The last 14 months since the Cedigaz long-term-contracts database (1) was last updated has shown a continuation of the wave of renegotiations that has gained momentum since 2010, recently culminating with the announcement by ENI of its agreement with Gazprom. The deal, which reduces both the price and take-or-pay obligation of contracted gas, has been hailed by the gas community has signaling a move away from oil-indexation by the Russian gas giant. Based on ENI’s declarations some analysts contend that the gas is now 100% hub indexed. According to Argus Media, the actual arrangement is more subtle, the pricing formula would still be oil-based but would include a price corridor based on TTF prices.

Natural Gas Prices - Page 18

International Gas Prices – June 6, 2014

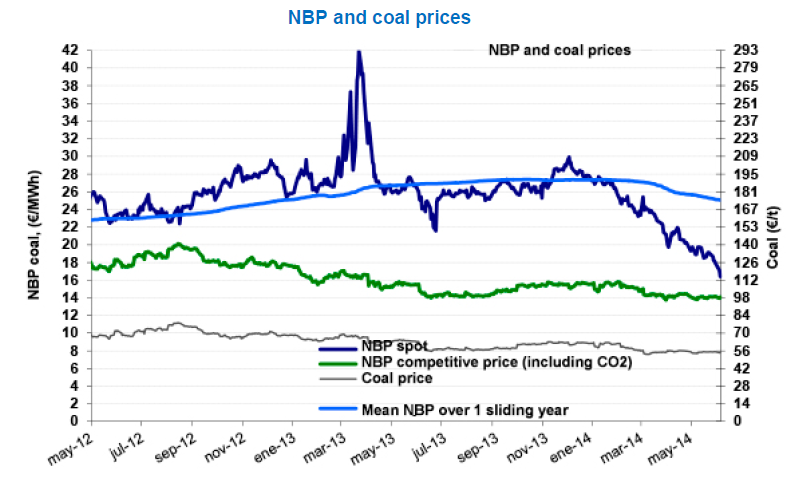

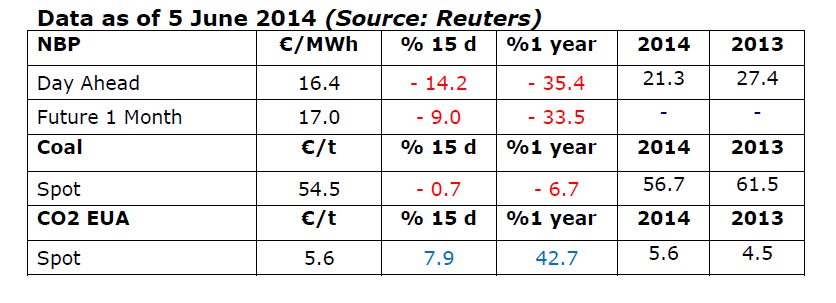

NBP: 8% fall in two days

The fall in the price of NBP which began in December (-45%!) is continuing (an 8% fall in May compared with the previous month) and even picked up the pace in June: an 8% fall between 30 May and the current €16.4/MWh (US$6.5/MBtu) listings. This means that the price of NBP is approaching the competitive price for coal – an estimated €14/MWh (US$5.6/MBtu) based on a level of €55/tonne for coal (€61/tonne in 2013) and €5.4/tonne for CO2. This price correction can be attributed to several factors, including the extension granted until 10 June to find an agreement on the Ukrainian crisis, but mainly to the UK market context. Demand is moderate (71 Gm3 over a

The fall in the price of NBP which began in December (-45%!) is continuing (an 8% fall in May compared with the previous month) and even picked up the pace in June: an 8% fall between 30 May and the current €16.4/MWh (US$6.5/MBtu) listings. This means that the price of NBP is approaching the competitive price for coal – an estimated €14/MWh (US$5.6/MBtu) based on a level of €55/tonne for coal (€61/tonne in 2013) and €5.4/tonne for CO2. This price correction can be attributed to several factors, including the extension granted until 10 June to find an agreement on the Ukrainian crisis, but mainly to the UK market context. Demand is moderate (71 Gm3 over a  sliding year as opposed to 80 Gm3 12 months ago), temperatures are rising, stocks are high as they are on the continent, and sales of LNG have been sustained since the end of March (40/50 mcmd – 20/25% of demand). Overall, the LNG market is unaffected by tensions, with prices in Asia of under US$13/MBtu, as opposed to US$20 in February. The shoring up of Norwegian deliveries at the end of May via the “Langeled” gas pipeline should also be mentioned among the economic factors. The imminent closure for maintenance (11 to 26 June) of the Interconnector, which is currently used to transit 30 mcmd to the continent, is also a factor pushing prices down (down to €14/MWh, or US$5.6/MBtu?). And the downward trend of oil price indexation in contracts (which encourages spot gas prices to respond in a more marked way to supply/demand balance) should also be highlighted. This is a structural movement in Europe (ENI/Gazprom agreement in May based on the market, 60% of spot prices referenced in France) that is in the process of affecting Asia.

