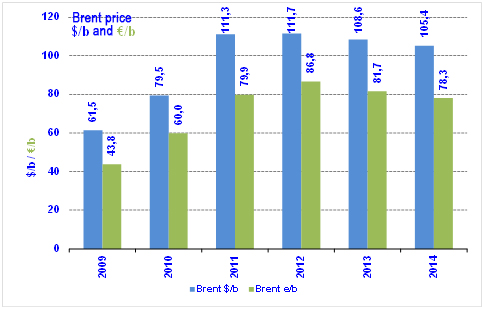

Brent: shrinkage anticipated in 2014

Since the beginning of the year, Brent has varied between $98/B (September) and $115/B (at the beginning of June), which is fairly close to the extremes seen in 2013. The anticipated average for 2014, which has fluctuated between $105 and $110/B, is currently situated at $105/B, slightly down on 2013 ($108.60/B). Movements the price of Brent remain highly uncertain in the light of possible influencing factors: whether or not there is an increase in exports from Libya; whether or not negotiations with Iran on nuclear power are successful (deadline postponed to 24 November); whether or not the insurgents in Iraq affect production and exports in the south of the country; whether or not the tension in Ukraine escalates; the dollar exchange rate (increasing against the Euro since May, a factor depressing the oil price); the global economic climate (increased growth expected in 2015) and the outlook for the stock exchanges. The field of factors affecting the price of Brent is therefore obviously very wide. In any case, the increase in US production due to shale oil is playing a moderating role and partly explains the slight decline experienced since 2012.

Since the beginning of the year, Brent has varied between $98/B (September) and $115/B (at the beginning of June), which is fairly close to the extremes seen in 2013. The anticipated average for 2014, which has fluctuated between $105 and $110/B, is currently situated at $105/B, slightly down on 2013 ($108.60/B). Movements the price of Brent remain highly uncertain in the light of possible influencing factors: whether or not there is an increase in exports from Libya; whether or not negotiations with Iran on nuclear power are successful (deadline postponed to 24 November); whether or not the insurgents in Iraq affect production and exports in the south of the country; whether or not the tension in Ukraine escalates; the dollar exchange rate (increasing against the Euro since May, a factor depressing the oil price); the global economic climate (increased growth expected in 2015) and the outlook for the stock exchanges. The field of factors affecting the price of Brent is therefore obviously very wide. In any case, the increase in US production due to shale oil is playing a moderating role and partly explains the slight decline experienced since 2012.