By Irina Mironova for Cedigaz

Recent months have seen extensive reporting on Russia’s oil “shadow fleet.” This prompted a parallel review of the LNG shipping segment: does a comparable structure exist in LNG, and what does the actual fleet engaged in transporting Russian LNG look like?

The result is a dedicated database compiled for Cedigaz subscribers, covering vessels directly or indirectly involved in transporting LNG from Yamal LNG, Sakhalin LNG and Arctic LNG-2, as well as vessels participating in transshipment operations.

Data sources

The database combines information from:

- IGU World LNG Report 2025 (Owner, shipyard, capacity data)

- Appendix 3: Global active LNG fleet

- Appendix 4: Global LNG vessel orderbook

- VesselFinder (General vessel characteristics, AIS-based port calls, flag history, sanctions indicators)

In addition, qualitative vessel selection was informed by analysis of LNG flows from Yamal LNG and transshipment patterns, using publicly available reporting, including:

- Overview of LNG exports from Yamal LNG (January–May 2025)

- Update on LNG exports (June–

August 2025) - Reporting on ship-to-ship transfers in the Barents Sea

- Coverage of vessel movements linked to Arctic LNG trade

- Analysis of regulatory loopholes affecting LNG shipping

Vessel selection criteria

The fleet list was constructed through qualitative analysis of:

- Direct departures from Sabetta

- Participation in ship-to-ship transfers near Kildin Island

- Recurring presence in Arctic-linked LNG flows

- Ownership and registry r

- estructuring patterns

- Sanctions exposure

The aim was to identify vessels demonstrably engaged in the transport of Russian LNG, either as project-dedicated carriers (Arc7), seasonal ice-class support (Arc4), or conventional LNG carriers integrated into the Arctic-linked logistics system.

Fleet size

Based on this methodology, the Russia-linked LNG transport system currently consists of approximately:

- 60+ LNG carriers in total

- 50+ operational vessels

- 14 vessels under construction

This figure includes dedicated Arctic carriers, newly built intermediate tonnage, conventional LNG carriers repositioned into Russian trade, and vessels under construction for Arctic LNG-2.

