By Irina Mironova for Cedigaz

In a previous blog, we examined the constraints affecting Qatari LNG supply. This note shifts the focus to the receiving end: how do importers of Qatari LNG manage supply disruptions?

We review the approaches of importers across the following clusters:

- China – state-controlled diversified buyers

- India – structurally short, price-sensitive system

- Pakistan and Bangladesh – emerging Asian importers with divergent strategies and outcomes

- Taiwan, Korea and Japan – portfolio optimization and domestic system flexibility

- Kuwait – locked inside the Gulf

Exports from Qatar – Contracts structure

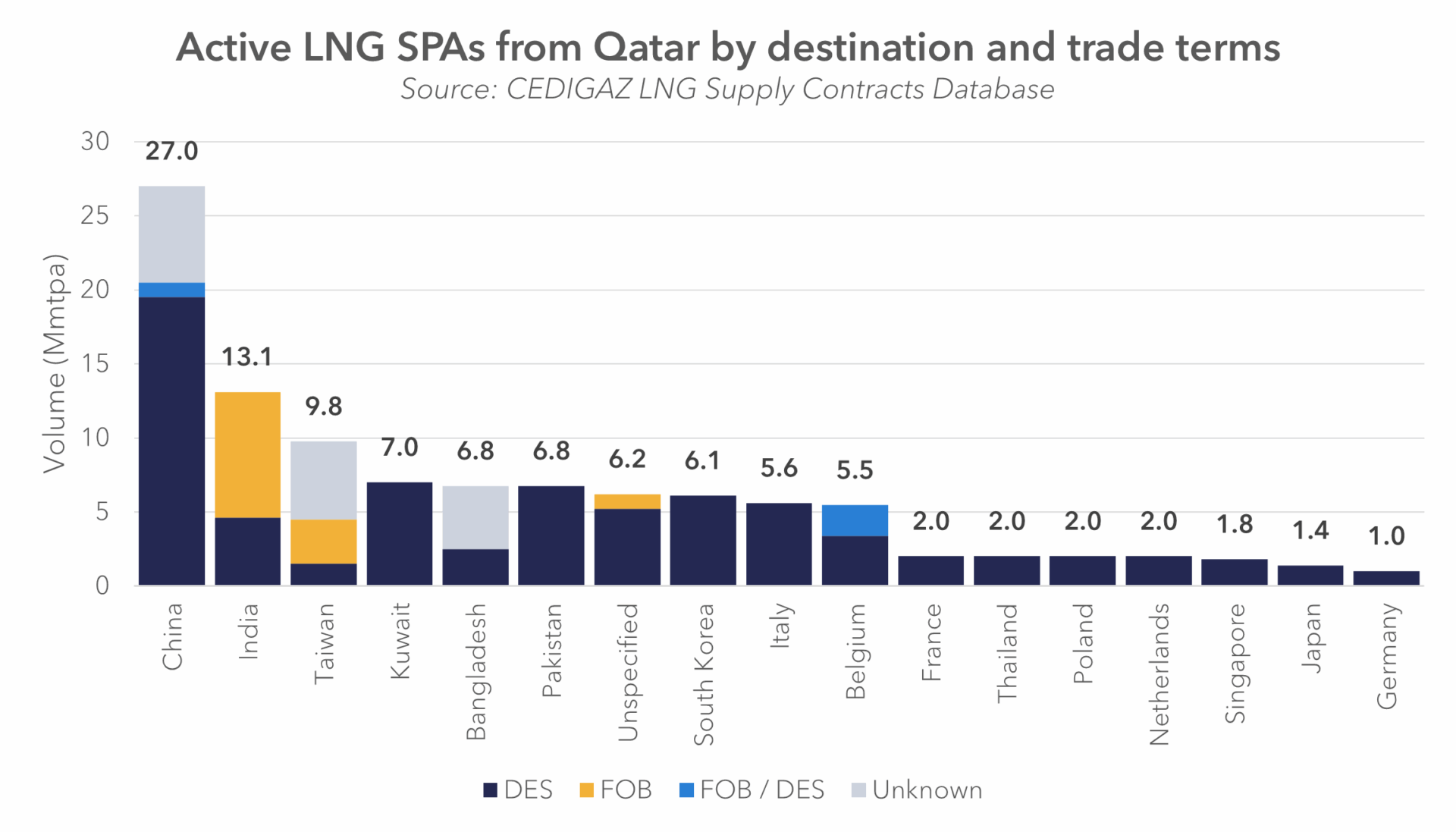

Qatari supply is framed through a set of long-term contracts. According to the Cedigaz LNG Supply Contracts Database, the largest volumes are contracted to China (27 mtpa), followed by India (13.1 mtpa), Taiwan (9.8 mtpa), Kuwait (7.0 mtpa), and Bangladesh and Pakistan (6.8 mtpa each).

Qatari LNG exports are structurally rigid. Of the 49 active contracts, only one is concluded with a portfolio seller – QatarEnergy Trading’s 3.6 mtpa SPA with GAIL (2025–2030).

The remainder are long-term SPAs, predominantly on a DES basis, linking fixed volumes to designated buyers.

Split by buyer type, only 16.55 mtpa is contracted by portfolio buyers, compared to 89.33 mtpa held by other companies. The portfolio segment is dominated by Total and KOGAS, with smaller positions held by Shell, Eni and others. More importantly, destination flexibility remains limited: only 6.2 mtpa in the database is associated with unspecified destination clauses.

The non-portfolio segment is larger and more fragmented, with volumes concentrated among Chinese buyers and South Asian importers.

This structure implies that flexibility is not embedded in Qatari contracts. Adjustment must therefore take place outside the contractual framework.

