By Irina Mironova for Cedigaz

Qatar’s LNG system has been materially disrupted following the escalation in the Middle East after February 28, 2026. The closure of the Strait of Hormuz and direct attacks on energy infrastructure have cut off export flows and constrained production.

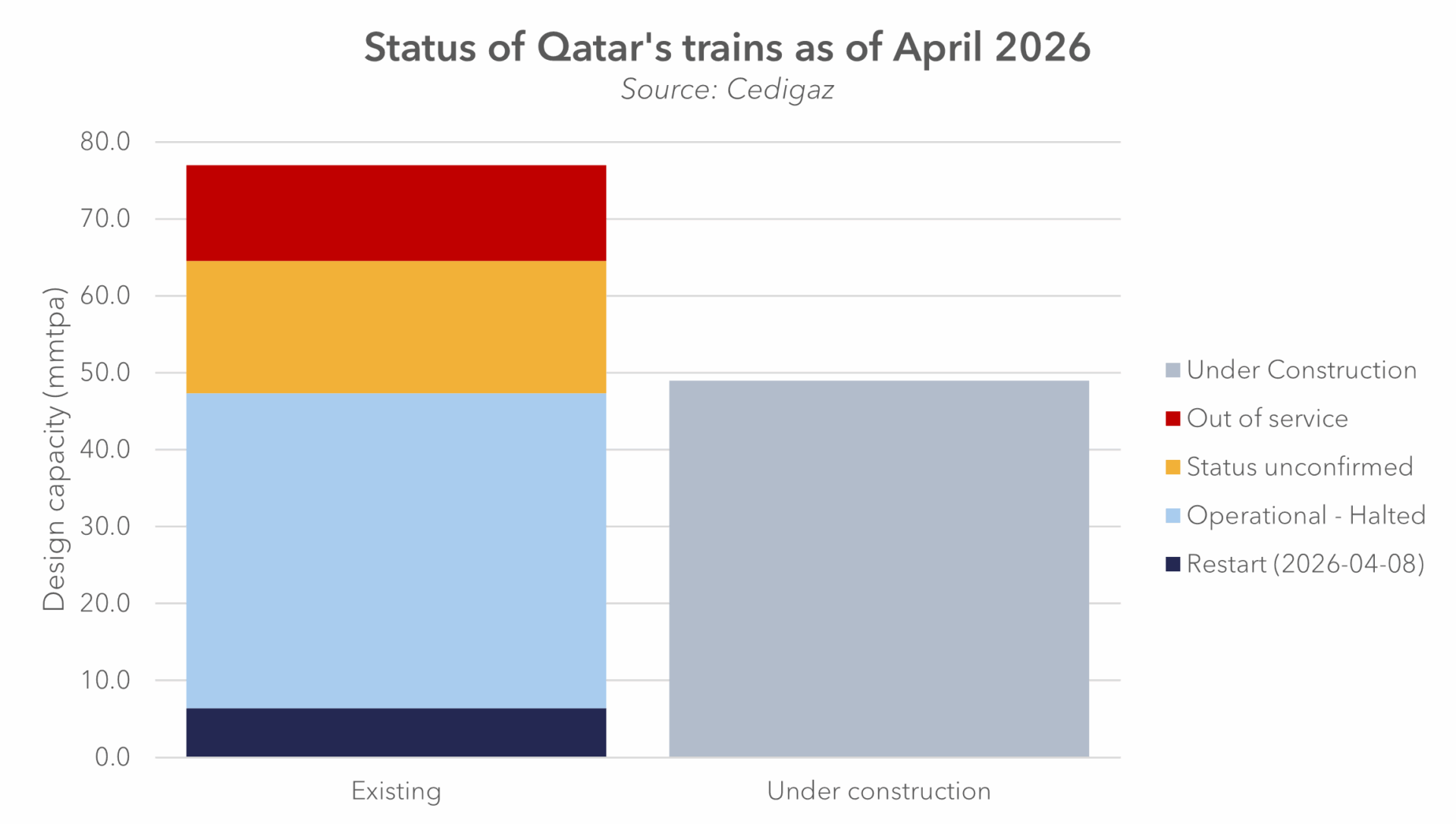

Status update on Qatari capacity

At the liquefaction level, two trains (QELNG South 2 Train 4 and QELNG South 3 Train 6) have been taken out of service, removing approximately 12.8 mtpa – around 17% of Qatar’s capacity. The damage involves critical components such as main cryogenic heat exchangers, implying long lead times for replacement and extended outages of at least three years, and potentially up to five. QatarEnergy estimates the impact at around $20 billion per year in lost revenue.

Across the broader system, the status of several trains remains uncertain.

All operational trains were halted in the early phase of the crisis in March. Confirmed outages include QELNG South Train 4 (4.7 mtpa), which affects supplies to Edison and EDFT, and Train 6 (7.8 mtpa), which impacts KOGAS, EDFT, and Shell in China. The status of adjacent trains (T3, T7, T5) remains uncertain (“status unconfirmed” in the figure above). While no visible damage has been reported, inspections will be required to determine whether the explosions have affected their operational integrity.

Despite these constraints, there are initial signs of operational recovery. QatarEnergy has begun restarting liquefaction, with two out of three trains at QELNG North 1 returning to operation on April 8. This facility, with a combined capacity of around 10 mtpa, represents the first step toward restoring output.

However, a return to full production remains contingent on export routes reopening.

Status update on vessels and Hormuz transit

Shipping constraints remain the dominant limitation. No LNG carrier has successfully transited the Strait of Hormuz since the escalation began. Several vessels approached the strait in early April but reversed course and returned toward the Gulf. This includes cargoes that had been loaded prior to the disruption, which remain largely stranded within the region.

By April 10, all Qatari LNG cargo outside the Strait arrived at their destinations, no Qatari cargoes remain in the global market outside the Gulf. The last cargo to Asia was delivered to China on March 20, with subsequent deliveries concentrated in Europe and concluding on April 10 with UK’s South Hook.

Loaded Qatari LNG tankers approached the strait in what would be the first outbound LNG transits since late February (Al Ghashamiya, Lebrethah, Fuwairit, Rasheeda and Disha). But they are still west of Hormuz as of April 22, while the situation seems to be on way to deterioration.

How much volumes have been lost to the market so far?