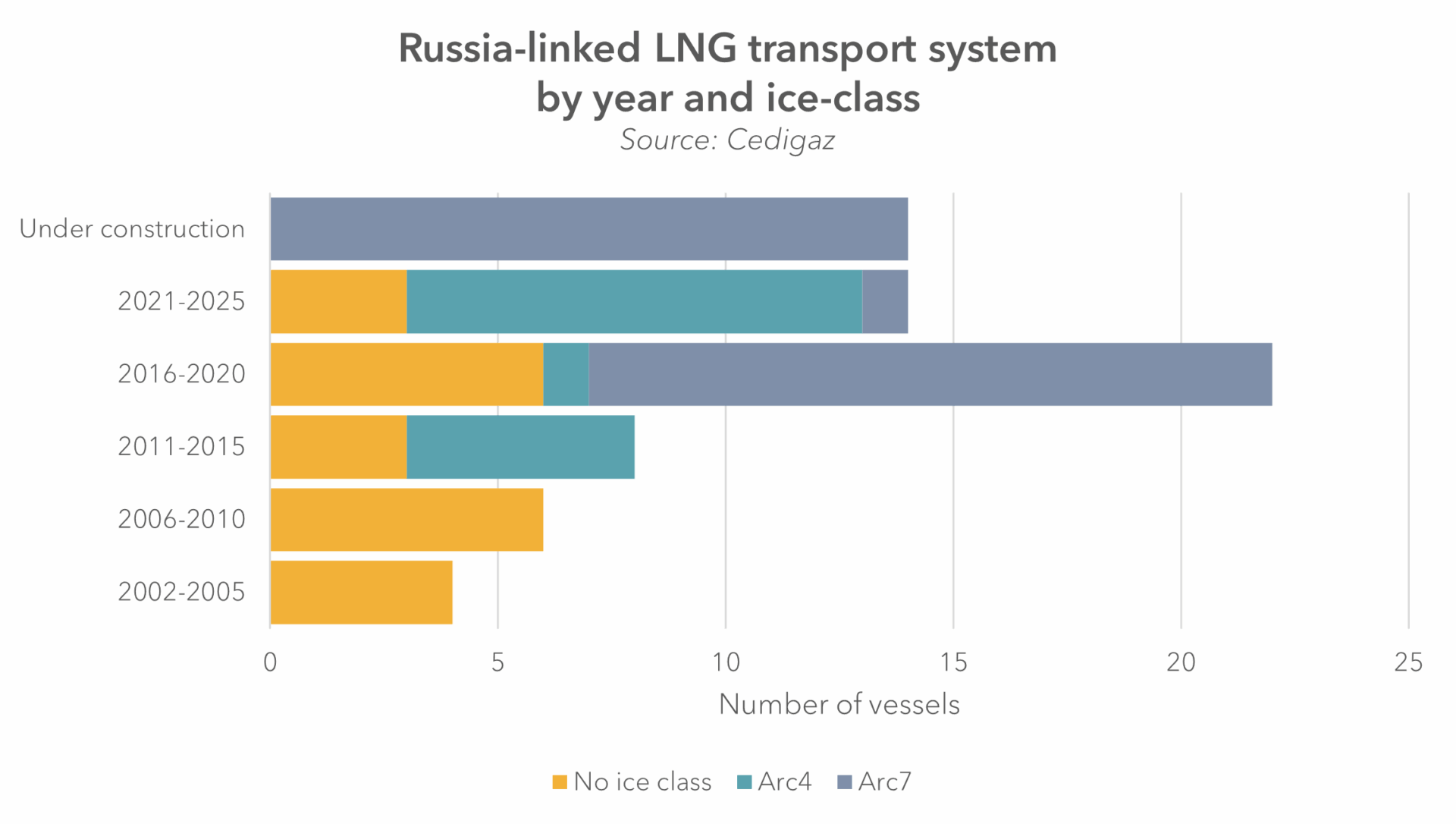

Built year and ice class

The age structure of the fleet is concentrated in the 2013–2020 period, corresponding to the construction of the Arc7 vessels for Yamal LNG and a cohort of modern conventional LNG carriers later integrated into Arctic-linked logistics. A secondary layer consists of early-2000s vessels acquired on the secondary market, providing supplementary lift capacity.

The age structure of the fleet is concentrated in the 2013–2020 period, corresponding to the construction of the Arc7 vessels for Yamal LNG and a cohort of modern conventional LNG carriers later integrated into Arctic-linked logistics. A secondary layer consists of early-2000s vessels acquired on the secondary market, providing supplementary lift capacity.

The most recent additions – vessels delivered in 2023–2024 and those currently under construction – demonstrate continued fleet development.

The ice-class composition of the fleet shows that Russian LNG shipping is structurally Arctic-oriented. A significant share of operational vessels are classed Arc7 or Arc4, with conventional non-ice-class carriers representing only one segment of the overall system.