Impact of Hormuz closure on importers of LNG from Qatar

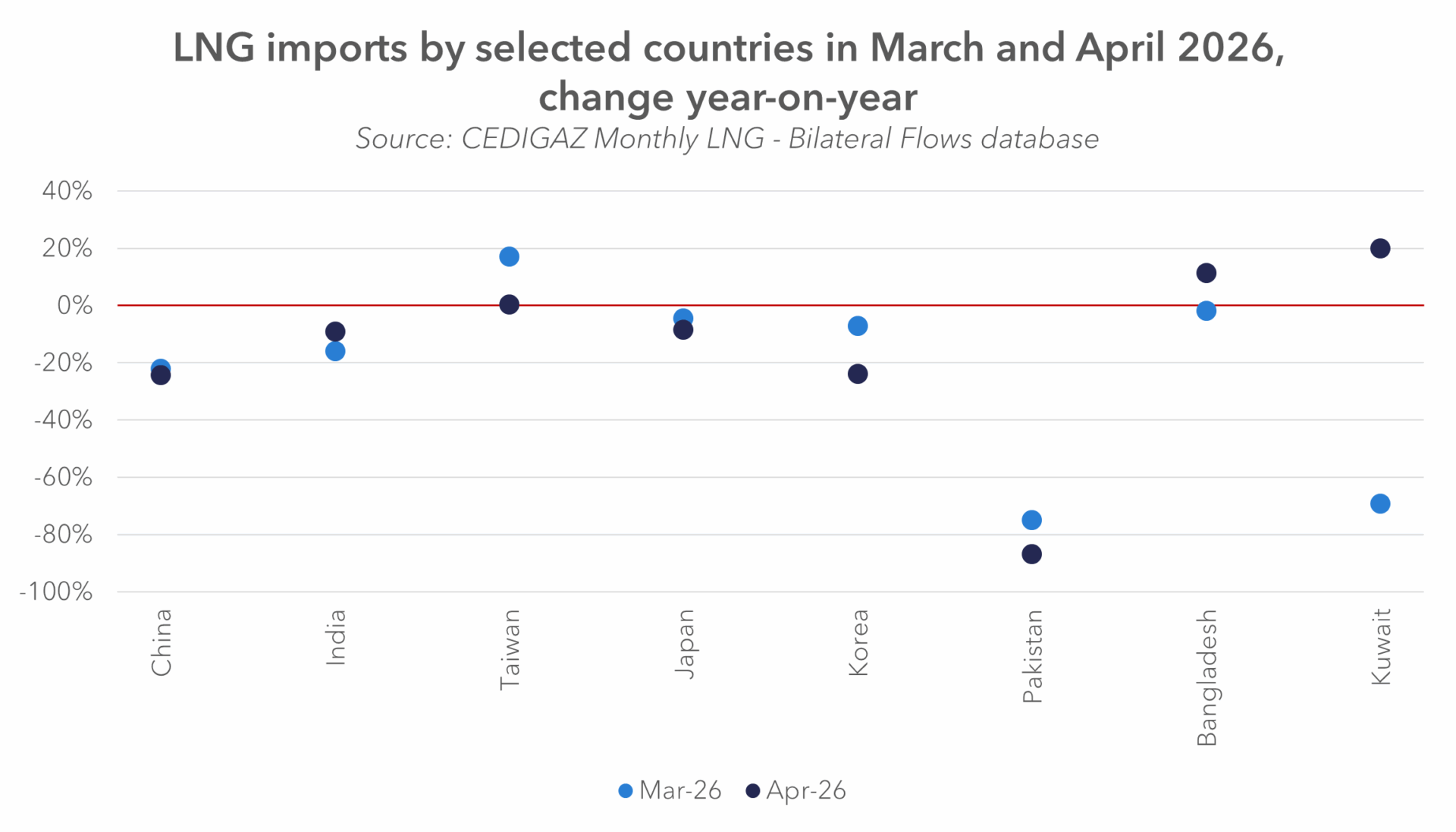

To assess the impact of the Hormuz closure on LNG importers, we use the Cedigaz Monthly LNG – Bilateral Flows Database. Across countries exposed to Qatari supply, monthly export volumes declined in March in all cases except Taiwan. In April, Bangladesh and Kuwait showed an upward trend relative to April 2025, while Taiwan’s imports remained stable year-on-year.

In the following sections, we will review the approaches of these importers.

