Pragmatism, optionality and communication were the words of the day at Cedigaz’ traditional annual seminar held in Paris on June 20th. Members of the European gas industry and overseas producers say these are badly needed to make long-term plans, ensure energy security and a ‘just’ energy transition. More than two years after the unprecedented energy crisis sparked by Russia’s invasion of Ukraine in February 2022, the list of challenges is not short: worsening global macro-economics, industrial demand destruction, chaotic global geopolitics, the imperative to fight climate change, and the necessity for Europe to boost its economic competitiveness and stem the tide of populism that has been fueled by higher food, energy and costs of living.

Political Uncertainty

The event, which brought together more than 70 delegates active across the gas value chain, was dominated by bittersweet feelings. The fact that Europe managed to avert major energy blackouts and worst-case scenarios after the war in Ukraine broke out demonstrated its capacity to respond to reduced Russian gas pipeline supplies.

But this was not without record prices spikes and wider socio-economic damages, from job losses at industrial sites in Europe, to costs incurred by poorer nations in emerging markets who could not afford to pay record LNG prices and turned to coal and oil for their own energy security.

Despite wider perceptions, the energy crisis which actually started in 2021 due to a structural supply-demand imbalance is not over. Many at the seminar warned against any complacency over security of supply. On the other hand, the rippling effects of reduced Russian gas pipeline supplies in Europe and beyond are a stark reminder of the importance of better forecasting and managing gas and energy demand in order to avoid price spikes.

Policy and effective governance remain key to this. At last year’s seminar, delegates were already criticizing the lack of precision on the role of gas in the EU’s energy transition policy and in the RePowerEU plan in particular. Such concerns were reiterated this year after the UAE consensus reached at the latest COP28 in December 2023. And following the recent European parliamentary election, more uncertainties are looming. A different political framework will govern the EU’s climate and energy policies for the next five years, raising deeper questions on the implementation of the Green Deal and making the importance of energy security and affordability more pressing than ever.

Shifting Supply and Demand

In 2023, gas demand in Europe registered a 7.4% decline to 444 bcm, its lowest level since 1995, according to Cedigaz. The drop was primarily driven by a combination of mild winter temperatures, falling demand for gas-fired generation due to increased renewable and nuclear energy capacity, as well as energy savings from the residential and commercial sectors.

The demand destruction from industrial sites due to high prices and economic difficulties sparked by cuts in Russian pipeline supplies also contributed to the sharp drop in consumption. Despite a relative recovery in 2024, some delegates believed it was still too early to make a full assessment on whether this demand destruction was permanent or not. But undeniably, this issue has stressed the need for Europe to boost its industrial competitiveness across sectors. The theme of competitiveness remains a fundamental, underlying concern as it is increasingly correlated with bigger geopolitical challenges and forces, such as the major trade wars between China and the US regarding clean energy equipment.

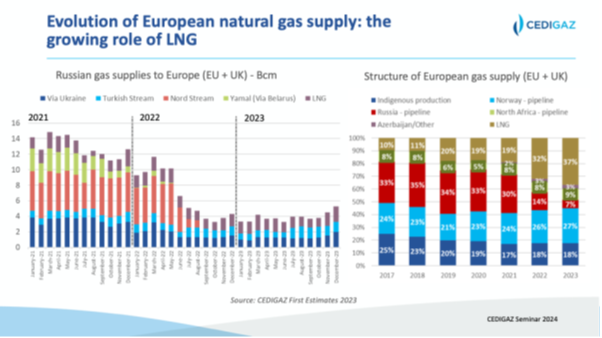

On the supply side, historically high storage levels continued to play an essential part in 2023 thanks notably to the emergency measures introduced by the European Commission in 2022, as praised by many during the seminar. LNG remained the other major supply lever as Russian pipeline gas supplies to the EU fell to 26 bcm in 2023, down from 65 Bcm in 2022 and 146 bcm in 2021. This came with a higher concentration of LNG providers, however, especially from the US, which catered for 48% of Europe’s LNG supplies in 2023, against 44% in 2022, and 26% in 2021.

