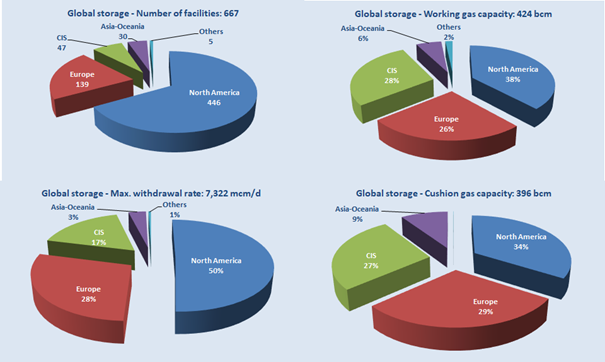

Key UGS metrics in the world remained virtually unchanged in 2021

Seven new storage facilities were commissioned, six of which were in China and one in Sharjah. These new capacities were largely offset by declines in the main storage markets. Overall, the global number of storage facilities, working gas capacity and peak withdrawal rates remained virtually unchanged year-on-year.

… but interest in UGS is growing, as evidenced by a growing pipeline of new projects and expansions totalling 133 bcm of working capacity

While the UGS market remains highly concentrated, with 5 countries (United States, Russia, Ukraine, Canada and Germany) accounting for almost 70% of global storage capacities, there is a clear shift of storage activity towards new, fast growing gas markets, China and the Middle East notably.

Global underground gas storage at the end of 2021 – by region

Source: CEDIGAZ

Gas storage market trends in 2021 and 2022 – Key takeaways

- Russia’s invasion of Ukraine is reshaping global gas markets and putting security of supply at the top of gas importing countries’ agenda.

- Europe: gas storage essential for security of supply and market resilience

- New EU regulation requires that stocks levels are filled ahead of winter, at least at 80% by 1 November 2022, and 90% the subsequent winters.

- Increased supply of LNG, mainly from the US, and gas by pipeline from Norway and Azerbaijan, together with demand reduction, have enabled Europe to fill its stocks at 95% of their maximum working gas capacity on 1 November 2022.

- European countries are reopening storage facilities (Rough in the UK) and investing in UGS expansion (Poland).

- Despite difficult conditions, Ukraine has filled its UGS

- Russia: Reduced exports led to fast replenishment of gas stocks

- Pivot to the East strategy requires a significant development of the gas transmission and UGS facilities.

- But China may not want to rely too heavily on a supplier that has shown a willingness to use gas as a political weapon.

- US growing demand and exports lead to lower stock levels

- Growing LNG exports and rising domestic consumption have led to lower stock levels all along 2022, putting pressure on the HH price.

- Higher injection rates in September and October 2022 have reduced the storage deficit, reducing spot prices. This trend is expected to continue after winter2022/23.

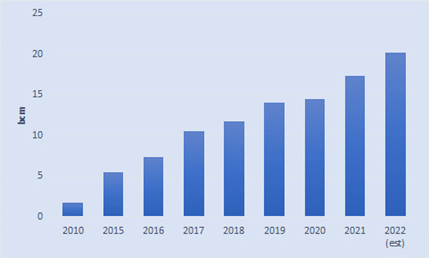

- China: Significant increase in storage capacity

- The global gas crisis has reinforced the acceleration of UGS construction with significant increases in working gas capacity in 2021 and 2022. Working gas capacity totalled more than 20 bcm at the end October of 2022.

- Total gas storage capacity is expected to reach 55 bcm to 60 bcm in 2025 (of which 32 bcm of working gas capacity in UGS), accounting for around 13% of expected natural gas demand.

Evolution of China’s storage working gas capacity (2010-2022)

Source: CEDIGAZ

- Central and South America advances UGS projects

- Brazil is building the first UGSs in the country, while Mexico has revived its previous gas storage policy, including the building of strategic storage of natural gas.

- The Middle East is expanding its storage market

- The storage market is expanding in the Middle East.

- Sharjah opened the second UGS facility of the Emirates at the beginning of 2021 (Moveyeid gas storage).

- Saudi Arabia is building its first UGS facility, the Hawiyah Unayzah Gas Reservoir Storage (HUGRS).

By Sylvie Cornot-Gandolphe, Consultant on Energy Markets and Raw Materials, CEDIGAZ

UNDERGROUND GAS STORAGE IN THE WORLD – 2022 STATUS

November 2022 – 45 pages PDF format

For more information: contact@cedigaz.org

CEDIGAZ (International Center for Gas Information) is an international association with members all over the world, created in 1961 by a group of international gas companies and IFP Energies nouvelles (IFPEN). Dedicated to gas information, CEDIGAZ collects and analyses worldwide economic information on natural gas, LNG, renewable gases (hydrogen, biogas) and unconventional gas in an exhaustive and critical way.