By Irina Mironova for Cedigaz

Australia remains one of the world’s largest LNG exporters and one of the earliest large-scale LNG success stories in the Asia-Pacific region. The country strengthened its export position through a wave of liquefaction projects commissioned between 2015 and 2019, including GLNG, Australia Pacific LNG, Gorgon, Wheatstone, Ichthys and Prelude.

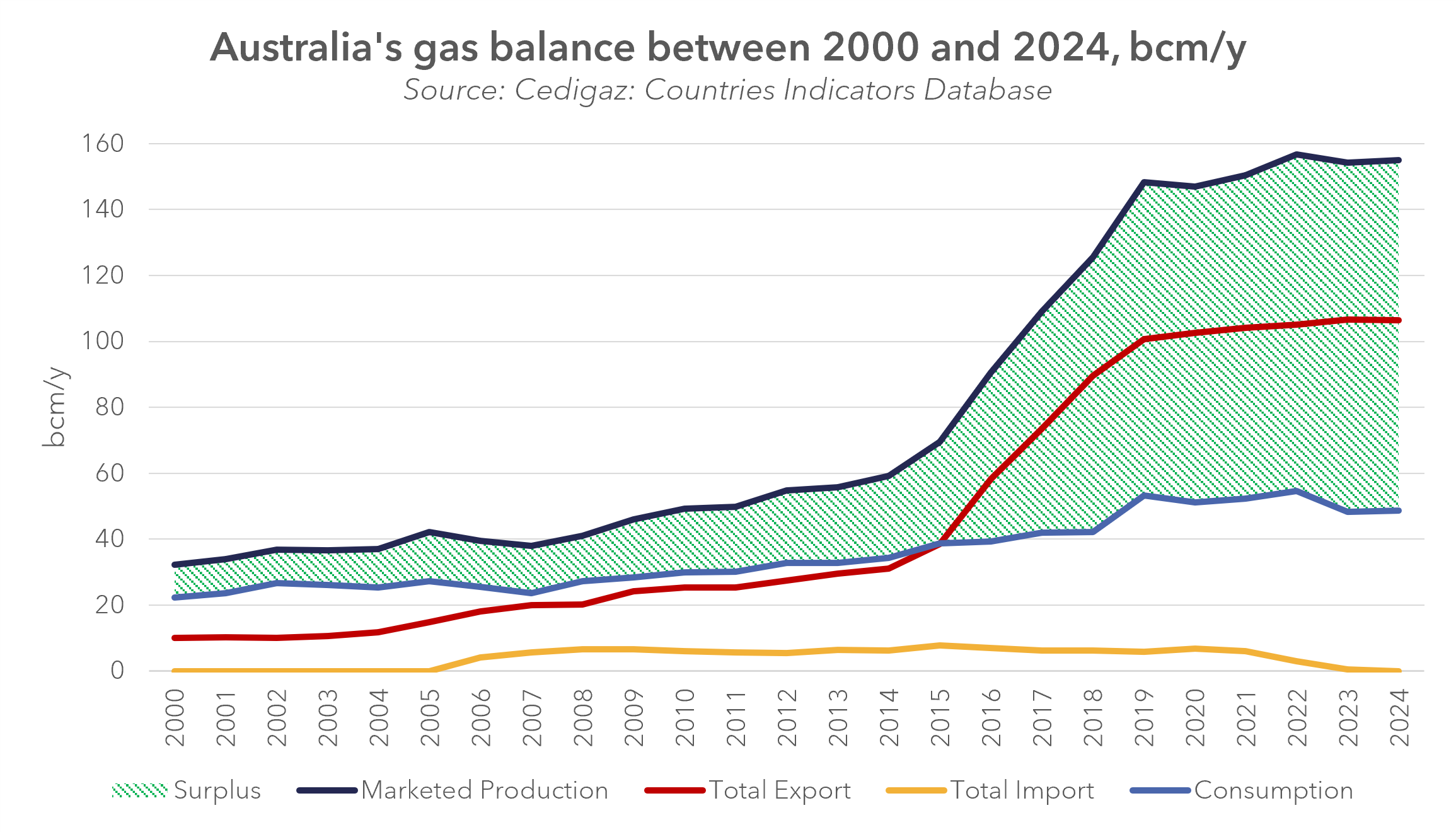

As a result, Australian gas exports rapidly expanded and surpassed domestic gas consumption from 2015 onward. By 2019, total exports had reached around 100 bcm/y and have broadly remained at plateau levels since then. Marketed gas production stabilised at around 150 bcm/y, while domestic consumption remained comparatively flat.