High Prices

The European Index TTF fell by 66% year on year to 41€/MWh in 2023, due to a steep reduction in natural gas demand, record-high gas storage levels and US LNG imports. It has remained highly volatile, however. On a global level, demand remained sustained even if it was still below pre-war levels. Despite the drop in Europe, global consumption ticked up by 0.6 % to 4047 bcm, primarily due to increased demand in Asia (+2.3% to 905.8 bcm) and the Middle East (+3.4% to 590.3 Bcm). In 2024, demand indicators remained strong in the first five months of the year, with LNG imports into Asia posting significant year-on-year increases (+10.37 mt year on year, up 15.3% to 115.31 mt), partly due to prices becoming more attractive for buyers such as China and India.

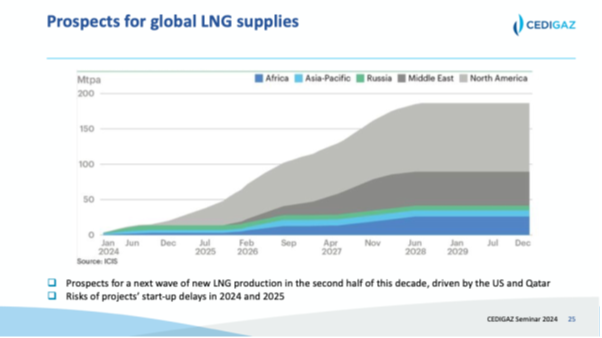

Importantly, with the role of LNG constantly growing, sluggish supply growth of the fuel means supply risks remain significant during the next two winters at least, until the next wave of LNG projects from Qatar and the US come online. This is reflected in the price strength displayed on the forward curve at the TTF due to several bullish factors: from risks of delays in LNG projects, unplanned outages, and the end of the transit contract through Ukraine’s transmission system on 31st December 2024. Other key drivers comprise the demand growth in Asia, as well as increasingly unpredictable weather such as heatwaves recently seen in South Asia, or the possible return to ‘normal’ cold temperatures next winter.

What Worked

Perhaps one lesson from the energy crisis is that politicians and regulators alike “understood” the value of the flexibility offered by LNG, participants stressed at the seminar. This point was backed by increased investment in new regas capacity in Germany for instance, the deployment of new FSRUs, and on other levels, the consolidation of new long-term deals through existing or newly forged commercial partnerships. Another argument in this direction is the resurgence of interest in capacity bookings at terminals for longer periods, according to some operators.

Gas companies also optimized the opportunities offered by the European gas pipeline network through the improvement of cross-border interconnections, notably for west-to-east flows to countries in Central and Eastern Europe that remain highly dependent on Russian pipeline gas.

Who Will Pay?

This was not cheap, and the reality is that more needs to be done to ensure solidarity and boost cross-border infrastructure. But as raised in the seminar, in the current political and economic context, it is difficult to justify investing in new long-term infrastructure that could potentially become stranded if gas demand is severely dented by climate-driven policies in the longer run.

The hard truth is that gas is expected to remain expensive in the foreseeable future, until at least more LNG supplies are scheduled to reach the market by the end of the decade. Beyond that horizon, things look blurrier for both gas consumers and producers to be able to make investment decision now.

There are clear demand drivers in key regions such as Asia and emerging markets, primarily because of population growth and economic developments. But trends vary considerably across the globe, not least because of the plethora of policies (or arguably, lack of, in some parts) and different scenarios depending on sectors, geographies and even competing fuels.

In addition, understanding and re-assessing demand drivers is becoming more complex as energy security, geopolitical risks, and decarbonization policies are increasingly intertwined. Such parameters raised different questions from participants at the seminar: from the evolving economics of gas as a baseload fuel, the pace of coal-to-gas switching in emerging economies, to the implications of often-changing regulation for the electrification of the residential sector through the deployment of heat pumps in some European countries.

Fuel Neutrality

One constant fundamental is the flexibility and optionality that can be offered by LNG, both in physical and commercial terms. Simply put, LNG allows players, importers and nations to calibrate the pace of their transition more effectively than if one has inflexible supply, said one analyst.

