By Irina Mironova for Cedigaz

Recent attacks on Qatar’s LNG infrastructure have taken two liquefaction trains out of service, removing approximately 12.8 mtpa (~17% of Qatar’s capacity) for an estimated three to five years.

This development intensifies the disruption seen in recent weeks, centred on the effective closure of the Strait of Hormuz, which normally carries around 20% of global LNG trade. Maritime constraints have already translated into both physical supply losses and logistical bottlenecks, with LNG carriers unable to exit the Gulf and export flows significantly constrained.

The crisis has now shifted into a structural supply loss, extending beyond the short-term disruption scenarios considered earlier.

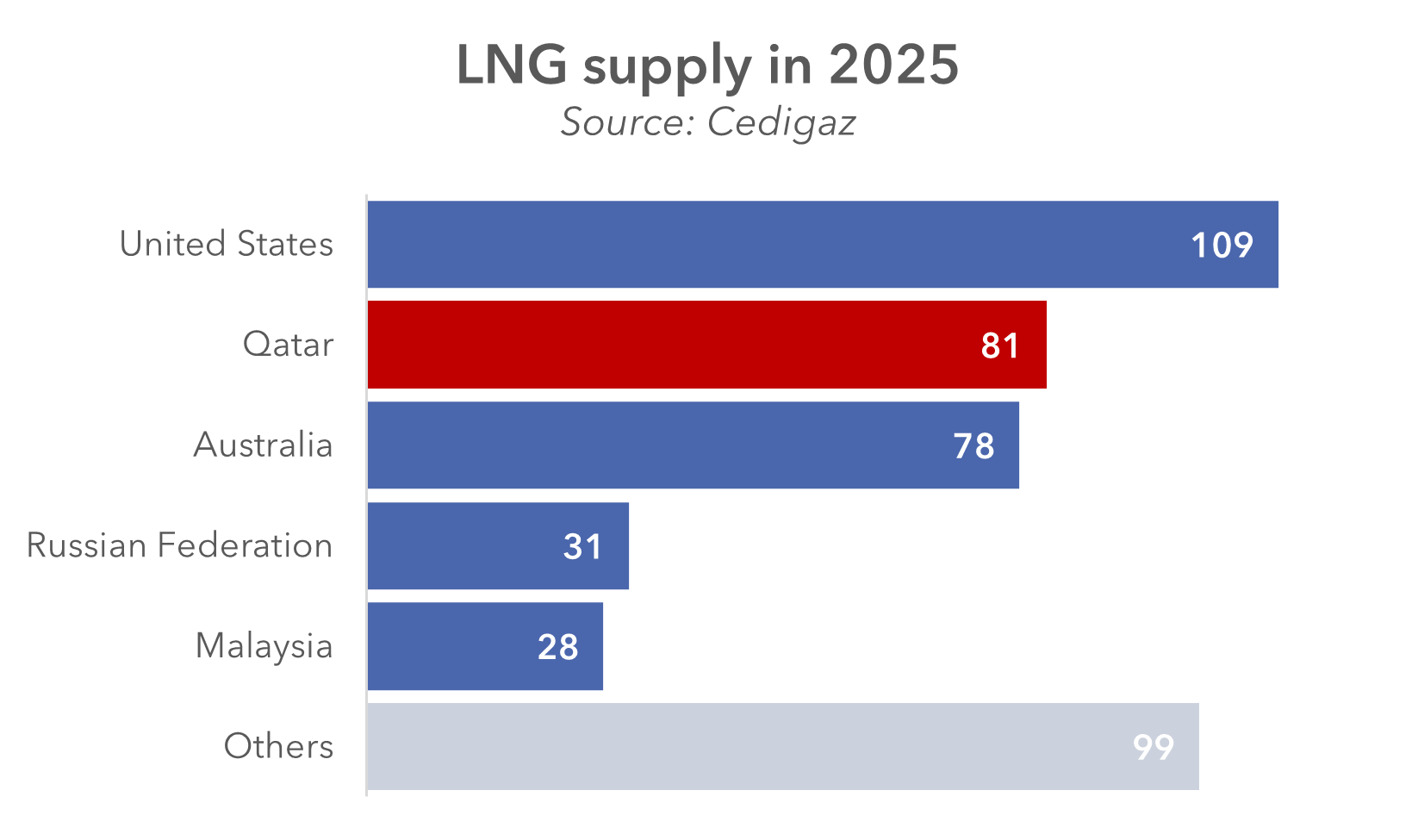

LNG supply as of early 2026

Global LNG supply reached approximately 426–429 Mt in 2025, reflecting the strongest annual growth since 2022 and supported primarily by new North American capacity. Headline utilisation is around 80–85% of nameplate liquefaction capacity. This may appear moderate, but effective available capacity is much tighter (~95–97%), as outages, feedgas constraints and maintenance reduce usable supply.

