European LNG net imports: + 27.8% year on year in H1 2015

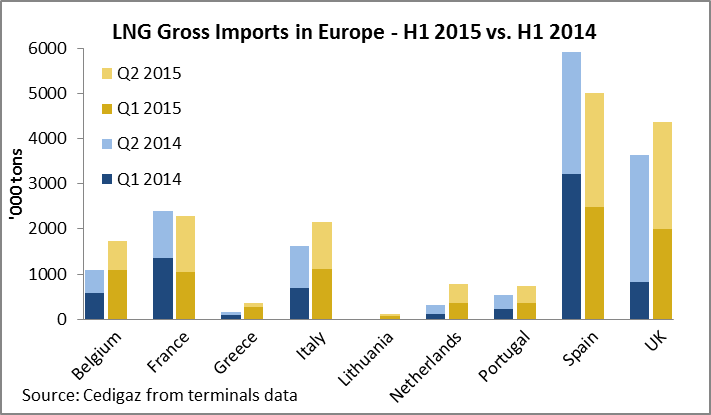

LNG net imports increased significantly to 15.9 million tons in the first half of 2015 against 12.4 million tons in H1 2014 due to more deliveries and less reloads. Gross imports showed a two-digit growth rate or even more in all countries but France and Spain – where they decreased by 5% and 15.3% respectively – thanks to the capacity of liquid markets of Northwest Europe to absorb the LNG left available by Asian buyers. Overall, gross imports grew by 11.9%, mostly driven by imports in Belgium, the Netherlands and the United Kingdom. Together, these three countries received 6.88 million tons of LNG in H1 2015 against 5.04 million tons in H1 2014 (+36.7%), mostly from Qatar. The latter, which is diverting flexible LNG from Asia, exported 9.8 million tons of LNG to Europe in H1 2015 against 7.85 million tons in H1 2014 (+24.9%).

LNG net imports increased significantly to 15.9 million tons in the first half of 2015 against 12.4 million tons in H1 2014 due to more deliveries and less reloads. Gross imports showed a two-digit growth rate or even more in all countries but France and Spain – where they decreased by 5% and 15.3% respectively – thanks to the capacity of liquid markets of Northwest Europe to absorb the LNG left available by Asian buyers. Overall, gross imports grew by 11.9%, mostly driven by imports in Belgium, the Netherlands and the United Kingdom. Together, these three countries received 6.88 million tons of LNG in H1 2015 against 5.04 million tons in H1 2014 (+36.7%), mostly from Qatar. The latter, which is diverting flexible LNG from Asia, exported 9.8 million tons of LNG to Europe in H1 2015 against 7.85 million tons in H1 2014 (+24.9%).