This approach calls on a pragmatic, fuel-neutral perspective on global climate and energy policy, something that has been lacking in Europe at least, according to many at the seminar. Such worries have been exacerbated by some narratives resulting from the UAE consensus reached at the Convention of the Parties (COP 28) in December 2023. The consensus was a step forward in that it called for a transition away from fossil fuels in energy systems, in a just, orderly and equitable manner for the world to achieve net zero emissions by 2050. It also recognized the role of gas as a transition fuel.

But clear pathways and targets for the fuel are missing, attendees concurred at the seminar. The consensus promotes short-term measures based on analysis and scenarios from the International Energy Agency (IEA): tripling the capacity of renewable energy (including biogas) by 2030, doubling the rate of efficiency measures, and reducing methane emissions. In Europe, the IEA sees gas demand peaking before 2030. By 2050, it sees it falling to around 30 bcm, just a tenth of what it is today, if Europe achieves its net zero target by 2050.

By its own admission, the IEA sees a mixed and uneven picture for the development of renewables and clean technologies across some advanced economies and some emerging markets, primarily due to the shortage of affordable finance. The IEA also sees a role for hydrogen, and carbon capture and storage beyond 2050, despite many challenges.

Public Funding

With regards to hydrogen, delegates agreed that the E

U’s 2030 hydrogen targets (producing 10 mt of clean hydrogen and import another 10 mt) under RePowerEU look unlikely to be met. Fundamentally, high costs and lack of projects’ progress have been stifling demand growth in this segment. For both projects and infrastructure, developers have been faced with high capital, development, and operating costs, including the costs of electrolyzers that still need to be imported.

The need to be less dogmatic about green hydrogen was mentioned again with some calling for political leaders and regulators to be pragmatic about the benefits of other sources of hydrogen and focus instead on defining standards for low-carbon hydrogen. Projects’ advocates called for greater cross-border cooperation for the development of a European market, despite the existence of political support at the EU and national levels, at least on paper. They say more public funding is required, in addition to policies that are more focused on local industrial development and competitiveness.

At a time when election outcomes have been clearly dictating short-term politics and budgets, one delegate stressed the policy-driven nature of the energy transition and called the future Commission to be clear on its future intentions on hydrogen, so that the responsibilities and financial risks endorsed by all stakeholders are clarified.

Low-Carbon Initiatives

The argument from many at the seminar, is that after years of backlash against gas due to mounting climate-driven pressure, the energy crisis in 2022 highlighted the crucial role of LNG as a transition fuel to replace dirtier fuels like coal. Clearer signals through targeted funding are required so companies can take position on future investment in supply, infrastructure. This goes hand in hand with incentives that support efforts to cut greenhouse gas emissions, delegates insisted.

Practical examples and initiatives have been undertaken to decarbonize LNG operations, an objective widely shared by many LNG players, from upstream to downstream operations. These include greater data provision and transparency on cargoes’ emissions to better offset their carbon footprint – a trend that was disrupted by the energy crisis in 2022, but now expected to pick up. Other projects aim to cut carbon emissions at LNG sites, thanks to the electrification of

operations and the introduction of CCUS.

Some participants are also joining forces to tackle the thorny issue of methane emissions. But data provision and transparency from producers across the world remain a challenge, something that can be made worse by current geopolitical conflicts.

Self-Examination

These initiatives need to be scaled up to establish a market-driven, level-playing field for ‘low-carbon LNG’ and gain a competitive edge against other overseas importers. The onus is now on political leaders and regualors, participants concurred.

These initiatives need to be scaled up to establish a market-driven, level-playing field for ‘low-carbon LNG’ and gain a competitive edge against other overseas importers. The onus is now on political leaders and regualors, participants concurred.

In the meantime, some at the seminar stressed the need to keep nurturing an honest amount of self-examination and bolder advocacy. The gas industry remains a fossil-fuel-based sector that needs to tackle climate change by starting change from within.

In a world currently overwhelmed by change, gas suppliers and infrastructure companies say they are the ones taking full financial risks to create practical net-zero paths with low-carbon fuels such as hydrogen, whilst still seeing gas as an insurance for energy security to make the energy transition work. This echoed yet again the need for better communication from gas players to carve themselves a positive role in the energy transition narrative. As one voice stressed, the industry has been “bad at explaining the problem, as well as explaining the solution”.

Fatima Sadouki – Independent Energy Specialist – for CEDIGAZ