CEDIGAZ has recently published its annual survey on the global hydrogen market along with comprehensive databases on low-emission hydrogen production projects worldwide. The report tracks recent policy and market developments of the global low-emission hydrogen sector. It also focuses on project development and medium-term demand and supply prospects.

Recent trends in hydrogen investments have shown that the development of low-emission hydrogen is faced with major challenges. In contrast to mature technologies of the energy transition, investments in emerging technologies, including hydrogen, have not grown as fast as expected. The European hydrogen industry has experienced a turbulent 2025, with project delays and cancellations dominating the headlines. The proportion of projects at the FID stage remains very low and the global clean hydrogen market is still in its infancy. Global low-emission hydrogen demand amounted to less than 1 Mt in 2025, or only around 1% of global hydrogen demand.

New hydrogen investment has been very selective, focusing on demand-secured and government-backed projects. The most advanced projects mainly occur in existing industrial hubs rather than in new applications. Policy uncertainty and high costs were the most frequent reasons announced by investors to justify projects’ cancellations. But the real hurdle for hydrogen investment seems to be the lack of offtakers and insufficient demand-side incentives. Regarding policy targets, progress was made on the demand side, but this remains low compared to the supply side.

Nevertheless, governments and private companies continue to bank on the significant potential of low-emission hydrogen for decarbonising many high-emission sectors (manufacturing, fertilisers, steel, transportation, and electricity), which are moving toward decarbonization at varying paces depending on the geographic zone. Demand-side policies have moved forward, frequently in the form of grants and sectoral quotas.

The diverse support mechanisms which are being implemented worldwide to accelerate hydrogen development aim in particular to reduce the cost gap between low-emission hydrogen and its fossil counterparts. In developed countries, key ongoing subsidy developments include the European Hydrogen Bank auctions, the Japanese CfD scheme, H2Global and North American tax credits. But year 2025 has showed that the most significant progress in hydrogen developments from the public and private sides occurred in emerging economies, especially China, and, to a lesser extent, India (SIGHT program).

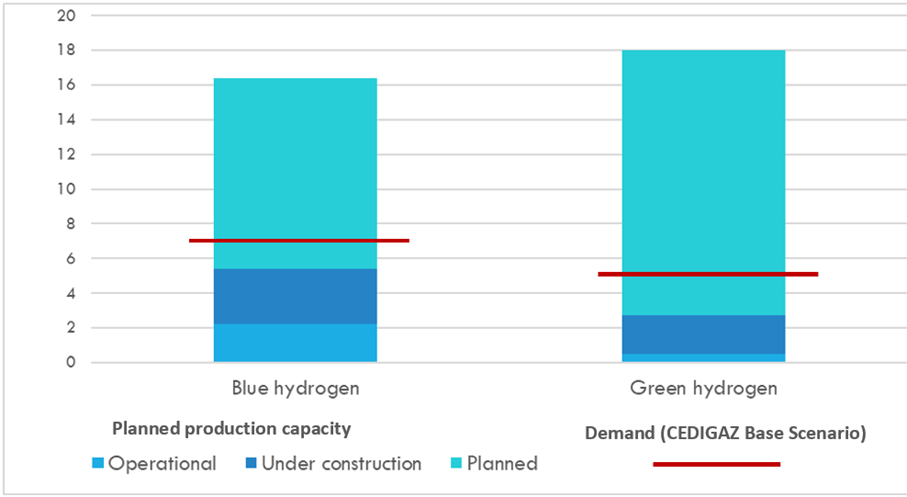

In total, operational and under construction facilities represented a production capacity of more than 8 Mt (including 5.4 Mt of blue H2 and 2.7 Mt of green H2) at the end-2025 or only 24% of the total planned and feasible capacity by 2030. China is undoubtedly the global leader in green hydrogen projects commissioning and construction. In 2025, its operational and post-FID green hydrogen production capacity reached 1,2 Mt, accounting for almost half of the world total, followed by India (0,5 Mt).

Only 17% of exported blue hydrogen projects and 9% of export-oriented green hydrogen projects have taken FID. Large-scale export-oriented green hydrogen projects which are mostly located in emerging and developing economies face funding challenges and an acute lack of offtakers. The lack of infrastructure is also a major hurdle. Hydrogen infrastructure has yet to leave its embryonic stage.

Today, the production capacity is largely under-utilized but low-emission hydrogen demand growth is expected to accelerate towards the end of the decade. Based on offtake deals, low-emission hydrogen demand is forecast to reach around 9 Mt by 2030. It is likely that the short-term increase in post-FID projects capacity (which has already reached 8 Mt today) will give a further boost to low-emission hydrogen demand. In Cedigaz Base Scenario, low-emission hydrogen demand is expected to reach 12 Mt by 2030. In Cedigaz high demand scenario which assumes a rapid acceleration of the energy transition, low-emission hydrogen demand is forecast to reach 18 Mt in 2030. The high scenario of the consultant Rystad predicts approximately 20 Mt in 2030. Even in these optimistic scenarios, potential projects’ capacity will largely exceed the demand.

These forecasts remain largely insufficient for hydrogen to contribute to a net zero-carbon pathway (which would mean a low-emission hydrogen demand of 123 Mt in 2035 according to the IEA Net Zero Emissions Scenario). Much stronger supportive policies are needed to scale beyond the present forecasts. Structural measures are necessary (stronger incentives and mandates, demand-side policies, higher carbon prices) to ensure the fundamental economics that will lead to long-term hydrogen demand at scale. As regards global supply, standards and certifications are critical to pursue subsidy schemes and support hydrogen commercialisation. Alongside R&D, public funding and technological developments needed to bring down the costs and remove technological barriers, companies will pursue collaboration efforts with all players involved, develop appropriate business models and solid international partnerships to allow the build-up of integrated international supply projects.

Figure 1: Planned and feasible production capacity versus low-emission hydrogen demand by 2030

Source: CEDIGAZ

Armelle Lecarpentier for CEDIGAZ

Get the full report (37 pages – PDF – €990)

For more information: contact@cedigaz.org

Cedigaz (International Information Center on Natural and Renewable Gases) is an international association with members all over the world, created in 1961 by a group of international gas companies and IFP Energies nouvelles (IFPEN). Dedicated to natural and renewable gas information, CEDIGAZ collects and analyses worldwide economic information on natural gas, LNG and low-carbon gases in an exhaustive and critical way.