Strategies to overcome supply disruption

China – state-controlled diversified buyers

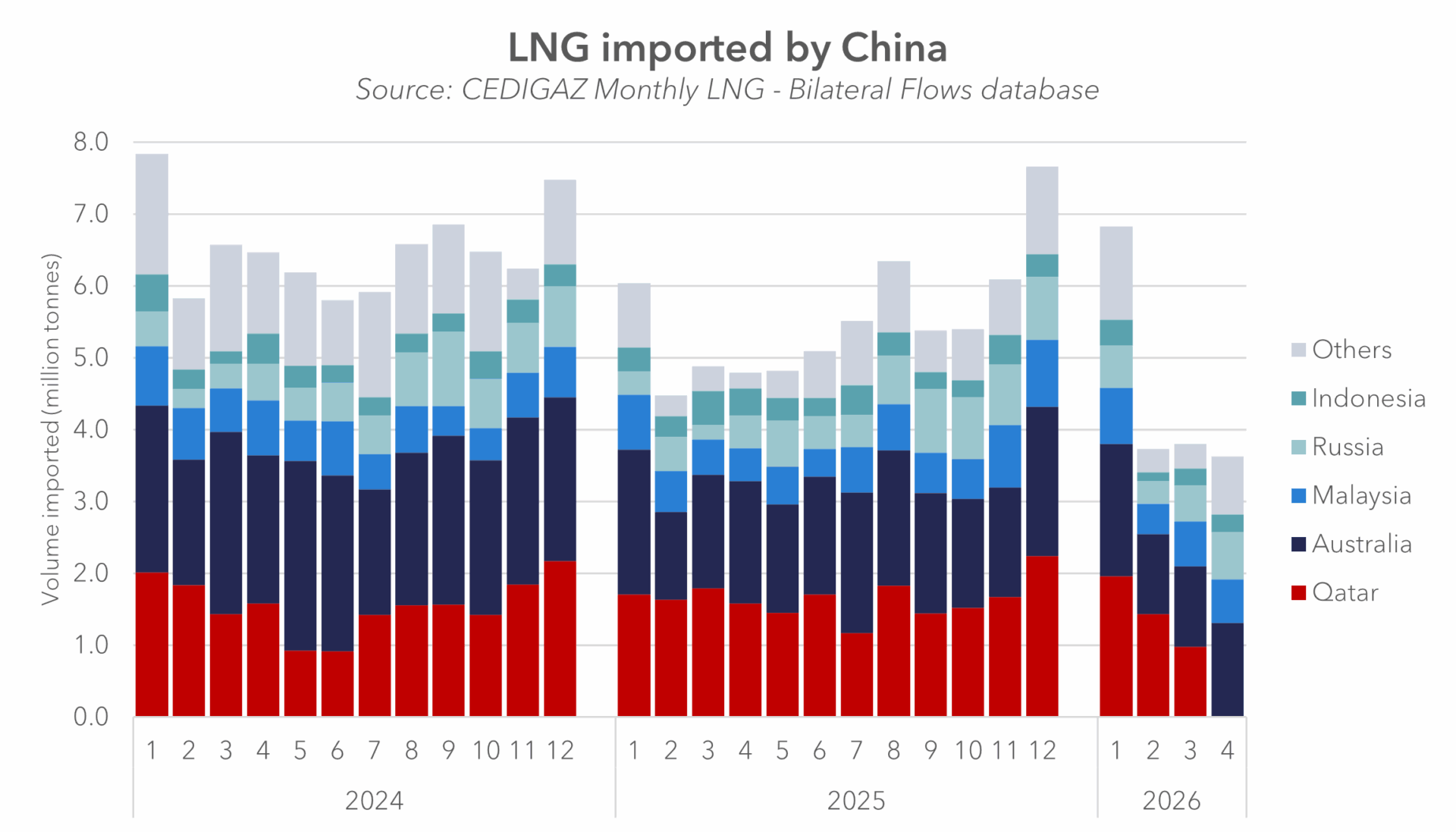

In China, supply disruption is absorbed at the system level. The response represents a state-coordinated buffering model. Importantly, Chinese imports were already very low in February and re-exports reached a record level in March. Reduced availability of LNG from Qatar (China’s second-largest source of LNG) increases the importance of alternative supply channels to China. In this setting, Russian pipeline deliveries, alongside existing LNG flows, provide a partial offset to lost volumes, limiting the need for additional LNG procurement on the spot market. While this does not eliminate the supply gap, it moderates the immediate demand response from China.

China also pre-empts LNG supply disruptions through system design. PetroChina maintains stable downstream pricing, effectively shielding end-users from global LNG volatility, while high inventory levels and a diversified supply base – including domestic production and pipeline imports – reduce reliance on spot procurement. With Qatari LNG accounting for a relatively small share of total consumption, disruptions can be managed through storage drawdowns and fuel substitution, limiting the need for market-driven adjustment. Sinopec’s equity participation in the North Field East expansion, combined with ultra-long-term contracts, reflects a strategy of embedding Chinese buyers within the supply base itself.