Australia is a structurally export-oriented gas producer with a persistent surplus available for international markets. The Australian case illustrates both the scale that LNG development can achieve and the structural tensions that emerge once the industry matures.

Infrastructure overview

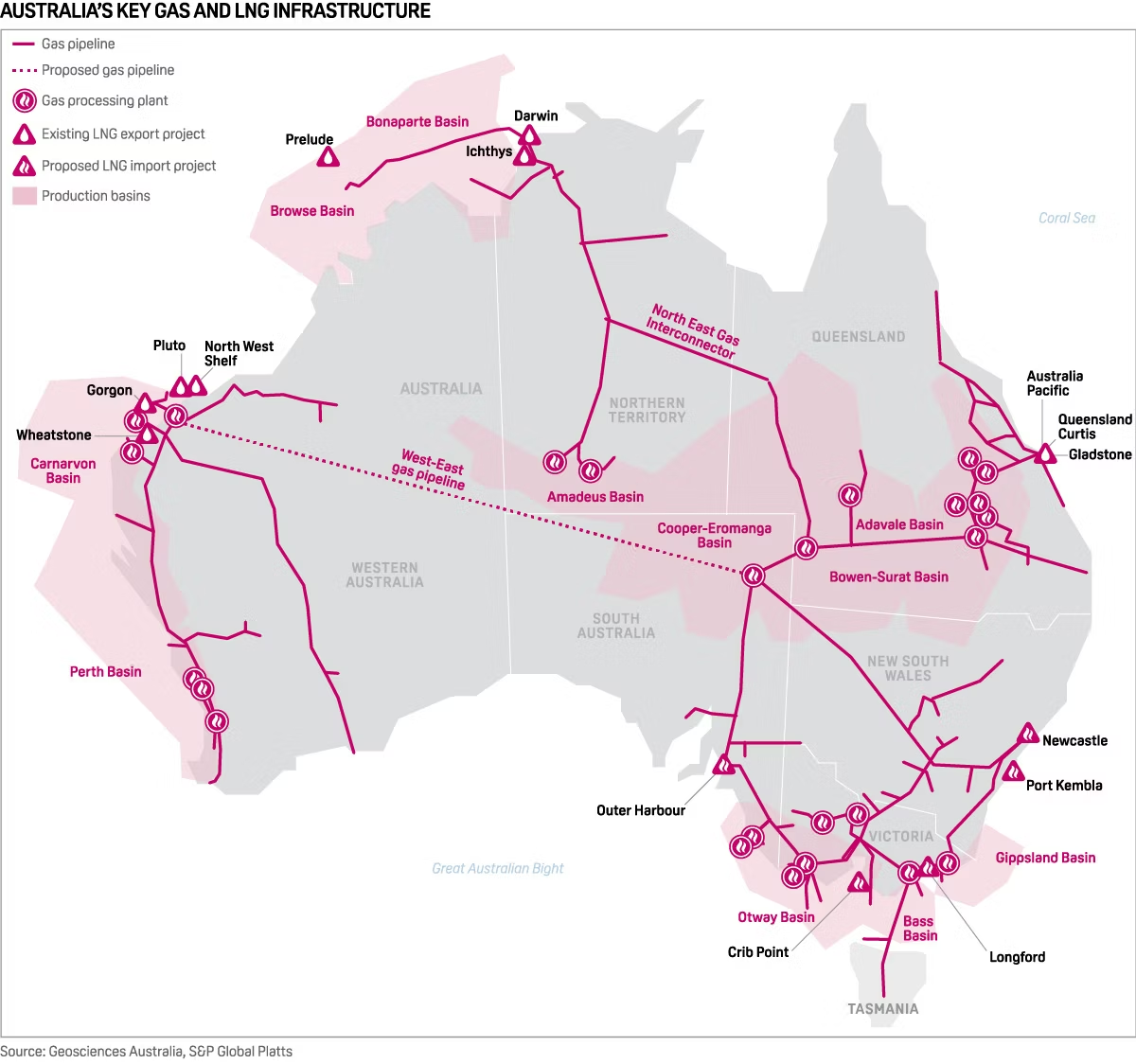

Australia’s LNG infrastructure is geographically dispersed and highly export-oriented. Operational liquefaction capacity is concentrated primarily in Western Australia and the Northern Territory, while major demand centres are located on the eastern seaboard.

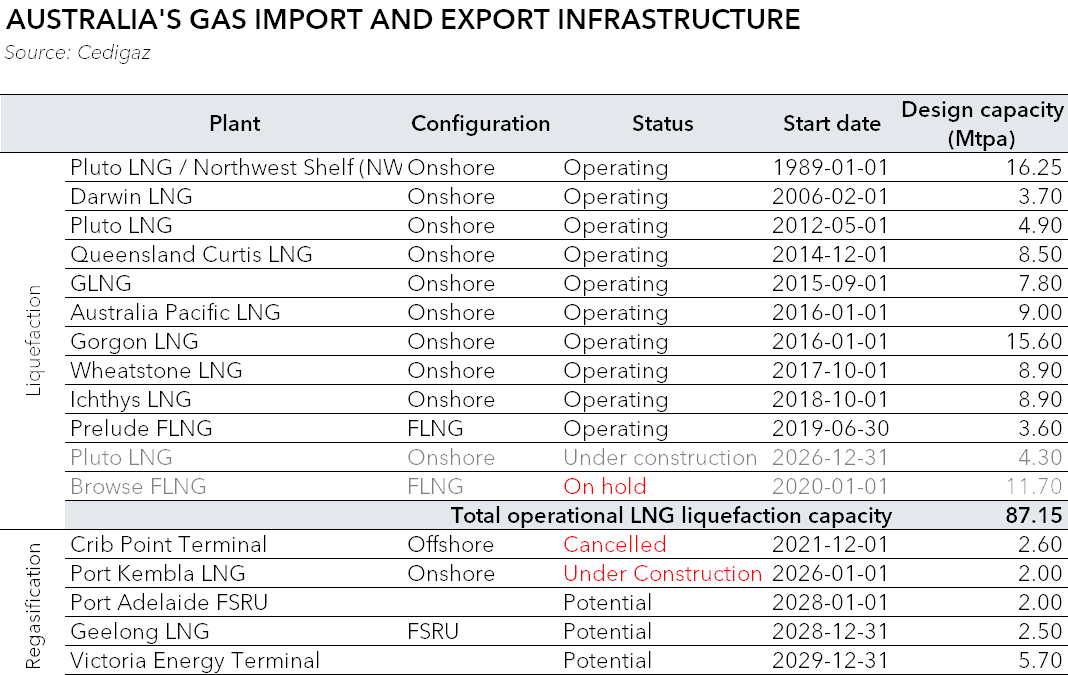

The country currently operates ten liquefaction plants with total operational capacity exceeding 87 Mtpa according to the Cedigaz infrastructure database. The development of upstream gas resources over the past decade was primarily driven by LNG export demand rather than domestic consumption growth.

The Australian gas system is not fully integrated on a national basis. Western and eastern gas markets operate largely separately, with limited pipeline connectivity between them. As a result, gas shortages or supply tightness in eastern Australia cannot easily be compensated by western upstream production.

This structural fragmentation explains the growing interest in LNG import infrastructure within Australia itself. Several regasification terminal projects have been proposed in the eastern part of the country, while one terminal is currently under construction according to the Cedigaz infrastructure database.

Maintaining export capacity increasingly depends on upstream replacement and backfill developments. In 2026, Woodside continued advancing the Browse project as a long-term feedgas source for the North West Shelf system. The proposed development is intended to sustain LNG exports from the Karratha plant as production from legacy offshore fields gradually declines.