This implies that despite expectations of an emerging supply wave prior to the crisis, the system actually entered 2026 with very limited spare capacity. Existing liquefaction infrastructure is operating at or near full utilisation, and most volumes are tied to long-term contracts. In the United States in particular, export facilities are effectively running at full capacity, with no idle volumes that can be activated in response to the disruption.

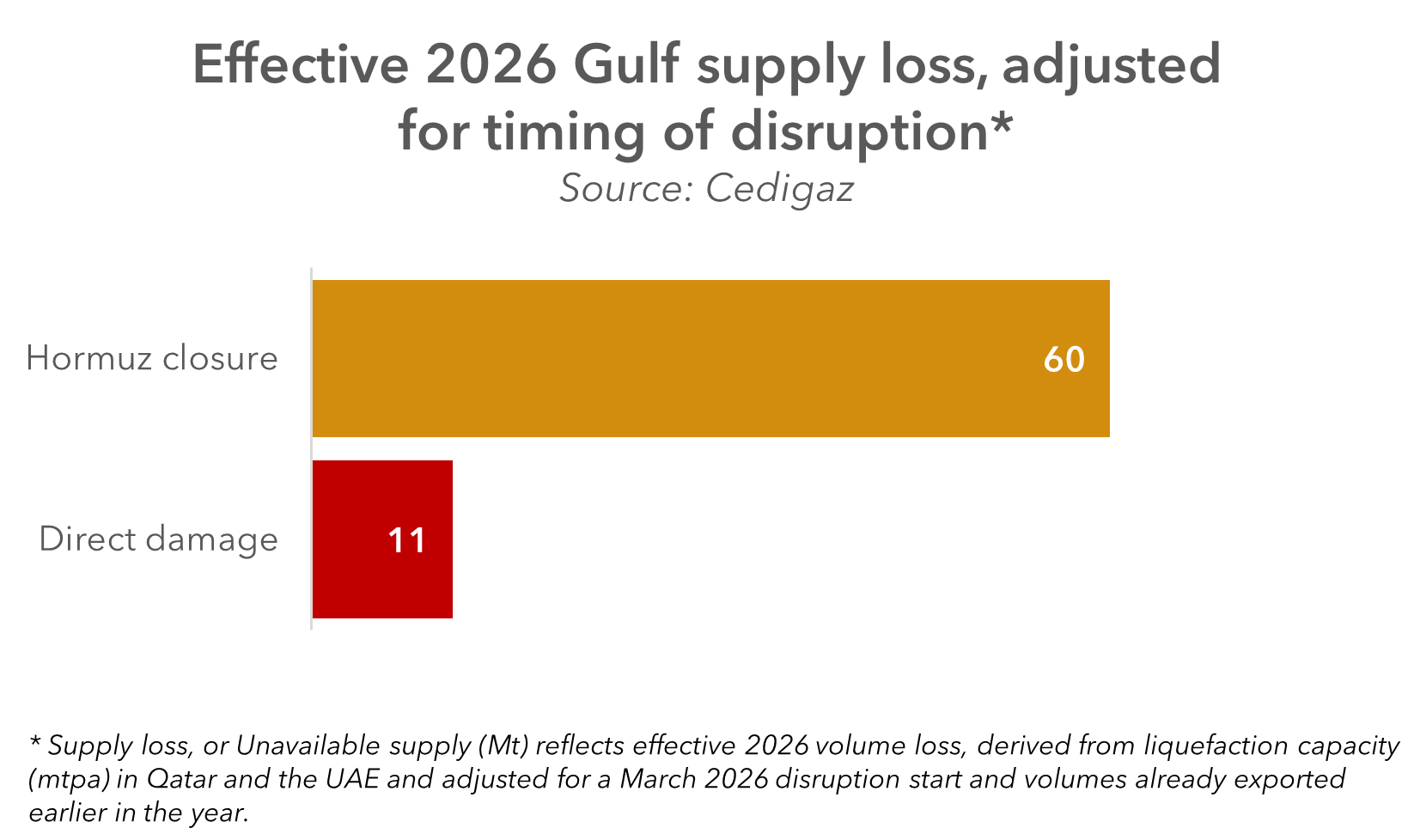

Effective supply loss from Gulf crisis

What supply is lost in the Gulf crisis in 2026? Unavailable supply (Mt) reflects the effective volume loss over the year, derived from liquefaction capacity (mtpa) in Qatar and the UAE and adjusted for a March 2026 disruption start, as well as volumes already exported earlier in the year. On this basis, the loss is estimated at around 71 Mt. This includes nearly 80 mtpa of Qatari capacity and around 6 mtpa in the UAE, adjusted to exclude volumes exported in January and February.

