For years, discussions about Russia’s LNG future have focused on liquefaction capacity. How many trains could be built? How quickly could new projects come online? Could Russia achieve its ambition of becoming one of the world’s largest LNG exporters?

Today, those questions remain relevant, but they are no longer the most important ones.

Russia’s ability to increase LNG exports is increasingly determined not by liquefaction capacity, but by the logistical and technological constraints that connect liquefaction plants to end-users. In other words, the bottleneck has shifted downstream.

This distinction has become particularly important in 2026. Following the disruption of LNG supplies from the Middle East, global gas markets have become significantly tighter. Under such conditions, the market naturally looks for alternative sources of supply. Russia possesses some of the world’s largest gas resources and substantial LNG capacity, making it an obvious candidate. Yet the amount of LNG that Russia can realistically bring to international markets remains constrained.

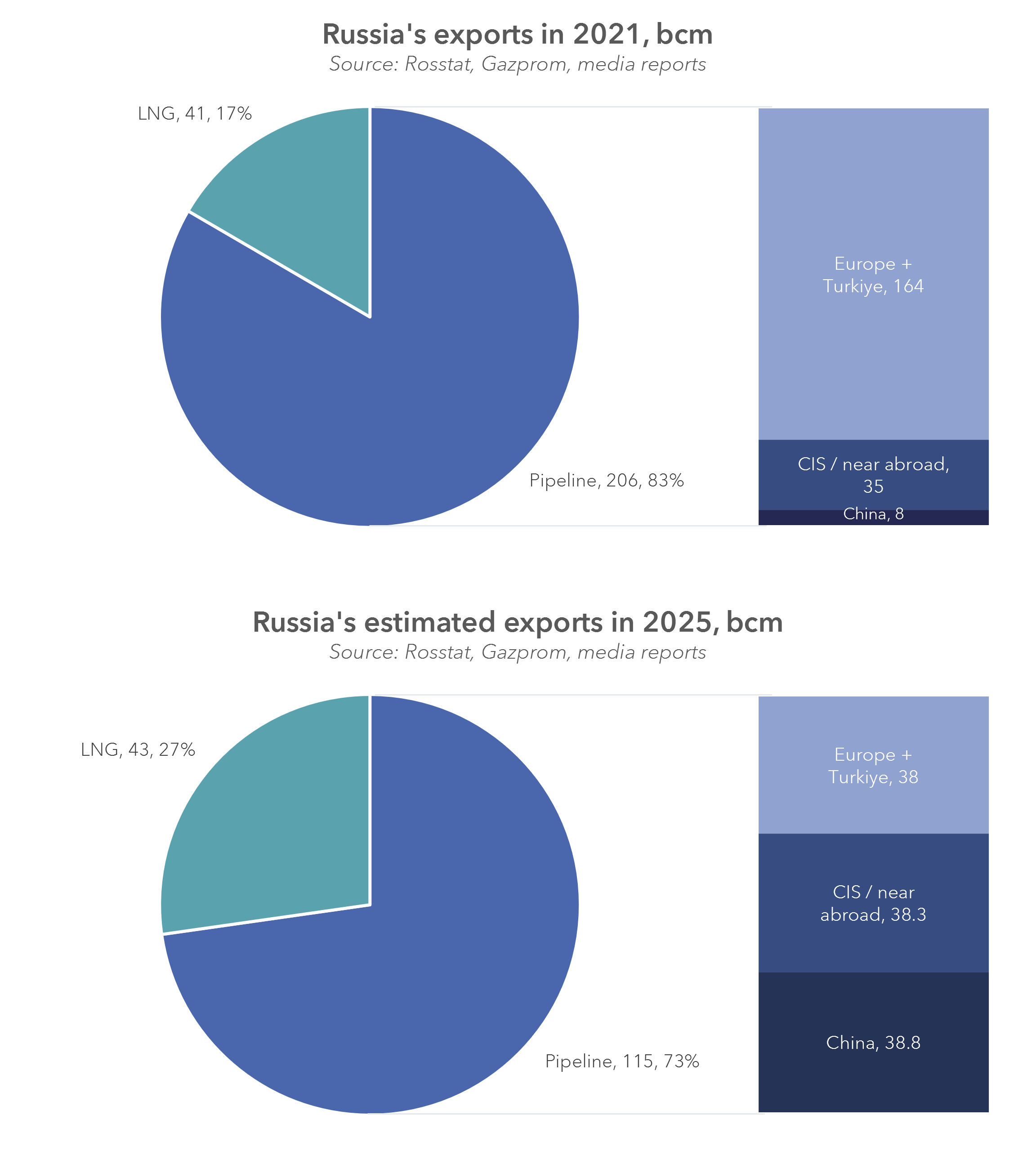

The Russian gas sector has undergone a profound transformation since

2022. Pipeline exports to Europe have collapsed, while exports to China have expanded through the Power of Siberia pipeline.

LNG has become increasingly important within Russia’s export strategy, both as a means of market diversification and as a way to monetise gas resources that can no longer access traditional European markets.

