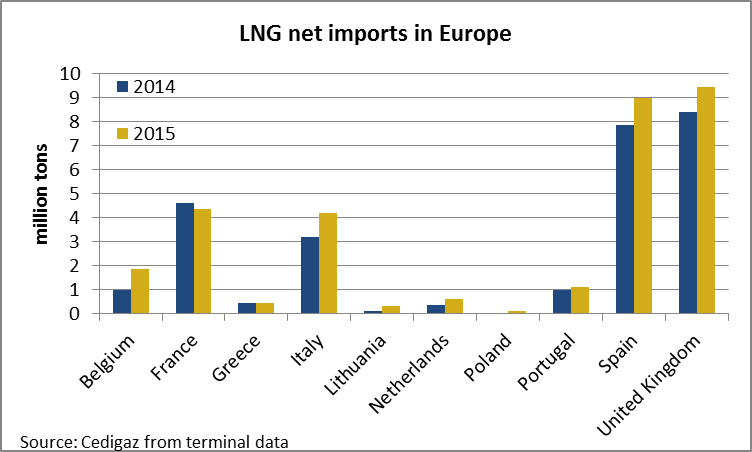

According to Cedigaz’ First Estimates, LNG imports grew by 2.1% in 2015 to 241.2 Mt. Main highlights include the reversal of growth trends in Asia and in Europe, the emerging role of the MENA countries as LNG importers and the growth of intraregional and intra-basin trade due to the convergence of global prices.

Change in growth trends in Asia and Europe

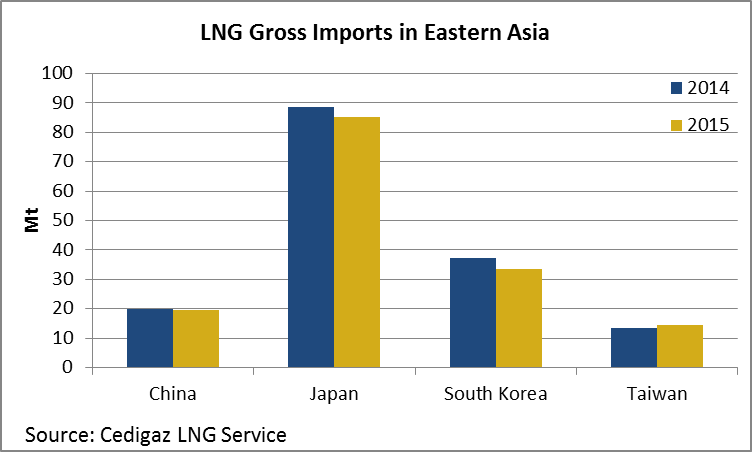

After many years of growing demand in Asia and declining demand in Europe, trends changed on the two largest LNG markets in 2015. For the first time since 2009, Asian LNG net imports declined by 2.8% to 172.8 Mt (-5Mt) mainly because of weather related factors, gas-fuel competiveness and the slowdown of economic growth. The bulk of the decline came from Japan and South Korea, the two biggest importers in the world: in these two countries, LNG net imports declined respectively to 85 Mt and 33.4 Mt which represents a combined decline of 7.2 Mt (-5.8 %). In a context of slowing economic growth and poor gas price competitiveness, Chinese demand dwindled by 0.9% to 19.7 Mt while LNG imports grew at an average annual rate of 20.1% from 2010 to 2014. Rising imports in Thailand (+ 1.3 Mt to 2.6 Mt) and Taiwan (+1.1 Mt to 14.6 Mt), as well as the beginning of imports in Pakistan (above 1 Mt) did not suffice to offset the regional decline.