India – structurally short, price-sensitive system

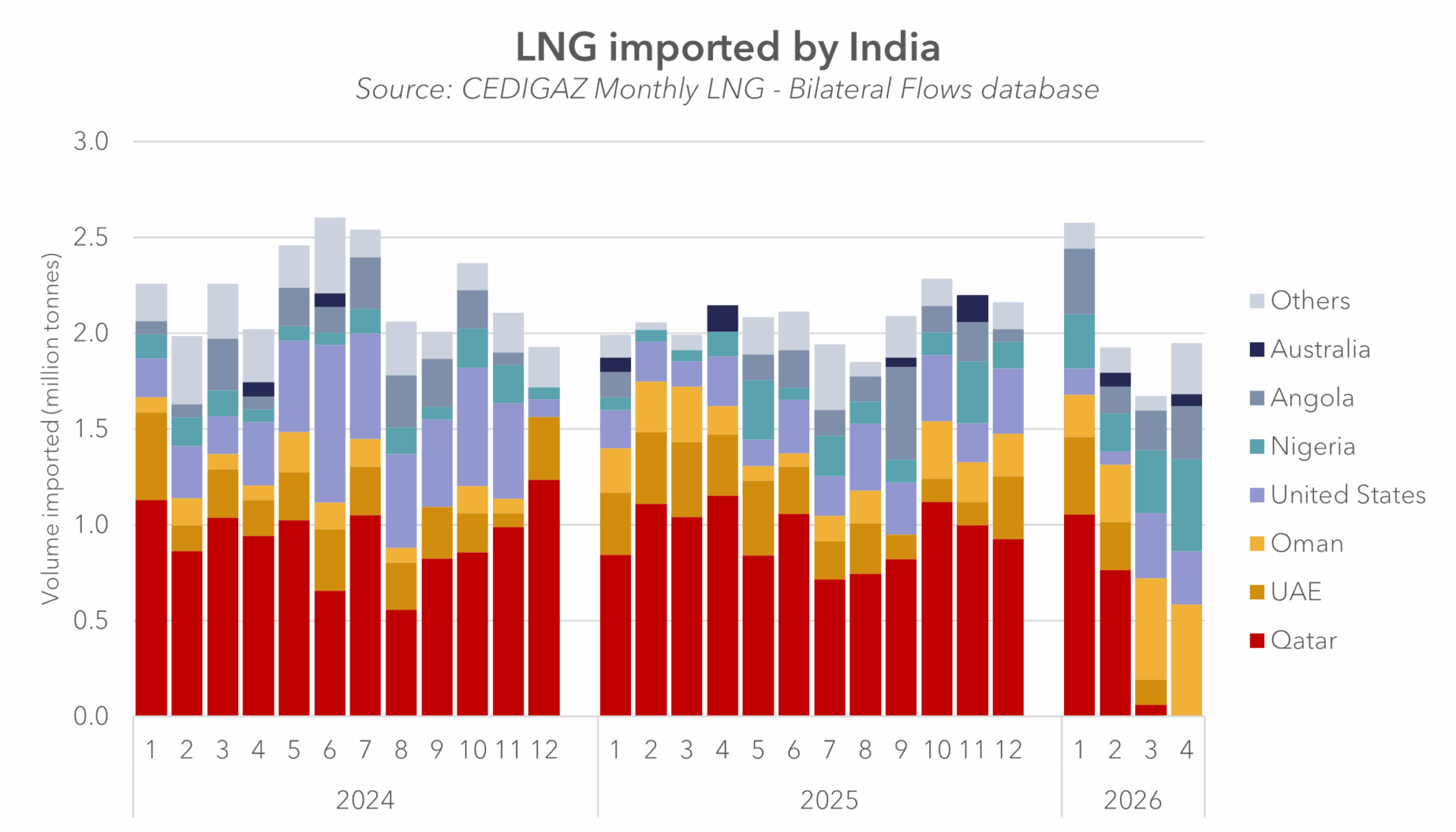

At first glance, India’s response to disruptions in Qatari LNG supply is primarily demand-side adjustment. Key importers such as Petronet LNG declared force majeure after cargoes were unable to load at Ras Laffan. This triggered a chain reaction across the domestic system, with supply constraints passed through to downstream users. Companies including GAIL, Indian Oil and Gujarat Gas reduced gas deliveries, particularly to industrial consumers. Curtailments have already affected fertiliser producers, indicating prioritisation across sectors, while households and transport have so far been shielded.

However, the data shows a more nuanced picture. Higher volumes are observed from alternative suppliers, including Oman, the United States, Nigeria and Angola.

