchase. Therefore gas-based power plants have a very low utilization rate and many are stranded assets. As government regulation, not market prices, determines gas allocation, consumption distortions occur. The government recognizes that the current gas allocation policy restricts gas market development by making it difficult to identify the ‘true’ gas demand.

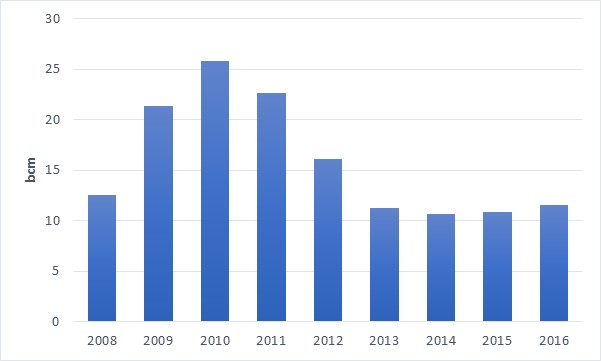

Gas consumption by the power sector (2009-2016)

{kind=link}

Source: MoPNG (fiscal years)

Source: MoPNG (fiscal years)

Increasing the role of gas to 15% of India’s primary energy mix would mean that annual gas consumption would increase to above 200 bcm in the future. However, based on current energy and climate policies, gas demand is expected to grow to only 70 bcm in 2020, 90 bcm in 2025 and 115 bcm in 2030. Gas mainly substitutes or complements oil products rather than coal. The industrial sector, including fertilizers, leads the growth. The role of gas in the power sector is limited to meeting peak demand and load balancing needs and the sector is not expected to drive a surge in gas demand. Rather the government relies on renewables and high-efficiency coal to meet its commitment to reduce the country’s carbon emission intensity by up to 35% by 2030.

Further growth in India’s gas demand depends on several factors. Due to the nascent stage of the gas market, development of gas infrastructure is the most critical enabler for transition to a gas-based economy. Because the ability of end-users to pay high prices for gas-fired power generation and for gas as feedstock is limited, increased gas demand requires continued low prices and government financial support for the fertilizer and power sectors. Increasing domestic gas production is critical and a pre-condition to increase the share of gas in the electricity mix. In light of the country’s growing import dependency, the price of imported LNG will also shape future gas demand in the country.

The government has taken several steps to enhance the availability of gas in the country, including intensification of domestic exploration and production activities, notably with the adoption of a new hydrocarbon exploration and licensing policy (HELP), liberalized gas price regime, and support to LNG imports and to the creation of a national gas grid across India. However, despite the positive steps taken to incentivize natural gas business in the country, a clear and integrated policy that defines—and clearly demarcates—the role of natural gas in India’s energy mix is still missing.

Sylvie Cornot-Gandolphe – SCG Consult for Cedigaz

More: Download the complete PDF report with data figures

Contact: contact@cedigaz.org