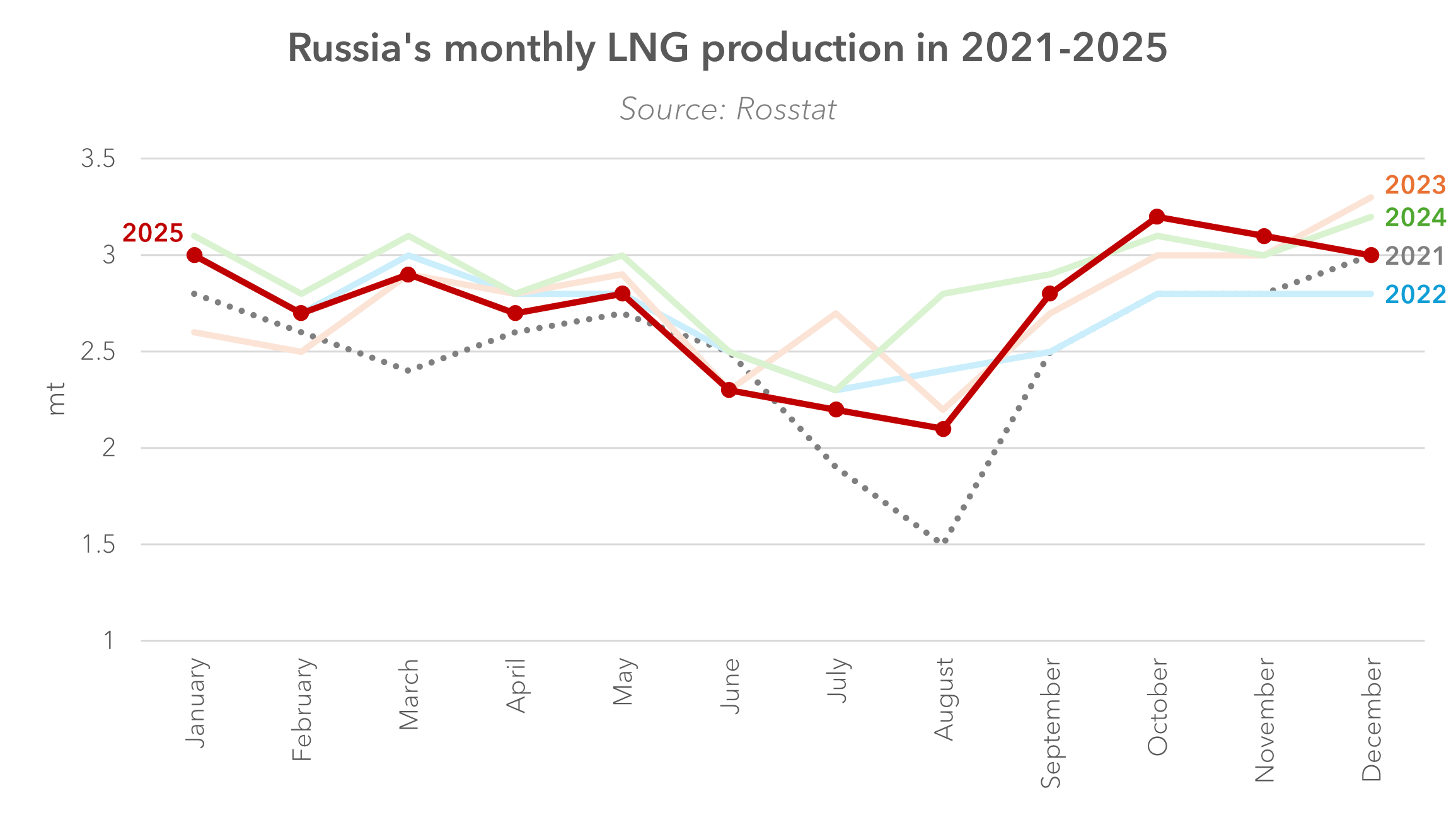

Several large-scale LNG projects remain operational. Yamal LNG continues to perform strongly, regularly producing above its nameplate capacity. Sakhalin-2 remains a reliable source of supply to Asian markets. Arctic LNG 2 has technically started operations but continues to face severe commercial and logistical challenges.

Several large-scale LNG projects remain operational. Yamal LNG continues to perform strongly, regularly producing above its nameplate capacity. Sakhalin-2 remains a reliable source of supply to Asian markets. Arctic LNG 2 has technically started operations but continues to face severe commercial and logistical challenges.

At first glance, Russia appears to possess sufficient liquefaction capacity to increase exports further. However, the practical reality is more complex.

