The 2014 edition of CEDIGAZ’s flagship survey Natural Gas in the World highlights some disturbing signs of weakness on the demand and supply sides, indicating structural challenges that will need to be addressed before a golden age of gas can occur.

In 2013, growth in worldwide gas demand decelerated, up by only 1% versus 2.4% in 2012. This is less than the 3% growth achieved by coal and, most remarkably, less than that of oil (1.4%). Moreover, gas was the only fossil fuel to record lower growth in 2013 than in 2012. This phenomenon may be observed even in Asia – a powerhouse in terms of growth in gas demand – where demand rose 4% in 2013, down from 6% one year earlier. Gas demand had already shown its limitations in 2012, when it gained only 2.4%, compared to an average growth of 2.8% per year in the previous decade.

CEDIGAZ, the International Center for Natural Gas Information, has released today the updated version of its Worlwide Underground Gas Storage (UGS) database. According to Cedigaz, worldwide working gas capacity stood at 399 bcm at January 1, 2014, a 5% growth over the previous year. Salt caverns represented 8% of working gas capacities worldwide and 26% of daily withdrawal capacity, they were the fastest growing segment of the market, with a 10% growth rate in 2013 and a 33% share of the planned projects backlog in terms of capacity. In difficult times for storage operators, European capacities grew by almost 3% (+13% for salt caverns).

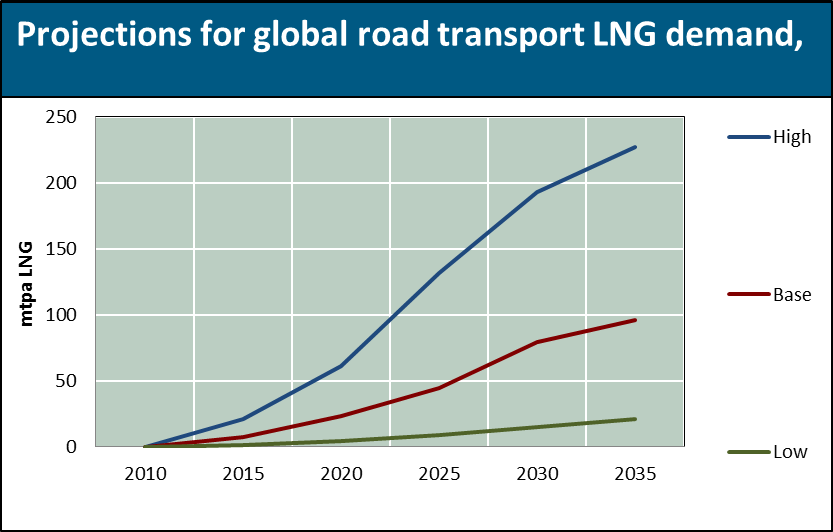

According to a new report by CEDIGAZ, the International Center for Natural Gas Information, LNG as a fuel will capture a significant market share in the transport sector by 2035. The greatest potential is seen in road transport, were annual demand is projected to reach 96 million tons per year (mtpa) in CEDIGAZ’ base scenario while demand in the marine sector could grow to an estimated 77 mtpa. The rail sector could add another 6 mtpa to global demand. However, the development of LNG as a transport fuel faces a number of challenges, and will have to go hand in hand with the development of fuelling infrastructure.

Fuel cost differentials will drive the growth in trucking sector

Use of LNG in land transport will be largely limited to heavy duty vehicles (HDV) and will essentially be driven by the difference between the price of diesel and that of LNG. In contrast with the marine sector, environmental legislation is unlikely to play a major role in triggering the adoption of LNG as a fuel for land transportation, as traditional fuels and technologies will be able to comply with the gradual tightening of emissions standards. However, the cost advantage of LNG relative to diesel currently provides a strong economic incentive in the trucking industry. In its base scenario, CEDIGAZ projects a worldwide demand of 45 mtpa in 2025 growing to 96 mtpa in 2035, with China representing almost half the global market. China has several features that combine to make it a prime candidate for the development of LNG in the road sector. The country has the world’s largest inland goods transport market and has already developed an extensive LNG supply infrastructure, initially as a means of transporting gas from remote fields or to consumers who were not connected to the pipeline supply network. With at least 100,000 LNG vehicles and 1,100 refuelling stations at the end of 2013, China already has a head start over the rest of the world in this nascent market. However, gas price reform in China may slow LNG growth there. LNG should also carve out a significant market share in the US, Europe and the rest of Asia.