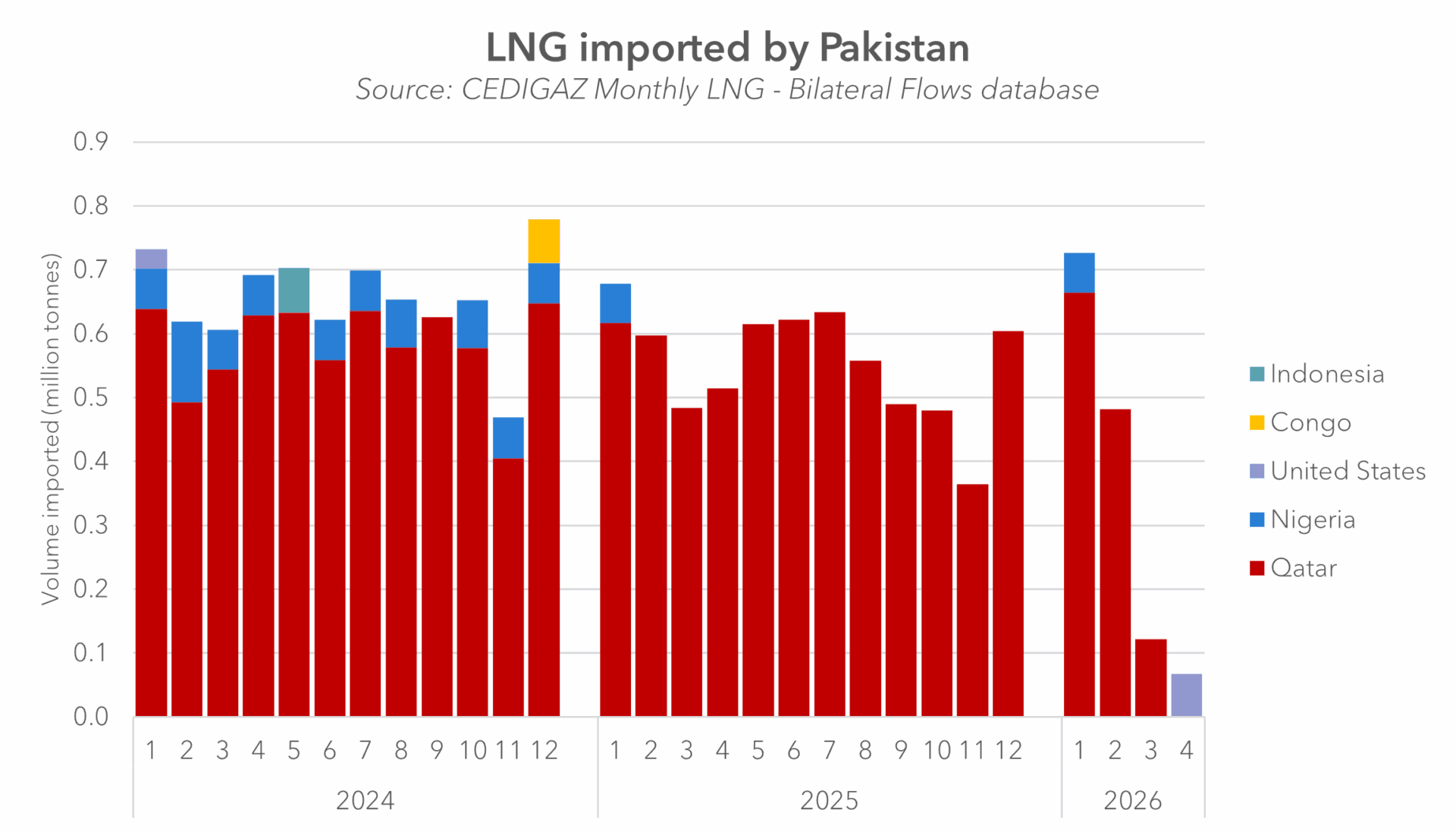

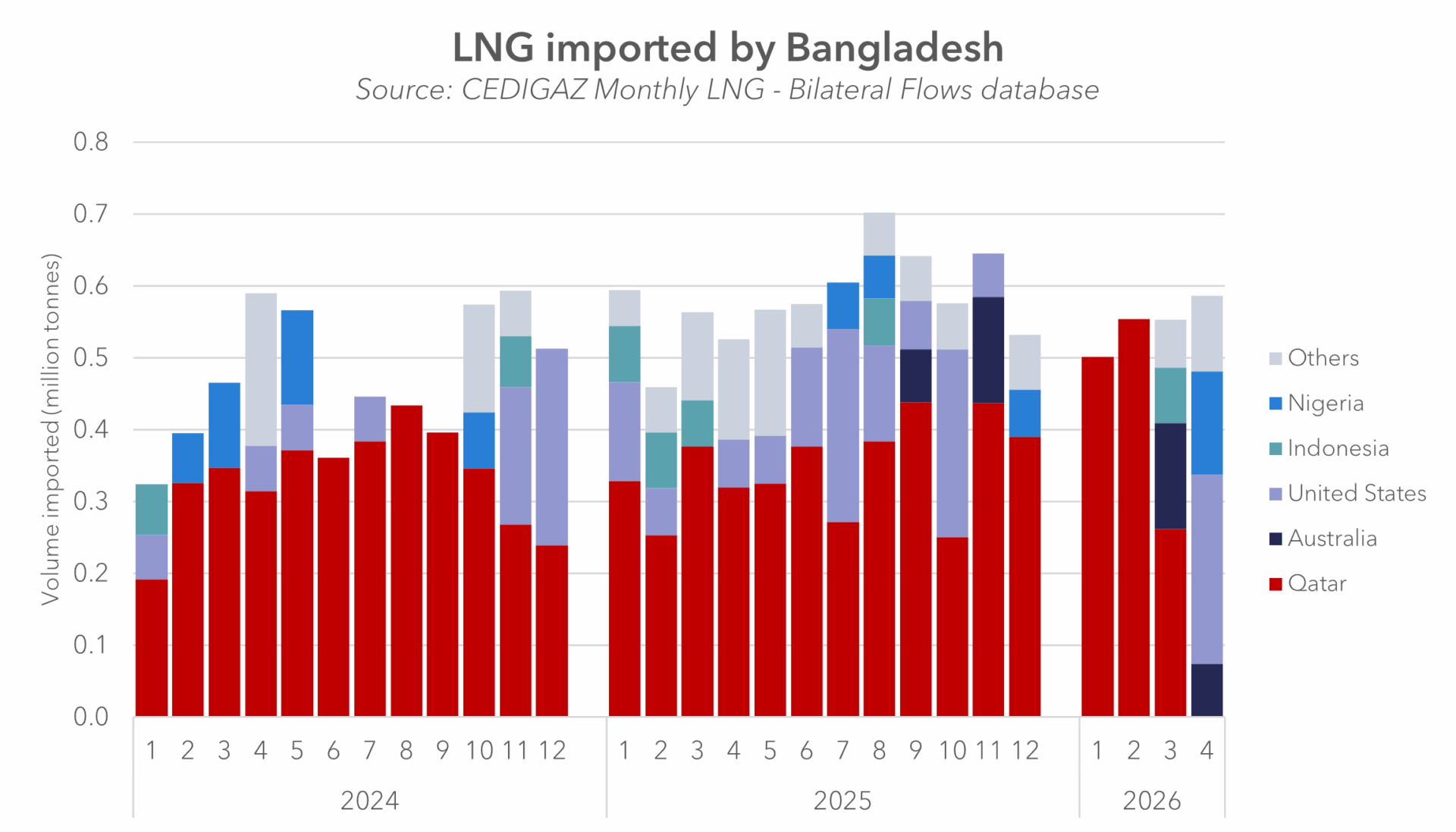

Pakistan & Bangladesh – constrained importers

While figures show an 89% decline in Qatari exports to Pakistan, the loss of supply was effectively complete since the beginning of the crisis until mid-May.

Pakistan is an interesting case, as it is commonly grouped among emerging Asian LNG markets and has long been one of the largest contributors within this group. In recent years, however, both import volumes and relative market share have declined. Pakistan’s share of the group’s imports fell from around 30% in 2020 to approximately 18% in 2025, and it moved from second to third place within the group, overtaken by Bangladesh.

The remaining LNG volumes have been supplied almost exclusively from Qatar.

In late 2025, Pakistan took a series of measures to reduce LNG imports, including cancelling and diverting contracted cargoes and preparing to resell surplus volumes on international markets.

In this context, the Middle East disruption coincides with Pakistan’s recent policy direction of reducing LNG imports. This is also reflected in the lack of response to proposals from SOCAR to supply portfolio LNG.

A major development in this context is the successful eastbound crossing of QatarEnergy’s Al Kharaitiyat through Hormuz on 9 May en route to Pakistan, reportedly under a limited arrangement between Pakistan and Iran covering selected LNG cargoes. Another tanker carrying Qatari gas, Mihzem, successfully went through the Strait of Hormuz on May 12.

Bangladesh, another major importer from the emerging Asia group, managed to secure alternative supplies.

The country’s power sector has undergone a rapid transition over the past decade. Domestic gas production, the longtime backbone of electricity generation, has stagnated as major gas fields mature. To bridge the supply gap, the government began importing LNG in 2018 through floating storage and regasification units at Moheshkhali. Since then, LNG has become an increasingly important component of the country’s energy mix.

Both Pakistan and Bangladesh are characterised by limited financial and infrastructure flexibility and high exposure to DES contracts. Their responses include difficulties in procuring spot cargoes, load shedding and demand curtailment, alongside reliance on government intervention. The outcomes, however, differ. Bangladesh was able to substitute a significant share of lost Qatari volumes through spot purchases, in some cases at prices two to three times higher than in December, while Pakistan has moved toward fuel switching and a limited arrangement with Iran covering selected LNG cargoes from Qatar.