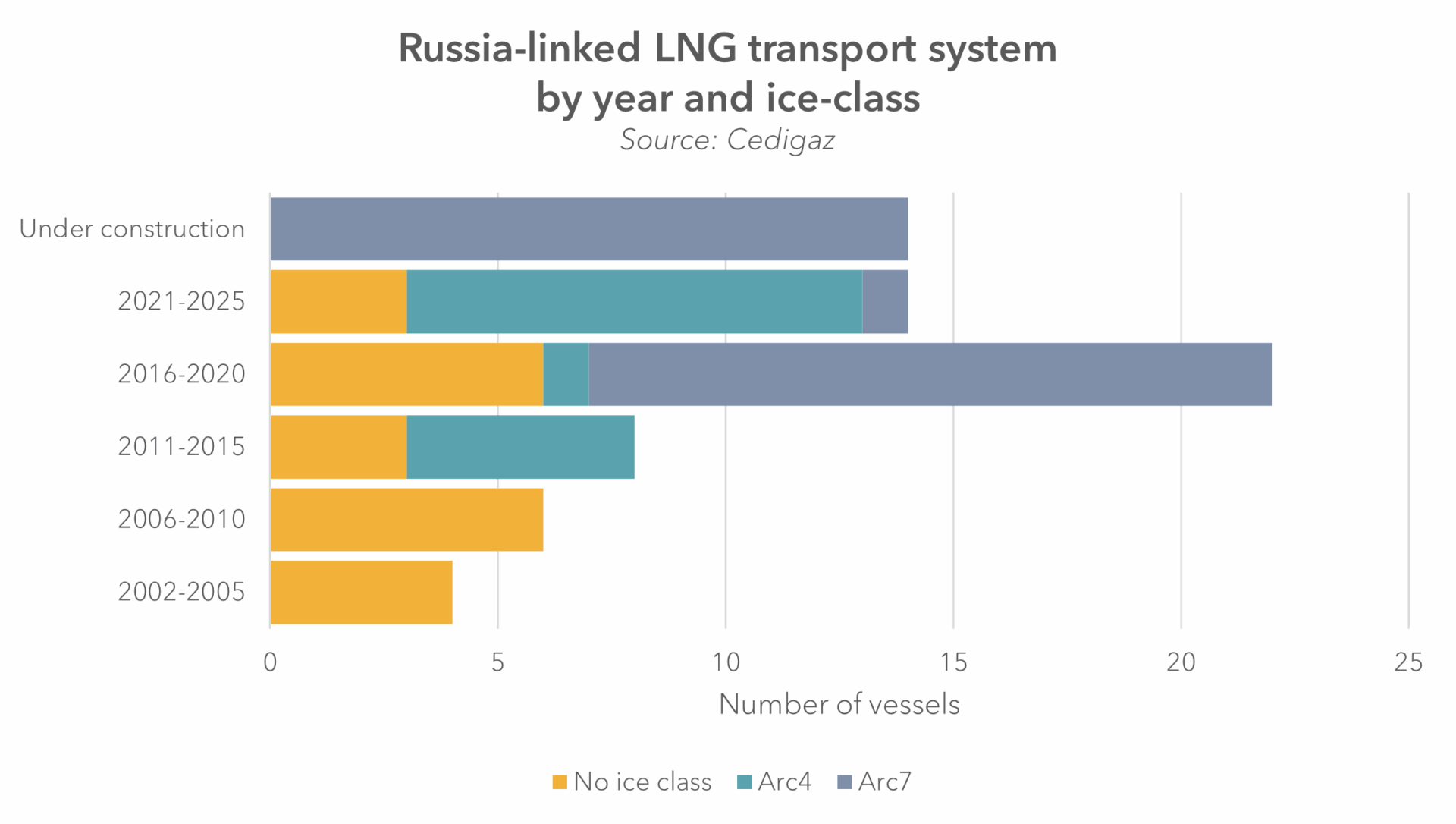

The first constraint is shipping.

Russia’s Arctic LNG projects rely heavily on specialised Arc7 ice-class LNG carriers. These vessels are essential for year-round operations in Arctic conditions. While Russia has expanded its LNG carrier fleet and additional vessels are under construction, fleet growth has not kept pace with project ambitions. The availability of suitable vessels increasingly determines how much LNG can be exported, particularly during winter months.

(For more details, see Cedigaz blog on Russian fleet – part 1, part 2).

The second constraint is logistics.

The second constraint is logistics.