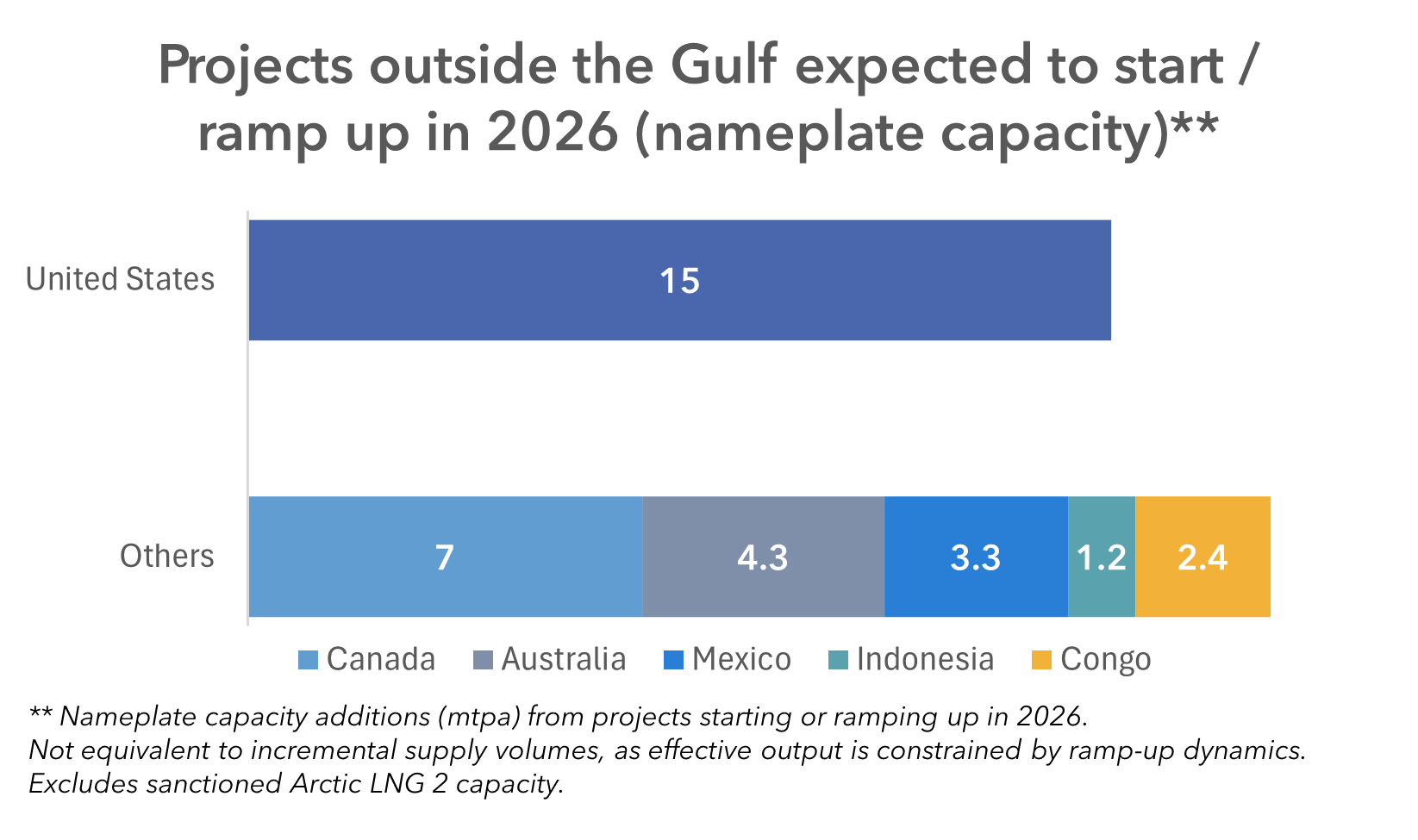

New supply

The system does add supply in 2026, with approximately 35 Mt of nameplate capacity expected to come online outside the Gulf. These figures reflect projects starting or ramping up during the year (not incremental supply volumes, as effective output is determined by ramp-up dynamics). Sanctioned Arctic LNG 2 capacity is excluded.

Around three quarters of these additions are concentrated in the Americas. A significant share reflects ramp-ups and phased developments such as LNG Canada, as well as staged train additions at Corpus Christi and Golden Pass.

Importantly, this figure would have been higher, as earlier expectations included more than 30 mtpa of additional supply from Qatar, which is no longer expected to come online.