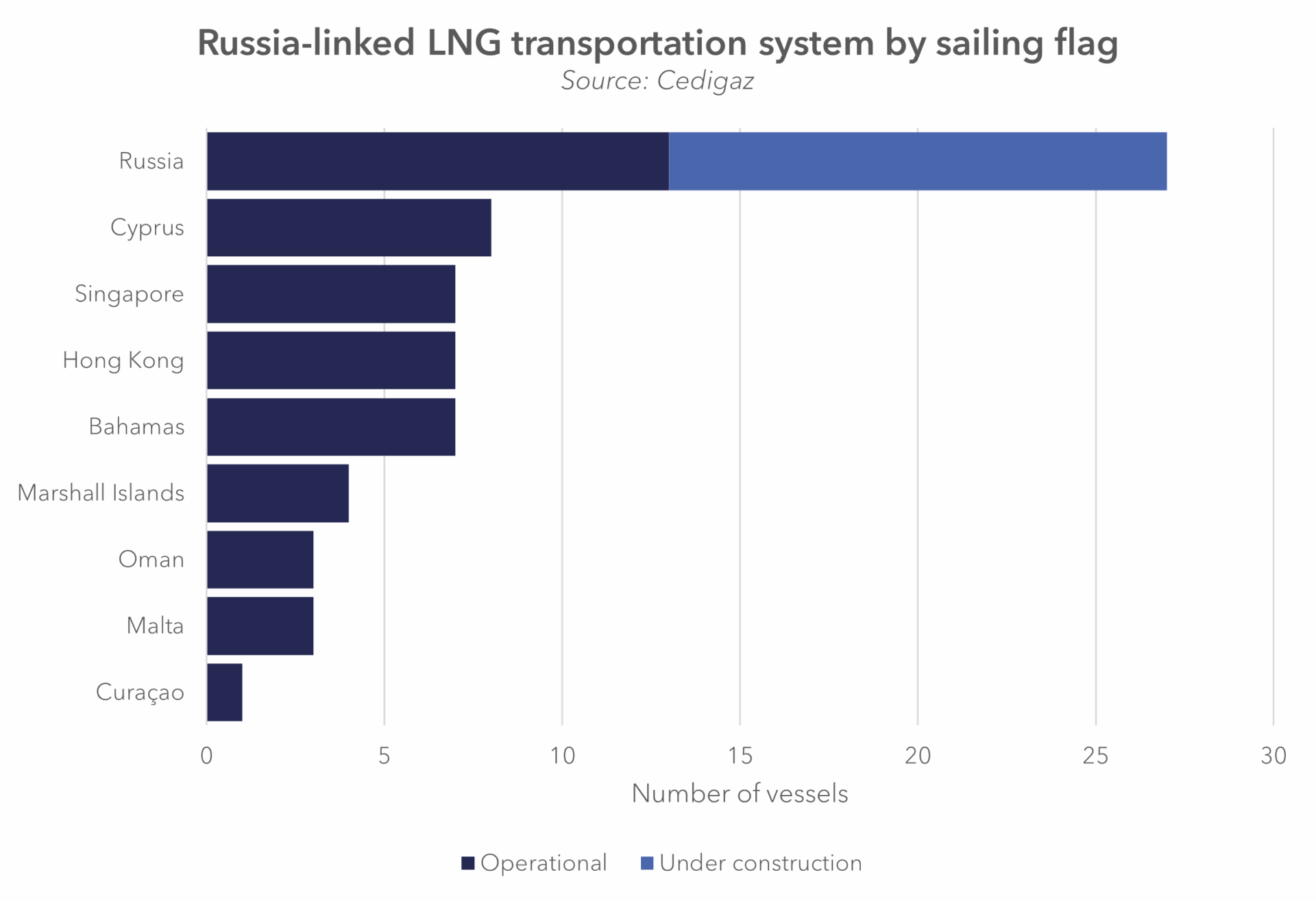

Sailing flag

While Russia represents the largest single registry, a significant share of vessels continues to sail under Cyprus, Bahamas, Hong Kong, Singapore, Marshall Islands, Malta and Oman flags. This dispersion mirrors the historically international structure of LNG shipping and the contractual legacy of long-term charter arrangements.

It is also worth mentioning that 2024 saw a visible wave of registry repositioning. A group of vessels – Arctic Vostok, Arctic Metagaz, Arctic Pioneer, Arctic Mulan and Portovyy – transitioned through intermediary flags, often Liberia and Palau, before re-registering in Russia. However, the vessels operate openly under their current flags and retain traceable name histories.

A similar pattern can be observed in the Oman-flagged Valera and Perle, which followed a sequential registry pathway from Liberia through Gabon, Barbados and Comoros before settling under Oman. These vessels also remain commercially active and identifiable.