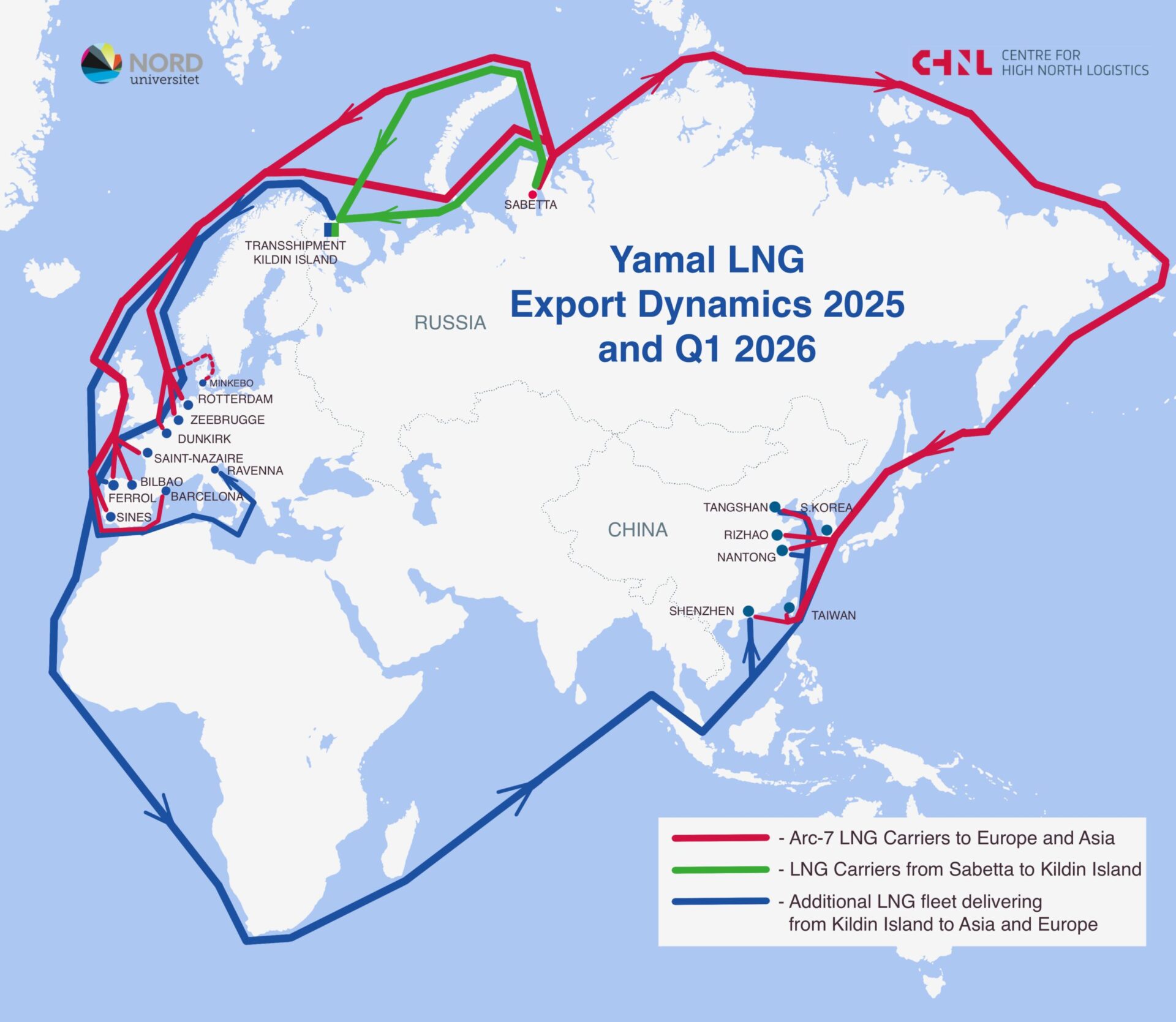

Historically, Russian LNG exports benefited from transshipment operations in European ports. Following restrictions on LNG transshipment services, Russia has been forced to reorganise its logistics around domestic hubs, particularly near Murmansk. This adaptation has allowed exports to continue but has increased complexity and reduced flexibility throughout the system.

Principal scheme of Russian LNG exports via NSR and transshipment facility based on Yamal LNG exports in 2025

Source: Centre for High North Logistics

The Northern Sea Route provides an important seasonal advantage, enabling shorter voyages to Asian markets during summer months. Yet it remains a seasonal corridor rather than a year-round solution. During winter, exports continue to depend on scarce ice-class shipping capacity and transshipment infrastructure.

Technology has also become increasingly important.

Sanctions have complicated access to specialised equipment, large liquefaction turbines, engineering services, and maritime support systems. Existing facilities continue to operate, but the development of new projects faces greater execution risks and longer timelines.

As a result, a growing gap has emerged between Russia’s nominal LNG capacity and its effective export capability.

This distinction matters for the global LNG balance. Market participants often focus on headline liquefaction capacities when assessing future supply. Yet in Russia’s case, installed capacity alone no longer provides a reliable indicator of potential exports.

The practical ability to move LNG molecules from Arctic liquefaction plants to international buyers has become the key determinant of supply.

Several projects could eventually improve Russia’s position. Ust-Luga LNG would provide a major new export outlet in the Baltic region, while Murmansk LNG could reduce dependence on Arctic shipping constraints thanks to its ice-free location. However, both projects face technological, financial, regulatory, and geopolitical uncertainties.

For the period to 2030, Russia’s LNG outlook is therefore likely to be shaped less by resource availability or policy ambitions than by logistics, shipping and infrastructure execution.

In today’s LNG market, the critical question is no longer how much LNG Russia can produce.

It is how much LNG Russia can actually deliver.

New Cedigaz report, Russia and the 2026–2030 LNG Supply: Constraints, Strategic Niches and Scenarios, prepared by Irina Mironova for CEDIGAZ subscribers, spans 50 pages and includes 30+ figures covering Russia’s gas production, LNG logistics, export geography, shipping constraints, and scenario outlooks.