There is also growing domestic political pressure to prioritise local gas supply. In 2026, debates around a proposed domestic gas reservation framework raised concerns among producers and Asian buyers regarding the long-term reliability of Australian export commitments.

LNG export contract structure overview

Australia’s LNG exports are extensively covered by long-term SPAs. According to the Cedigaz LNG Supply Contracts Database, Japan remains the largest contracted destination for Australian LNG with 25.7 Mtpa of active contracted volumes, followed by China with 16.8 Mtpa. A significant share of contracts is also associated with unspecified destinations (9 Mtpa). Other contracted buyers include South Korea, Malaysia, Taiwan and India. Excluding the unspecified category, all contractual destinations are located within the Asia-Pacific region.

A key feature distinguishing Australia’s LNG contract structure from that of Qatar is the predominance of FOB-based contracts. 58% of Australia’s active SPA portfolio is contracted on an FOB basis, while around one-third remains DES. This creates substantially greater flexibility for buyers, as FOB offtakers can redirect cargoes depending on market conditions, arbitrage opportunities and portfolio optimisation strategies. By contrast, Qatar’s contract portfolio remains predominantly DES-oriented.

Exports dynamics in 2026

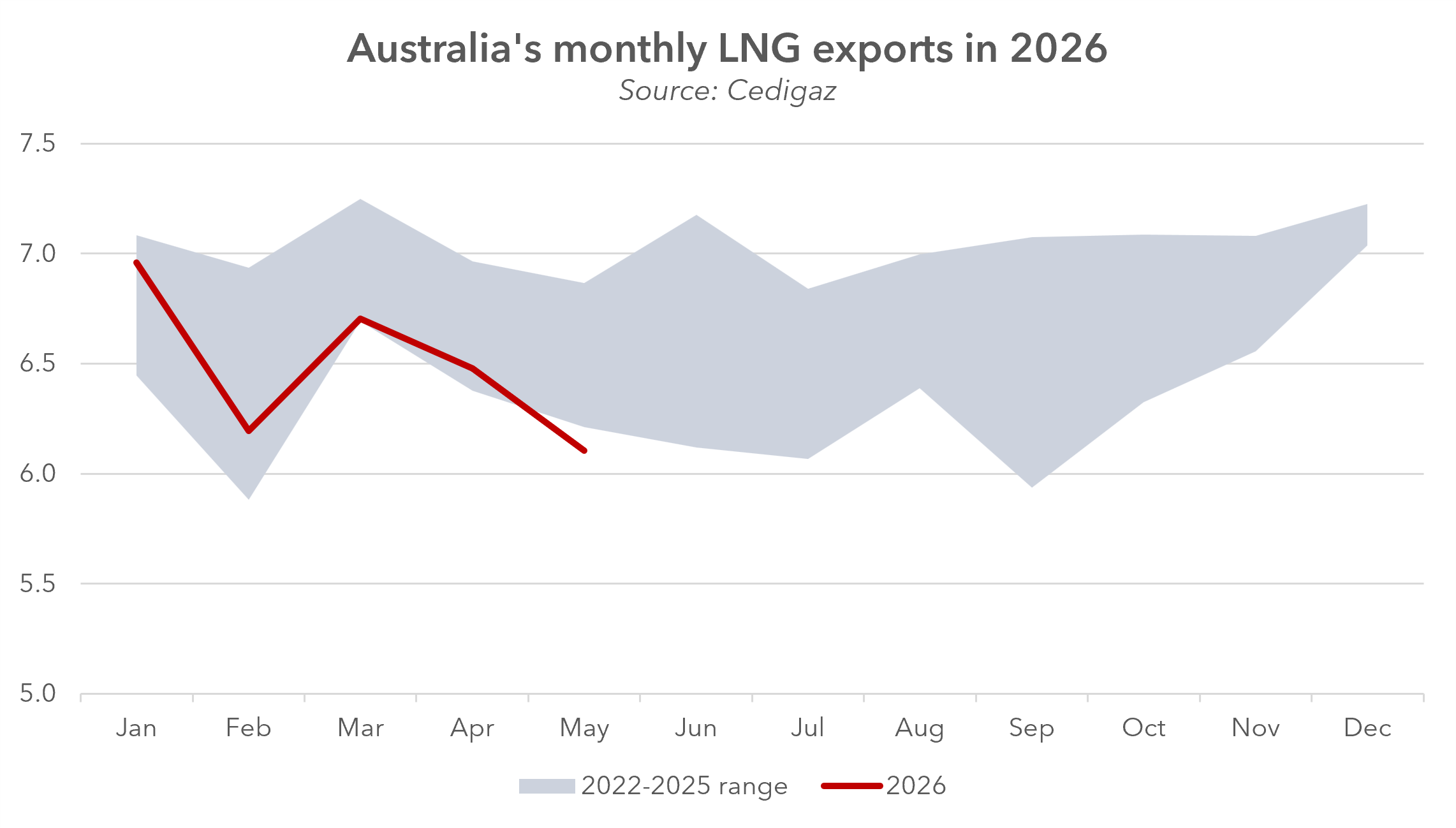

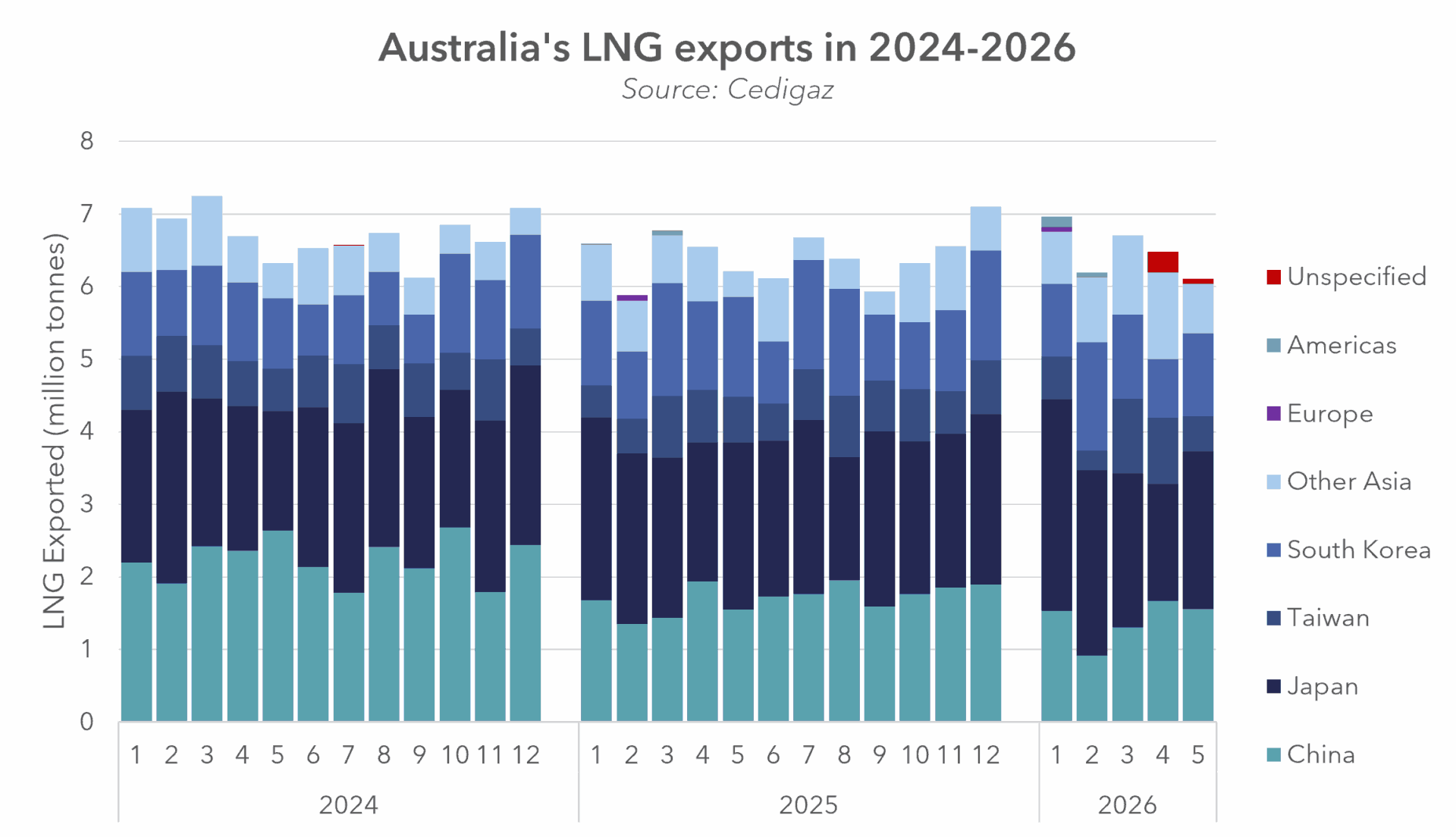

Several Asian buyers exposed to Qatari supply constraints during the Middle East disruption of 2026 – particularly China, South Korea, Taiwan and India – are among the established buyers of Australian LNG. Australia thus appeared to be one of the most likely suppliers capable of partially compensating for reduced Qatari LNG availability in the Asia-Pacific region. However, export performance during the first five months of 2026 demonstrated the limitations of mature LNG systems operating close to plateau production levels. There is no room to increase significantly the exported volumes.

