In the fourth quarter of 2022, average European and Asian prices fell back compared to the previous year. European prices have been extremely volatile in the short term, with periods of dramatic, weather-driven declines. The TTF price has fallen over the last four weeks to pre-war levels in Ukraine, a sign of unexpected easing in the European market as the Russian gas crisis intensifies. The drop in gas consumption, due to unusually mild weather and the decline in industrial activity, and the continued strong growth in LNG imports explain the very high level of European gas stocks, which reaches 930 TWh at the beginning of 2023. This situation has pushed down spot and forward prices and eased fears of tensions in the coming months.

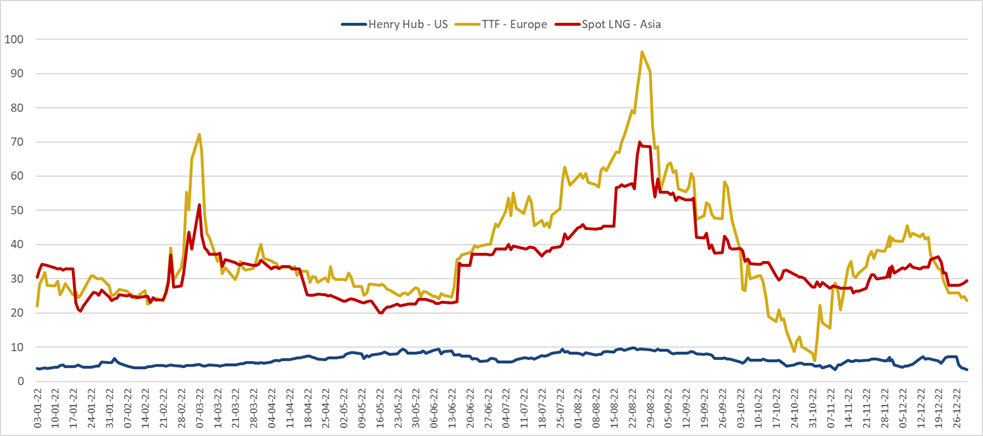

Evolution of international gas prices in the fourth quarter of 2022

Although the Russia-Ukraine crisis persists, Russian gas supplies to Europe are at their lowest and the LNG market remains tight, average European and Asian prices fell by 9% and 11% respectively in the last quarter of 2022 compared to the fourth quarter of 2021 to reach $29/MMBtu and $31/MMBtu respectively.

These averages mask irregular trends that reflect extreme variations in weather conditions. After peaking at over $300/MWh in August, the European TTF price fell sharply until the end of October, the hottest month on record, before rising again in the following weeks as temperatures fell. Then, since mid-December, the exceptionally mild weather and the slowdown in economic activity ahead of the Christmas holidays caused consumption and prices to fall back. The latter have lost half their value over the period and now stand at €65-70/MWh, i.e. levels seen before the war in Ukraine and even before the winter of 2021-22.

Asian spot prices remained highly correlated with European prices as the global LNG market remained tight. However, short-term volatility has been lower in the Asian market, where weak demand, especially in China, and high levels of LNG stocks cap market prices.

The US Henry Hub spot price averaged 20% above the fourth quarter 2021 level. In December, severe winter storms put upward pressure on gas demand and prices. However, since the end-December, the Henry Hub has fallen back and plunged to its multi-month low at 3.3 $/MBtu on forecasts for warmer-than-normal weather and lower heating demand than previously expected.

The average Japanese LNG price is estimated at 19$/MBtu in the fourth quarter of 2022, down 5% from the previous quarter of the same year, reflecting the decline of the JCC price since June.

Figure 1: Evolution of daily international spot gas prices in 2022 ($/MBtu)

Source: Reuters, IFPEN, CEDIGAZ

Evolution of international LNG trade

Global net LNG flows continued to show strong growth in the last quarter, up 5% over 2021. As in the previous quarter, Europe absorbed most of the additional supply, while demand from Asia, and China in particular, remained sluggish. On the export side, the US remains by far the largest contributor to the growth in both global and European LNG supply.

Figure 2: Evolution of monthly global LNG supply (Mt)

Source: CEDIGAZ LNG Service

LNG plays a major role in Europe to compensate for the cut-offs of Russian gas supplies. From January to December 2022, total EU gas imports fell by 16% (-4.5 bcm), with pipeline deliveries of Russian gas collapsing by 81% (-6.5 bcm). From January to December 2022, the share of Russian gas in total imports collapsed from 28% to 6%, while the share of LNG imports (from all sources) jumped from 35% to 48%. Pipeline imports from other sources remained stable. Their short-term growth potential is limited.

Price Outlook 2023

In Europe, the decrease in consumption (-20% in the last quarter of 2022 vs. 2021) and the strong growth in LNG imports (+70% in the last quarter of 2022 vs. 2021) have limited the drawdown in European storages during the last quarter. The current level of European storage, which amounts to 930 TWh, is 30% higher than the 2011-2021 average. These very high levels of gas stocks and the unusually mild winter have weakened the expected forward prices for this year 2023. European markets now expect an average TTF price of around €70/MWh in 2023, compared to €123/MWh in 2022. Although the weather factor remains a determining factor in the evolution of market prices, the current conditions of the European market do not give rise to fears of major tensions in the near future. The increase in LNG regasification capacity and the energy saving measures aim to avoid a gas deficit in Europe. However, a resurgence of tensions is still possible as early as this summer when refilling stocks due to Russian gas cuts and a likely resumption of Chinese industrial demand, which will increase competition on the global LNG market.

Armelle Lecarpentier, Chief Economist, CEDIGAZ

Contact us: contact@cedigaz.org

Cedigaz (International Center for Gas Information) is an international association with members all over the world, created in 1961 by a group of international gas companies and IFP Energies nouvelles (IFPEN). CEDIGAZ collects and analyses worldwide economic information on natural gas and renewable gases in an exhaustive and critical way.