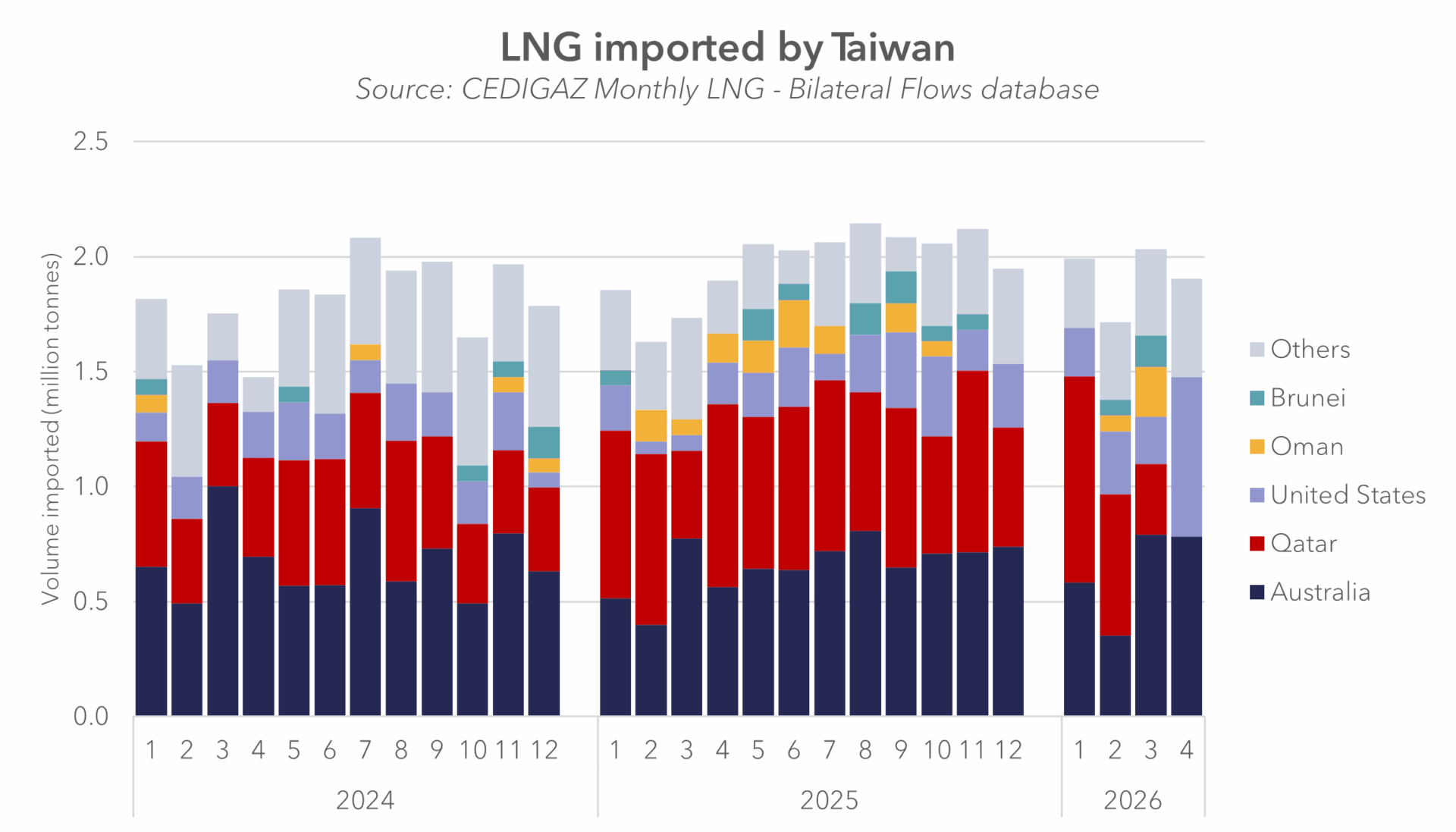

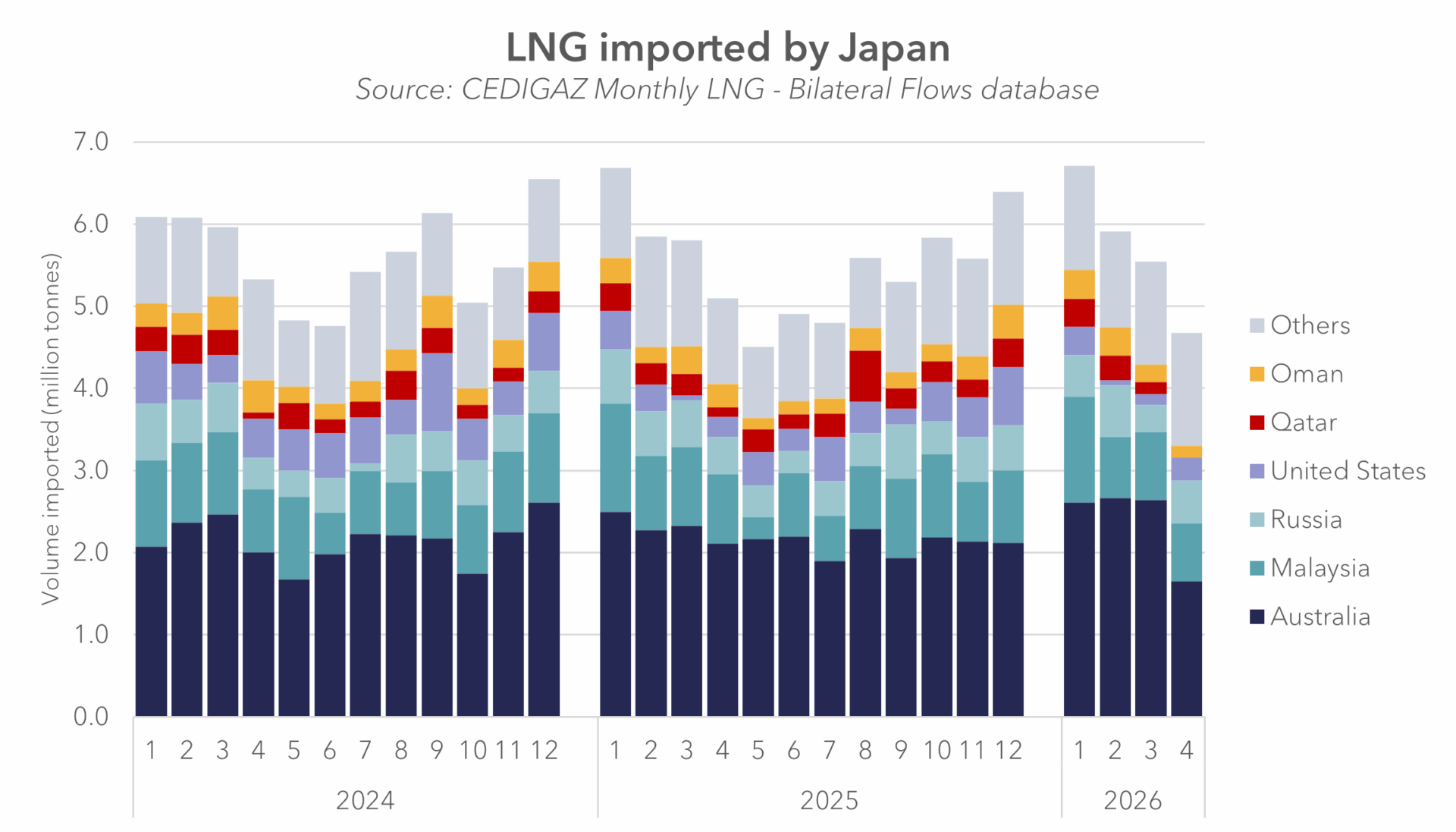

Taiwan, Korea and Japan – advanced portfolio optimization

Japan, South Korea and Taiwan represent mature LNG importing systems with well-developed infrastructure and diversified procurement strategies. While their contracts with Qatar remain largely rigid, these markets benefit from strong access to portfolio supply and alternative sources. This enables a high degree of system flexibility, allowing importers to manage disruptions through a combination of supply reallocation, portfolio optimisation and adjustments within the domestic energy mix.

Out of the three legacy LNG importers in Northeast Asia, Taiwan is the most exposed to loss of Qatari volumes. Taiwan’s response to disruptions in Qatari LNG supply is characterised by diversification and supply substitution. Imports from alternative