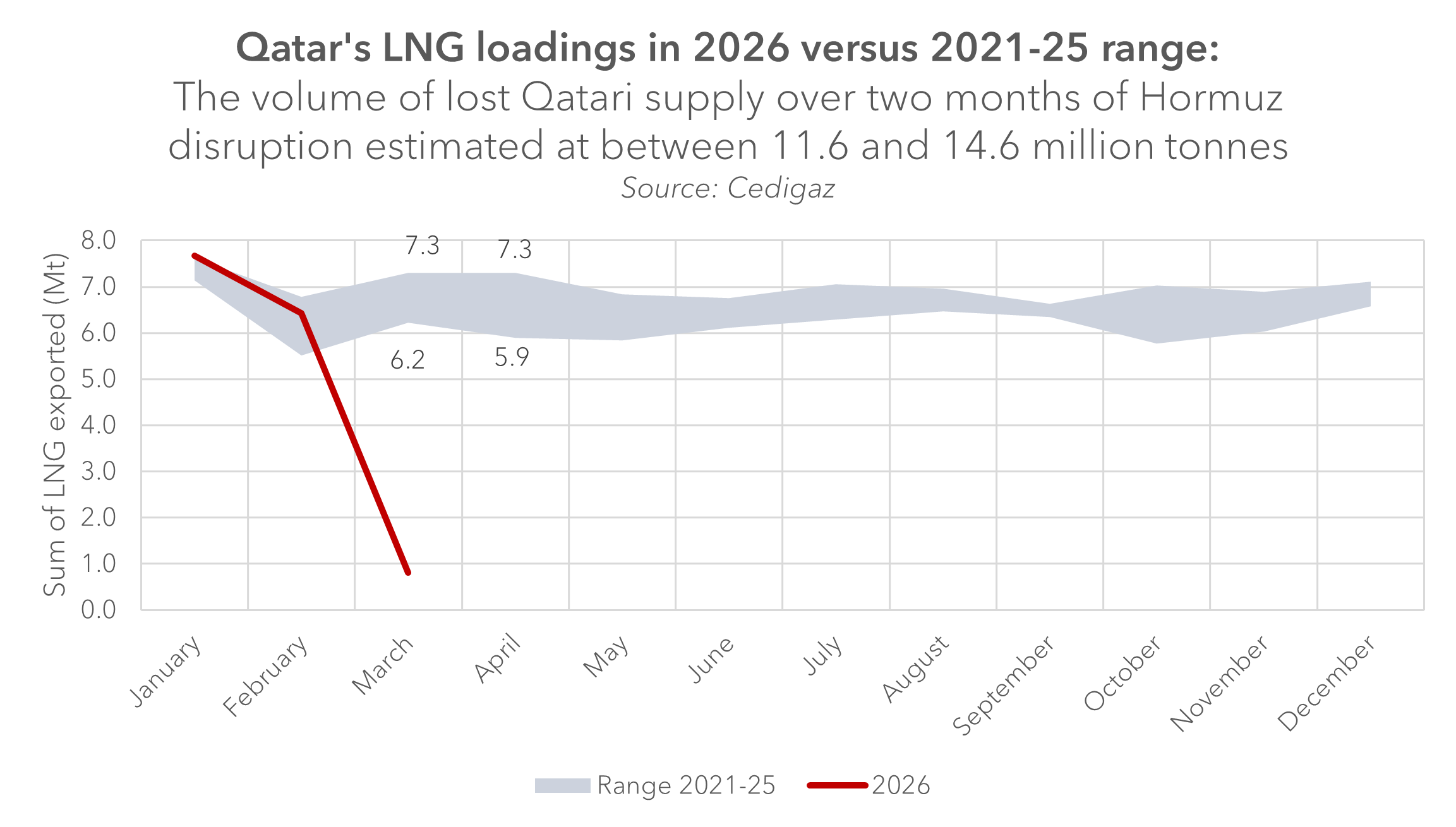

According to Cedigaz Monthly LNG – Bilateral Flows data, Qatar typically exports between 5.8 and 7.3 million tonnes of LNG per month. In March 2026, only four cargoes were loaded, with a combined volume of around 0.8 million tonnes. Of these, one cargo was delivered to Kuwait, while the others remained idle within the Gulf.

Based on export patterns observed over the previous five years, the volume of lost Qatari supply over two months of disruption at Hormuz can therefore be estimated at between 11.6 and 14.6 million tonnes.

What are the perspectives?

There remains some capacity to mitigate part of the supply loss. Of the installed capacity remaining after the attacks (65 mtpa if we add the trains with unconfirmed status), a combination of deferred maintenance and operational optimisation could lift effective production to around 70 mtpa. According to industry expert estimates, this level could be reached over an 18-month period following the reopening of the Strait.

At the same time, the disruption is beginning to affect forward supply. Expansion projects (Trains 8–13, with capacities of around 8–8.25 mtpa each) remain under construction, with initial timelines targeting completion from 2026 to 2027. These schedules (already revised in February 2026) are now exposed to further delays as contractors reassess site access and execution timelines.

The system remains constrained by two factors: the physical loss of liquefaction capacity and the continued restriction on exports through the Strait of Hormuz. Until both are resolved, Qatar’s LNG system will remain below effective capacity and disconnected from global markets.