sliding year as opposed to 80 Gm3 12 months ago), temperatures are rising, stocks are high as they are on the continent, and sales of LNG have been sustained since the end of March (40/50 mcmd – 20/25% of demand). Overall, the LNG market is unaffected by tensions, with prices in Asia of under US$13/MBtu, as opposed to US$20 in February. The shoring up of Norwegian deliveries at the end of May via the “Langeled” gas pipeline should also be mentioned among the economic factors. The imminent closure for maintenance (11 to 26 June) of the Interconnector, which is currently used to transit 30 mcmd to the continent, is also a factor pushing prices down (down to €14/MWh, or US$5.6/MBtu?). And the downward trend of oil price indexation in contracts (which encourages spot gas prices to respond in a more marked way to supply/demand balance) should also be highlighted. This is a structural movement in Europe (ENI/Gazprom agreement in May based on the market, 60% of spot prices referenced in France) that is in the process of affecting Asia.

Putting a price on gas or Putin’s gas price?

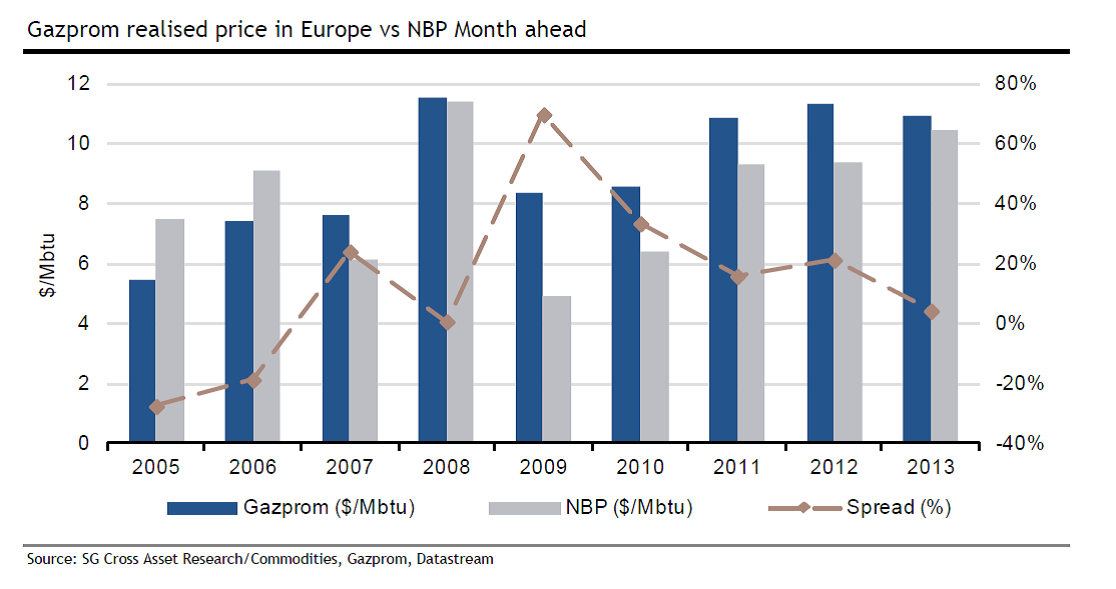

By avoiding pushing too much volume, Gazprom/Russia and Statoil/Norway not only avoided a price war in 2011-2013 but managed to reset spot prices at a level that is acceptable to them.

Higher prices were leading to permanent demand destruction. Russia is not willing to boost European gas demand for power generation at a price that it considers too low. As even with no growth in demand, Gazprom’s volumes are rising to mitigate the decline in European gas production.

So why has Gazprom provided additional volumes to Europe at the expense of prices, that went down by 40% since end-2013? Higher prices were also leading to the development of alternative supply. With the Final Investment Decision (FID) in December 2013 for Shah Deniz 2 in Azerbaijan and a long list of potential LNG projects in North America, Russia could see the threat of new suppliers/competitors entering the European market after 2020e.