suppliers, including the United States, Oman, Papua New Guinea and others, increased. Australia remained the dominant supplier and the main provider of additional supply.

Taiwan is strengthening procurement flexibility through new long-term contracts with US suppliers, alongside continued expansion of regasification capacity. Disruption management includes cargo rescheduling, regional reallocation within Asia and increased spot market procurement, supported by above-average inventory levels. This allows Taiwan to maintain supply continuity without resorting to demand curtailment. As a result, volumes of imported LNG have not declined.

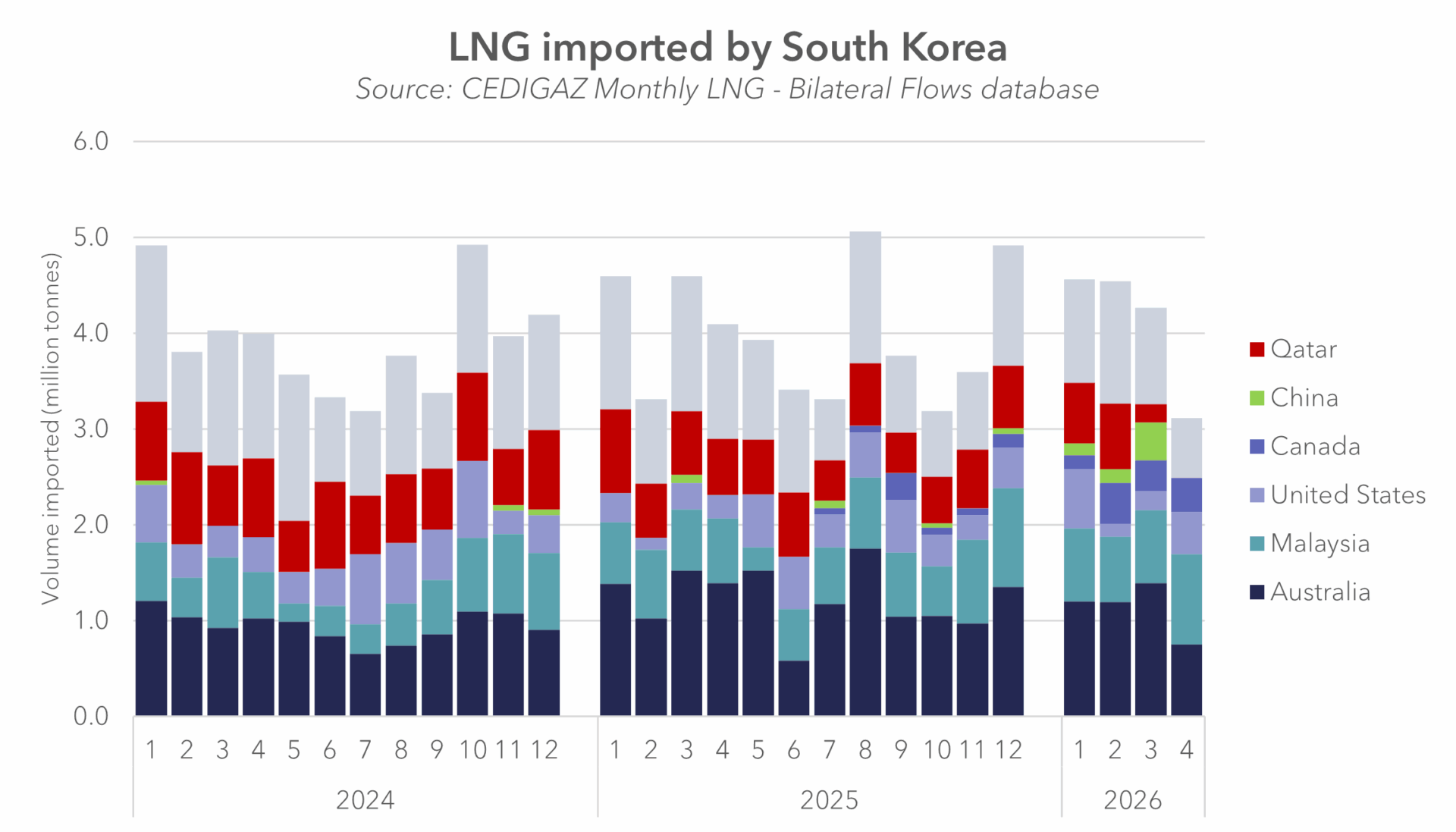

South Korea, the world’s third-largest LNG importer after China and Japan, uses gas across power generation, industry and heating. Qatar is Korea’s third-largest supplier after Australia and Malaysia.

