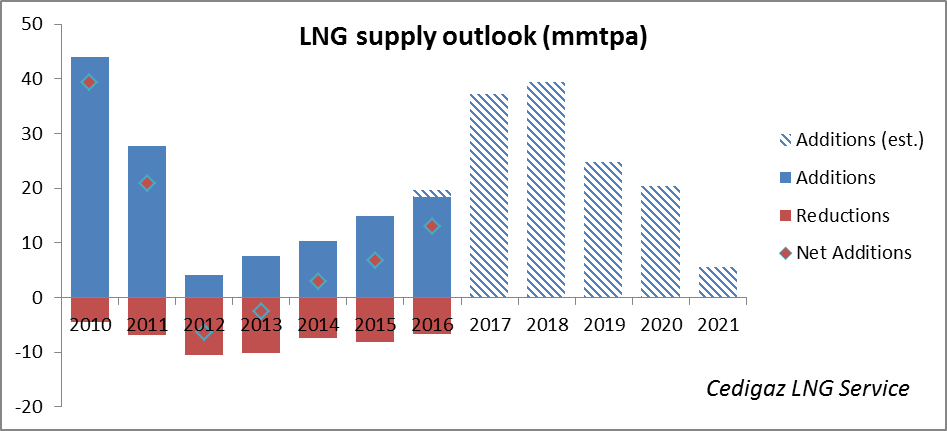

The ramp of new LNG production accelerated in 2016 when 16 million tons of new LNG supply were added to the market, representing a 6.8% annual growth. This was the highest growth rate recorded since 2011 but it only represents the very beginning of the LNG wave that is about to hit the market. There are still about 110 mmtpa of new capacity under construction that are expected to start producing from now to 2020-2021. This equates to around 42% of the 2016 LNG demand that would come on line in a very short time, raising the question of the capacity of the market to absorb the additional volumes and at what price.

2015 saw the unexpected decline of LNG demand in Asia. This unsettling development had two main reasons. First the end of the Fukushima-driven growth in the JKT countries, especially in Japan, together with energy conservation policies led to a strong decline of LNG demand in the historical Asian markets. Second the collapse of Chinese LNG demand growth due to price issues and the competition with piped gas. On the bright side, 2015 witnessed the emergence of new buyers (Egypt, Jordan and Pakistan) – that were able to take advantage of the low price environment, thanks to the flexibility offered by FSRUs -, as well as accelerated growth in the MENA region.

The situation in Asia somewhat normalized in 2016 with the resumption of strong growth in China and a price-driven acceleration of demand growth in India, but LNG demand continued to decline in Japan (-2%), and stagnated in Korea (+0.6%). Meanwhile, growth from new importers and MENA remained robust. In spite of a 5% growth of gas demand in Europe, net LNG imports only grew by a timid 1.7%, as flexible LNG was displaced by increased Russian imports.

Looking forward, if the start-up of the LNG plans currently under construction goes as scheduled, more than 30 mmtpa of new LNG capacity could come on line this year (including additional volumes from the ramping-up of trains launched in 2016), followed by a similar amount in 2018. In 2019, supply capacity additions could still top 25 mmtpa, with another 20 mmt expected in 2020. On top of that, Angola LNG should finally become fully operational, adding another 5.2 mmtpa to the market. Similarly, the restart of Yemen LNG (6.7 mmtpa) cannot be discounted.

On the demand side, while Chinese imports are still expected to grow strongly (be it at a slower pace than that projected a few years ago ), aggregated demand from the traditional Asian buyers (Japan, Korea, Taiwan) should plateau from now to 2020. Low prices should support growth in price sensitive markets like India in particular, although infrastructure bottlenecks in this country could act as a limiting factor. The expected launch of two new FSRUs should support a strong growth of Pakistan LNG imports to 2020. In Egypt, which became the eighth biggest importer in 2016, only one year after starting LNG imports, major new upstream developments (especially the development of the super-giant Zohr field) should lead to a decrease of LNG imports post 2018. In the Middle-East, gas demand growth should remain robust, driven by the power sector although LNG imports in Jordan could suffer from the start of pipeline imports from Israel. In Europe, some growth is likely, driven by a slightly improving competitive position of gas versus coal but more importantly, rapidly declining domestic production will translate into higher imports. How much of these will be LNG will depend on Russia’s commercial approach.

On the demand side, while Chinese imports are still expected to grow strongly (be it at a slower pace than that projected a few years ago ), aggregated demand from the traditional Asian buyers (Japan, Korea, Taiwan) should plateau from now to 2020. Low prices should support growth in price sensitive markets like India in particular, although infrastructure bottlenecks in this country could act as a limiting factor. The expected launch of two new FSRUs should support a strong growth of Pakistan LNG imports to 2020. In Egypt, which became the eighth biggest importer in 2016, only one year after starting LNG imports, major new upstream developments (especially the development of the super-giant Zohr field) should lead to a decrease of LNG imports post 2018. In the Middle-East, gas demand growth should remain robust, driven by the power sector although LNG imports in Jordan could suffer from the start of pipeline imports from Israel. In Europe, some growth is likely, driven by a slightly improving competitive position of gas versus coal but more importantly, rapidly declining domestic production will translate into higher imports. How much of these will be LNG will depend on Russia’s commercial approach.

Overall, projected supply-demand dynamics point out to the prolongation of the current buyer’s market and depressed prices well into the first half of the next decade. The coming online, mainly between 2018 and 2020, of massive amounts of flexible US LNG will put an additional pressure on prices. This raises the question of whether all these new volumes will find a market. The answer will largely depend on how growth markets, i.e. Asia and the Middle East, react to low prices and to what extent Europe can play the role of “market of last resort”.

Geoffroy Hureau – Secretary General – CEDIGAZ

Article written for the Flame conference: https://informaconnect.com/flame-conference/