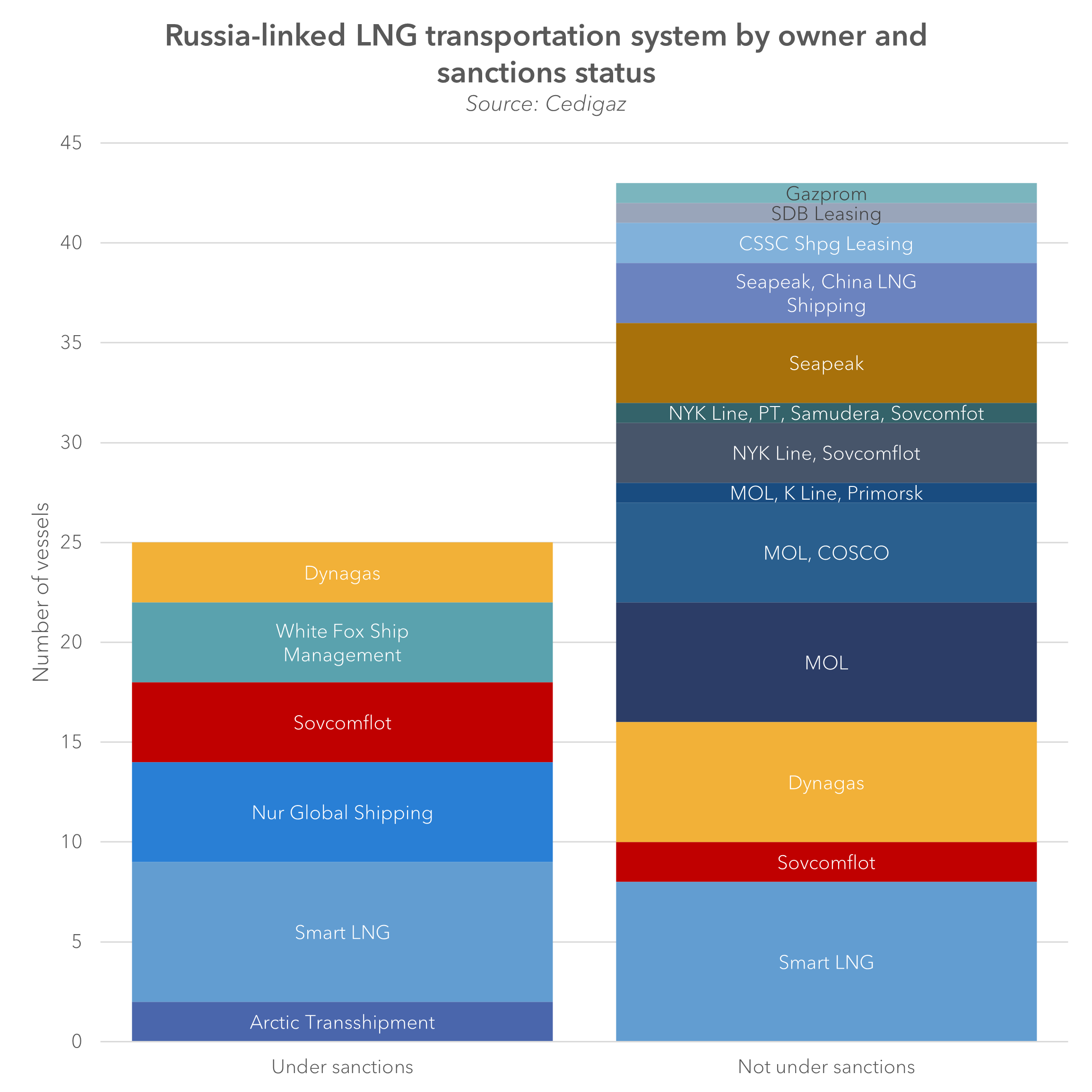

Owner and sanctions status

Vessels currently under sanctions are concentrated among a limited number of ownership platforms, notably Smart LNG (Arc7 newbuild programme at Zvezda Shipyard), Nur Global Shipping (the Dubai-linked conventional cluster), Sovcomflot, White Fox Ship Management and Dynagas. By contrast, the non-designated segment is more fragmented and includes a broader mix of international joint-venture structures and Asian shipping companies such as MOL, MOL/COSCO, NYK Line (including co-ownership configurations), Seapeak (including Seapeak/China LNG Shipping), CSSC Shipping Leasing, as well as smaller leasing entities. Sanctions exposure is not evenly distributed across the fleet and is concentrated in specific ownership clusters directly linked to Arctic projects or sanctions-adaptive restructuring, while a substantial portion of the conventional and joint-venture fleet remains operational outside formal designation regimes.

The ownership and sanctions status will be discussed in more detail in Part 2.

Preliminary conclusions

The dataset does not reveal a coherent LNG “shadow fleet” comparable to the oil sector. Instead, the structure that emerges is a sanctions-adaptive fleet architecture built around:

- a core of purpose-built Arctic ice-class carriers,

- registry repositioning in response to sanctions pressure,

- selective ownership restructuring,

- and continued reliance on internationally structured LNG tonnage.

Russian LNG shipping appears characterised by structural adaptation within the constraints of sanctions and Arctic logistics.