In response to the Qatari supply disruption, the government has prioritised reducing reliance on gas-fired generation. Measures include increasing coal output, accelerating maintenance completion at nuclear reactors to raise utilisation, and lifting caps on coal-fired generation. Gas accounted for 27% of electricity generation in 2025, with the remainder largely supplied by coal, nuclear and renewables.

At the same time, South Korea is seeking alternative LNG supplies, combining fuel switching in the power sector with efforts to secure replacement cargoes.

Japan has not been substantially dependent on Qatari LNG, which accounts for a relatively small share of its overall import structure. Volumes imported by Japan declined noticeably year-on-year (–4% in March and –8% in April), comparable with the 4–6% share of Qatari LNG.

Japan reduced LNG imports in March 2026 primarily to manage high import costs, strengthen energy security amid volatility, and shift toward alternative energy sources. The decline was driven by increased nuclear generation and higher coal-fired output, as well as elevated inventory levels, which reduced the need for additional spot and prompt cargoes.

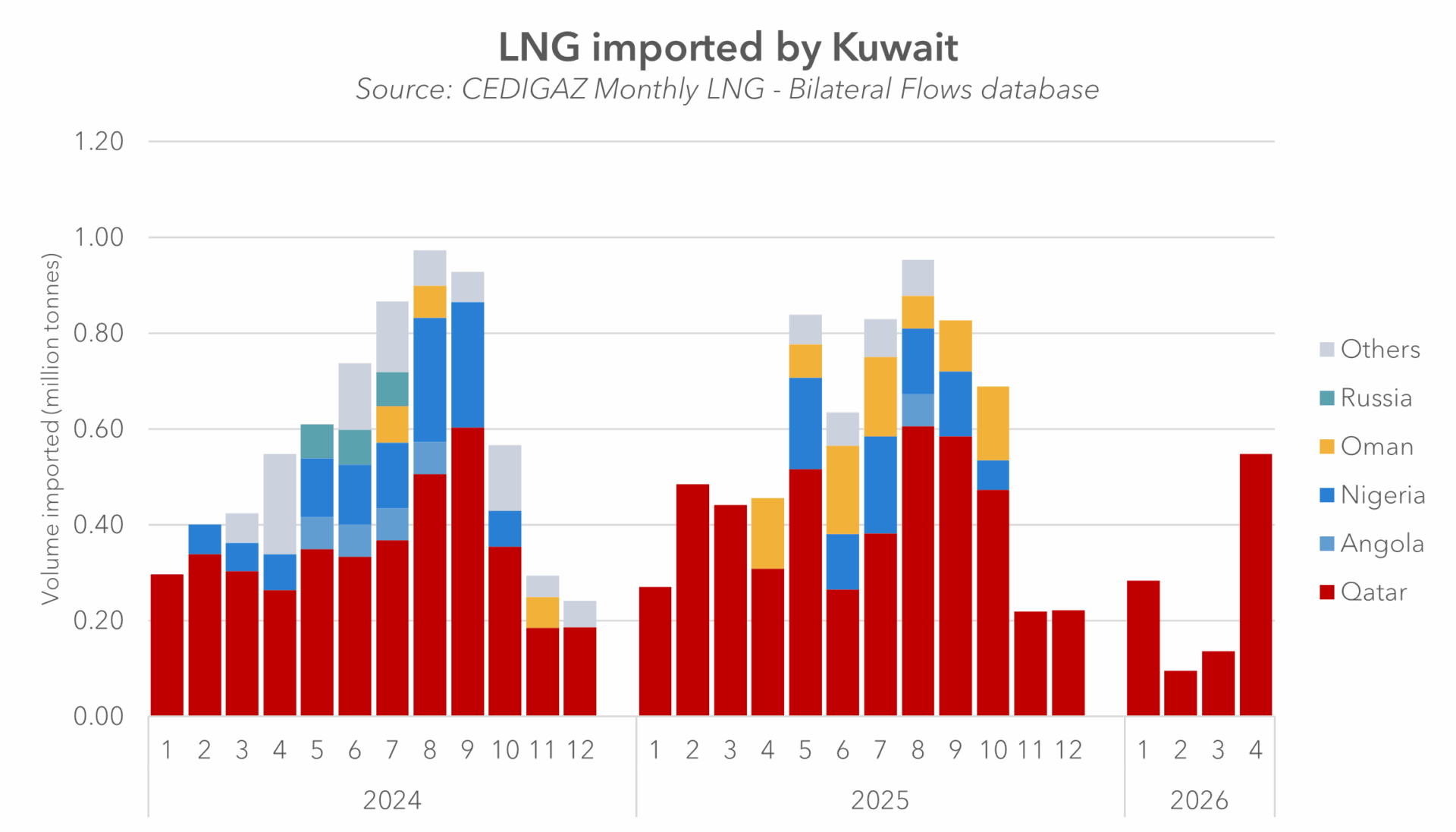

Kuwait – niche but strategic buyer

Kuwait still receives LNG from Qatar. In April, it was the only country Qatar exported LNG to. However, the disruption is constraining LNG imports from other sources as well as domestic gas availability. Reduced crude oil production – implemented by Kuwait Petroleum Corporation due to shipping risks – is likely to lower associated gas supply to the power sector. While some power plants can switch to fuel oil, this comes with lower efficiency and operational challenges, suggesting that the system can absorb the shock only partially.

Kuwait’s position within the Gulf system means limited access to alternative supply routes, contributing to the sharp decline in cargoes loaded toward this buyer. This also highlights the exposure of emerging LNG importers in the region. In Iraq, the start-up of its first LNG import terminal at Khor al-Zubair has been delayed.

Conclusion

Qatari LNG contracts are characterized by limited flexibility embedded in contract terms. As a result, adjustment to supply disruption takes place at the level of the importing system.

Responses differ across markets. China absorbs disruption through system-level buffers. India combines demand curtailment with partial substitution. Taiwan, Japan and Korea rely on diversified supply and domestic energy system flexibility. Pakistan and Bangladesh face more constrained options, with outcomes ranging from substitution to demand reduction.