Australian LNG exports remained broadly within the historical export corridor observed during 2022–2025 and by March–April moved toward the lower side of that range. Weather-related disruptions played an important role, with several facilities affected by cyclone and typhoon activity during the first half of March. Australian LNG exports in May 2026 fell below the range observed in 2022–2025, approaching levels last seen in 2021, when several export facilities were simultaneously affected by maintenance and operational disruptions.

Japan, traditionally the largest destination for Australian LNG, fell to second place in April as China imported more Australian cargoes during the month. Another notable feature was the increase in cargoes directed toward unspecified destinations in April 2026, although May flows returned to a more regular destination pattern.

What does the Australia case tell us about challenges standing before the LNG industry today?

1. Upstream gas availability

Large-scale liquefaction infrastructure ultimately depends on continuous upstream resource replacement. Mature LNG systems require new offshore developments and backfill projects to maintain utilisation rates and avoid gradual decline in export capacity. Feed gas is an issue for several major exporters including Algeria, Nigeria, Indonesia, and others.

2. Domestic supply security versus export priorities

Australia demonstrates the tensions that can emerge between export-oriented LNG development and domestic gas market stability. Even major gas exporters can face regional shortages and infrastructure bottlenecks when domestic and export systems evolve unevenly.

These tensions intensified further in 2026 after the Australian government advanced a draft domestic gas reservation framework aimed at increasing supply to the domestic market. The proposal raised concerns among LNG producers regarding investment incentives, future upstream development and the reliability of Australian LNG exports. Industry representatives warned that forcing LNG exporters to divert a share of export volumes into the domestic market could undermine long-term investment signals and create uncertainty for Asian buyers dependent on Australian LNG supply, including Japan, South Korea, Malaysia and Singapore.

3. Climate change and hazardous weather events

The weather-related disruptions observed during early 2026 illustrate the growing operational risks associated with climate change. Cyclones, typhoons and extreme weather events increasingly affect LNG infrastructure, shipping logistics and upstream operations.

Environmental and legal scrutiny of LNG developments also continued to intensify. In May 2026, Australia’s Federal Court allowed a UN special rapporteur to make submissions in a case challenging the 40-year extension of Woodside’s North West Shelf LNG license.

4. Labour-related disruptions and social constraints

In late May 2026, labour-related disruption risks re-emerged in Australia. Strike activity and planned industrial action affected workers at Woodside’s North West Shelf and Pluto LNG facilities as well as Inpex’s Ichthys LNG project.

Sources

This blog uses data from Cedigaz databases (available to subscribers):

- Country Indicators

- Infrastructure: Liquefaction plants; Liquefaction trains; Regasification plants

- Trade: Monthly LNG – Bilateral flows

- Supply contracts: LNG