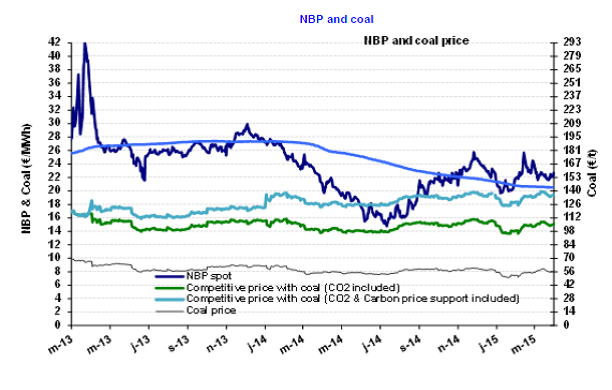

NBP: Long-term and spot prices converging in 2015?

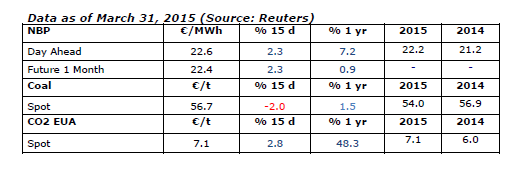

The NBP price averaged €22.3 /MWh ($7.1/MBtu) in March, down 4.5% over February. The average for winter 2014-15 was roughly the same (€22.5/MWh), lower by 16% than that of the previous winter. So concerns over supply (Russia versus Ukraine, uncertainty over Groningue, the storage capacity at Rought) have not had a structural effect on prices.

The NBP price averaged €22.3 /MWh ($7.1/MBtu) in March, down 4.5% over February. The average for winter 2014-15 was roughly the same (€22.5/MWh), lower by 16% than that of the previous winter. So concerns over supply (Russia versus Ukraine, uncertainty over Groningue, the storage capacity at Rought) have not had a structural effect on prices.

In upcoming months, the market is anticipating an average price of €21.5/MWh ($6.7/MBtu) for next summer and €24/MWh ($7.6/MBtu) for next winter. Based on the current forecasts, these levels are moving towards convergence with the prices of oil-indexed contracts. If the trend persists and convergence occurs, this would represent a break with the situation observed since 2009. Between 2009 and 2014, the indexed prices served as a ceiling for the NBP, whose prices were systematically lower.

One should point out that the carbon tax in the United Kingdom will double on April 1st to reach £18.08/tCO2 or €24.9/tCO2. This increase represents an additional cost of €4/MWh for gas-fired power plants and €11/MWh for coal-fired plants. This will significantly affect coal’s competitiveness, which could boost natural gas consumption and exert upward pressure on the NBP price.

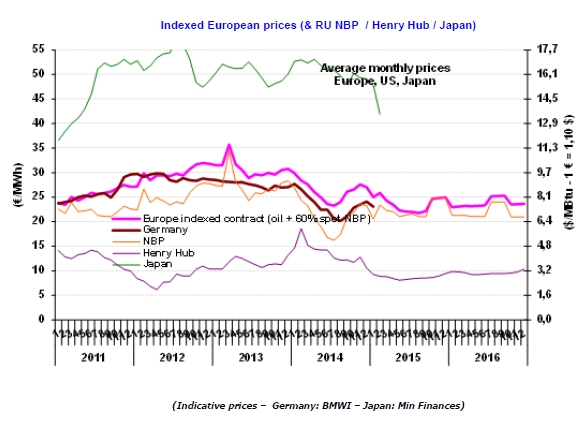

Indexed European price: a significant drop

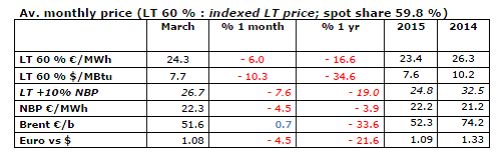

In March, the indicative European price (LT 60%) stood at €24.3/MWh ($7.7/MBtu), down by 6% over February. This decline is due to the downtrend in the NBP price (-4.5%) and in the six-month average for oil prices expressed in euros (-6.7%).

In March, the indicative European price (LT 60%) stood at €24.3/MWh ($7.7/MBtu), down by 6% over February. This decline is due to the downtrend in the NBP price (-4.5%) and in the six-month average for oil prices expressed in euros (-6.7%).

Based on current expectations pertaining to the oil price ($62/b for the Brent at year-end and $67/b at year-end 2016) and to the euro (stability at about $1.08), forecasts see a price of €22/MWh ($7.1/MBtu) for the summer and €24/MWh ($7.6 /MBtu) for the winter.

The oil price trend remains subject to uncertainty, given the geopolitical situation (Yemen) and the effects of future negotiations with Iran to finalize in June the framework agreement.

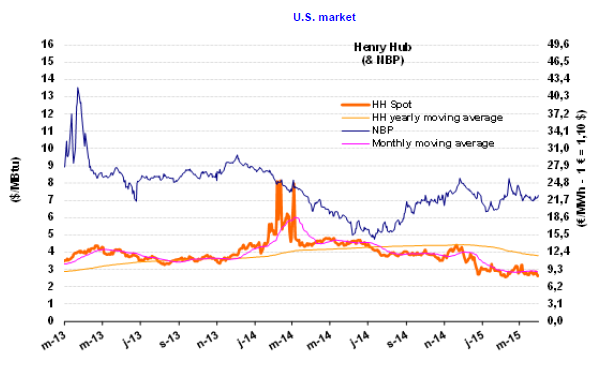

The U.S. market (Henry Hub): downward pressure

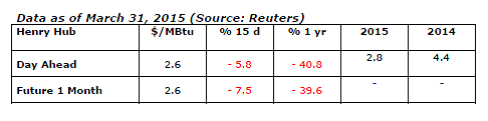

The Henry Hub price fell 0.8% in March, averaging $2.8/MBtu and, like in February, presenting fairly marked variations ($2.6 to 3.3/MBtu). Considering the conditions on the gas market, fairly low prices are expected in 2015 ($2.8/MBtu) and 2016 ($3.1/MBtu). The reason is that shale gas production continues to grow (40 bcf/d in February, i.e. 414 bcm/yr) in spite of the decrease in drilling operations (-31% since September, according to Baker Hughes). The EIA has estimated that total natural gas output will grow by 3.6 bcfd or 36 bcm/yr, a volume expected to exceed the rise in U.S. gas demand in 2015 (2.3 bcfd or 23 bcm/yr).

The Henry Hub price fell 0.8% in March, averaging $2.8/MBtu and, like in February, presenting fairly marked variations ($2.6 to 3.3/MBtu). Considering the conditions on the gas market, fairly low prices are expected in 2015 ($2.8/MBtu) and 2016 ($3.1/MBtu). The reason is that shale gas production continues to grow (40 bcf/d in February, i.e. 414 bcm/yr) in spite of the decrease in drilling operations (-31% since September, according to Baker Hughes). The EIA has estimated that total natural gas output will grow by 3.6 bcfd or 36 bcm/yr, a volume expected to exceed the rise in U.S. gas demand in 2015 (2.3 bcfd or 23 bcm/yr).

By Guy Maisonnier, Senior Economist – IFPEN