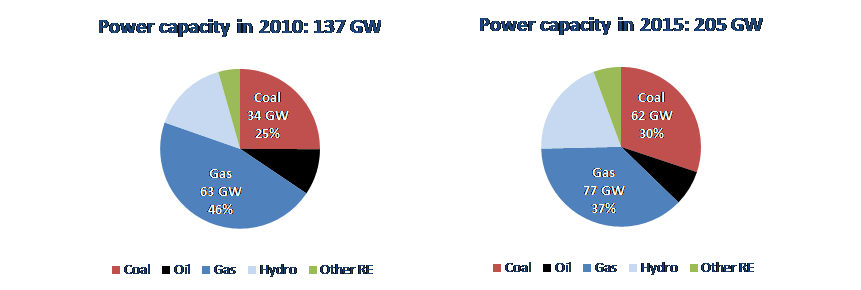

Today, Southeast Asia is again in front of great changes in its energy mix. To meet surging demand, the region must secure a reliable and affordable energy supply. It must also limit the environmental pressures associated with energy consumption. The power sector is fundamental to these changes. Driven by rapid economic growth, demographic and urbanization trends, and the extension of access to modern electricity to larger segments of rural populations, electricity demand is expected to almost triple by 2040.  While natural gas still dominates the regional electricity mix, a shift to coal has been observed since the end of the 2000s driven by the availability of coal in the region and its lower cost than competing fuels. In the short to medium term, this trend is going to continue: there are around 35 GW of coal-based capacity under construction in the region, most of them to be completed by 2020. In addition, there is a huge number of permitted and announced coal-fired power plants in the pipeline, which means that the dominance of coal may continue well after 2020. In the World Energy Outlook 2016 of the International Energy Agency (New Policies Scenario), coal becomes the first source of electricity generation by 2040, despite the increase in electricity generation from renewables. In contrast, the contribution of gas to electricity generation falls by 2040.

While natural gas still dominates the regional electricity mix, a shift to coal has been observed since the end of the 2000s driven by the availability of coal in the region and its lower cost than competing fuels. In the short to medium term, this trend is going to continue: there are around 35 GW of coal-based capacity under construction in the region, most of them to be completed by 2020. In addition, there is a huge number of permitted and announced coal-fired power plants in the pipeline, which means that the dominance of coal may continue well after 2020. In the World Energy Outlook 2016 of the International Energy Agency (New Policies Scenario), coal becomes the first source of electricity generation by 2040, despite the increase in electricity generation from renewables. In contrast, the contribution of gas to electricity generation falls by 2040.

Country Report - Page 6

Latest developments of the Egyptian gas industry

Egyptian marketed natural gas production has been steadily declining since 2009, as a result of the depletion of offshore mature gas fields and delays in new offshore developments (West Nile Delta), exacerbated by the political unrest. This downturn accelerated in 2013 (- 6%) and even further in 2014 (- 14%). In 2015, marketed production is estimated down 8.9% to 44.5 bcm, according to Cedigaz provisional estimates.

In a context of production shortfall, natural gas consumption declined from 52 bcm in 2013 to 48 bcm in 2014. In 2015, natural gas consumption stabilized despite the production decline as Egypt started importing gas after soaring power demand forced it to halt LNG exports.

Storm warning in the U.S. oil & gas sector

The new CEDIGAZ report, U.S. Natural Gas Update and Outlook*, analyzes the consequences of the oil price decline on the U.S. oil and gas sector as well as the implications for production and hydrocarbon prices.

The oil price decline has left American producers in a situation like that of 2009 following the collapse of the Henry Hub gas prices. At the time, shale gas production was growing fast but demand was depressed due to the effects of the subprime mortgage crisis. Producers reacted by redirecting their investments towards liquid-rich deposits (containing oil or natural gas liquids) and were thus able to benefit from the oil price recovery. This strategic reorientation did not penalize gas production, which continued to grow, thanks to the gases associated with oil production which, in recent years, have been responsible for almost all growth in gas production. Today, more than 50% of the shale gas produced in the United States comes from liquid-rich deposits. Consequently, any decrease in liquids production occurring in reaction to falling oil prices is bound to have major repercussions on domestic gas production.