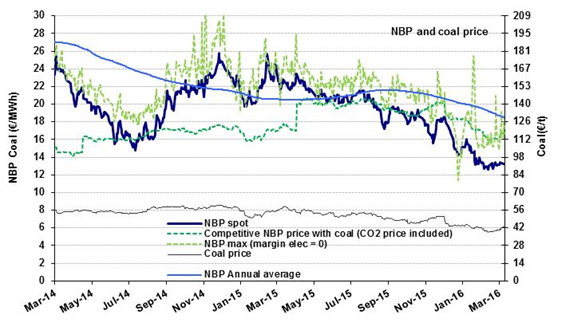

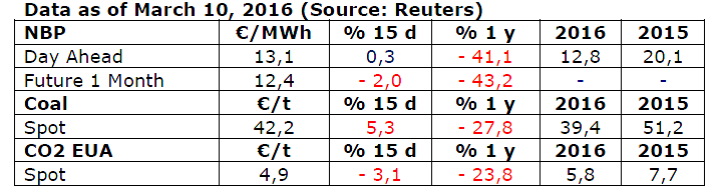

NBP: down next summer

In the first few days of March, the NBP was quoting at about €13/MWh ($4.2/MBtu), close to the previous month’s average. These levels are extremely low. Not since April 2010 (euro prices) and October 2009 (dollar prices) have such low numbers been recorded. The monthly average hit rock bottom at €7.6/MWh ($3.3/MBtu) in September 2009. The markets are not anticipating prices to drop that much next summer, but a series of decreases from the current levels to the vicinity of €11.8/MWh ($3.9/MBtu). For next winter, the NBP is expected to reach $14-15/MWh ($4.6-5.0/MBtu), in line with contracts 100% indexed to oil. This convergence indicates that the market deems $4.6-5/MBtu to be the lowest equilibrium threshold tenable in an average winter.

In the first few days of March, the NBP was quoting at about €13/MWh ($4.2/MBtu), close to the previous month’s average. These levels are extremely low. Not since April 2010 (euro prices) and October 2009 (dollar prices) have such low numbers been recorded. The monthly average hit rock bottom at €7.6/MWh ($3.3/MBtu) in September 2009. The markets are not anticipating prices to drop that much next summer, but a series of decreases from the current levels to the vicinity of €11.8/MWh ($3.9/MBtu). For next winter, the NBP is expected to reach $14-15/MWh ($4.6-5.0/MBtu), in line with contracts 100% indexed to oil. This convergence indicates that the market deems $4.6-5/MBtu to be the lowest equilibrium threshold tenable in an average winter.

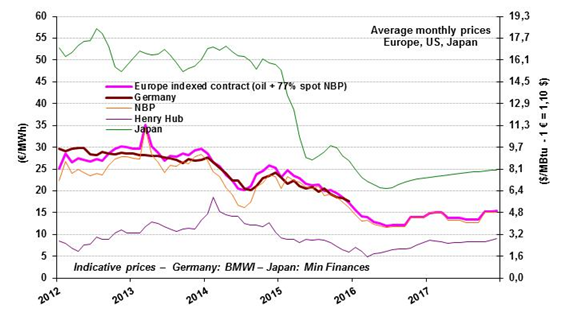

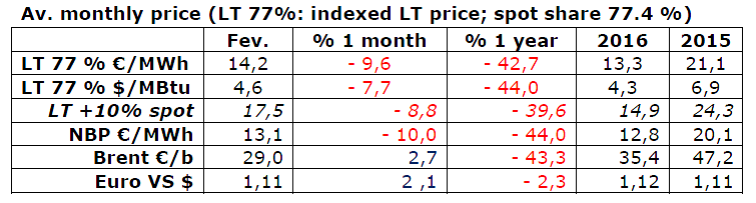

Indexed European prices: down 10% in February

The indicative European price (LT 77%) stood at €14.2/MWh ($5.0/MBtu) in February, down by nearly 10% in a month and by 42% in a year. This is in step with the trends over the same period for spot gas prices (-10%) and prices 100% linked to oil (-8,7%). The Brent’s March upturn – the monthly average was up 17% ($38/b) and the 2016 average (now $40/b) by 10% – will have a moderate effect on short-term LT prices. Forecasts still see prices dropping to €12/MWh ($4.0/MBtu) for next summer, after which they may gradually climb to about €15/MWh ($5.0/MBtu) in the course of next winter.

The indicative European price (LT 77%) stood at €14.2/MWh ($5.0/MBtu) in February, down by nearly 10% in a month and by 42% in a year. This is in step with the trends over the same period for spot gas prices (-10%) and prices 100% linked to oil (-8,7%). The Brent’s March upturn – the monthly average was up 17% ($38/b) and the 2016 average (now $40/b) by 10% – will have a moderate effect on short-term LT prices. Forecasts still see prices dropping to €12/MWh ($4.0/MBtu) for next summer, after which they may gradually climb to about €15/MWh ($5.0/MBtu) in the course of next winter.

The U.S. market (Henry Hub): free fall

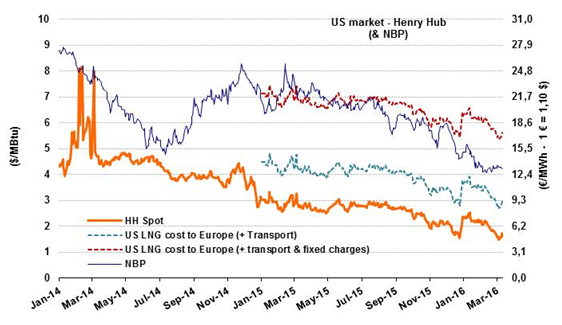

The Henry Hub’s January upsurge (+17%) did not last. On the contrary, it lost 13% in February, slipping below the $2/MBtu mark again. Since end February, it has hovered between $1.5 and 1.7/MBtu, affected by the high level of stocks. On March 4, the latter stood at 2480 bcf (70 bcm), exceeding the maximum levels observed for the last five years. In its March forecasts, the EIA projected that, in 2016, production would grow more slowly, pipeline imports would be down and LNG exports would rise. These trends should help gradually restore market equilibrium, which is why prices are expected to increase at year-end ($2.6/MBtu in December). It should be noted that, in 2017, the United States will be virtually self-sufficient in natural gas, with net imports of 2 bcm (Import/export balance 14 bcm in pipeline imports; 12 bcm in LNG exports). In 2007, the U.S. was still importing 107 bcm, equivalent to 16% of national consumption.

The Henry Hub’s January upsurge (+17%) did not last. On the contrary, it lost 13% in February, slipping below the $2/MBtu mark again. Since end February, it has hovered between $1.5 and 1.7/MBtu, affected by the high level of stocks. On March 4, the latter stood at 2480 bcf (70 bcm), exceeding the maximum levels observed for the last five years. In its March forecasts, the EIA projected that, in 2016, production would grow more slowly, pipeline imports would be down and LNG exports would rise. These trends should help gradually restore market equilibrium, which is why prices are expected to increase at year-end ($2.6/MBtu in December). It should be noted that, in 2017, the United States will be virtually self-sufficient in natural gas, with net imports of 2 bcm (Import/export balance 14 bcm in pipeline imports; 12 bcm in LNG exports). In 2007, the U.S. was still importing 107 bcm, equivalent to 16% of national consumption.

By Guy Maisonnier – Senior Economist – IFPEN