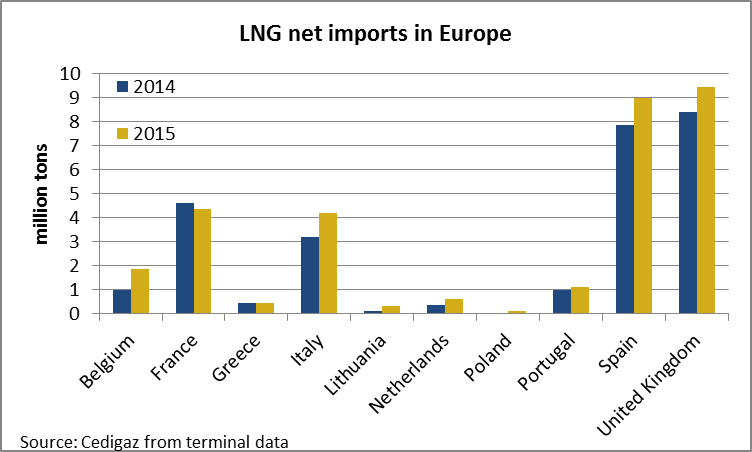

In 2015, LNG net imports grew by 16.6% in Europe as demand for natural gas grew in the region. As a consequence of more deliveries (+1.8 Mt) and less reloads (-2.68 Mt), net imports increased by 4.47 Mt up to 31.35 Mt. Except in France, where gross imports decreased from 5.07 Mt to 4.77 Mt while re-expors slightly decreased (-0.03 Mt), and in Greece, where imports were flat at around 0.45 Mt, net imports increased everywhere because of various factors.

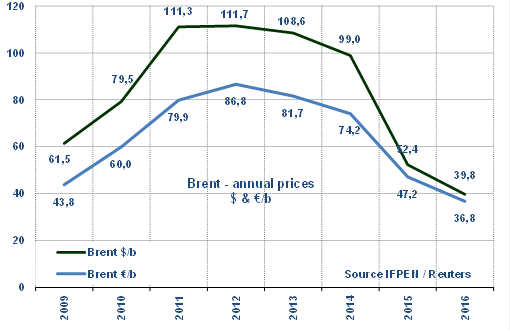

The Brent averaged $52/b in 2015, down 47% compared to 2014 ($99/b). The very disturbed geopolitical context had little impact on prices, apart from concerns arising early in the year after Saudi Arabia and its allies intervened militarily in Yemen, starting on March 26. All in all, excess supply defined the price which, after August, stayed below $50 and fell to $38 in December. Downward price pressures were due to the continued OPEC policy in favor of defending market share and the fact that U.S. production only registered a small decrease. Price forecasts for 2016, based on the futures markets, have been in the $40-60/b range since August 2015. Prices will be influenced by the following key factors:1/ the actual rate of economic growth, potentially “disappointing and uneven” according to the IMF; 2/ Iranian exports, likely to rise by at least 0.5 Mb/d; 3/ how far U.S. production falls as a result of reduced drilling activity; 4/ the effects of the decrease in upstream investment; 5/ whether OPEC policy – unchanged since year-end 2014 – changes or not; 6/ the influence on production of growing regional tensions in the Middle East. Looking at the supply-demand balance alone, the market could start to rebalance at the end of 2016, which could gradually put pressure on prices.

Prices for 2016 mainly reflect changes in forward prices and can not be considered as forecasts. Economic, climatic or geopolitical context may in particular greatly impact future trends.

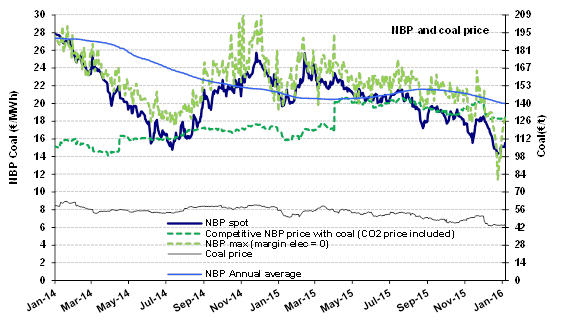

The NBP rose to €18.5/MWh ($5.7/MBtu) at end November, but could not withstand various downward pressures, including that of mild December temperatures. The 9.2°C average reported by the “Met Office” in the U.K. broke the 1934 record of 6.9°C. As a result, the level of demand was relatively low, about 200 mcmd compared to 250 mcmd under average weather conditions. In reaction, the December NBP price slipped to €16/MWh ($5.1/MBtu), down 7% in one month. The first January quotations are in the vicinity of €15/MWh ($4.9/MBtu), equivalent to the prices reported in July 2014.

In 2015, LNG net imports grew by 16.6% in Europe as demand for natural gas grew in the region. As a consequence of more deliveries (+1.8 Mt) and less reloads (-2.68 Mt), net imports increased by 4.47 Mt up to 31.35 Mt. Except in France, where gross imports decreased from 5.07 Mt to 4.77 Mt while re-expors slightly decreased (-0.03 Mt), and in Greece, where imports were flat at around 0.45 Mt, net imports increased everywhere because of various factors.

In 2015, LNG net imports grew by 16.6% in Europe as demand for natural gas grew in the region. As a consequence of more deliveries (+1.8 Mt) and less reloads (-2.68 Mt), net imports increased by 4.47 Mt up to 31.35 Mt. Except in France, where gross imports decreased from 5.07 Mt to 4.77 Mt while re-expors slightly decreased (-0.03 Mt), and in Greece, where imports were flat at around 0.45 Mt, net imports increased everywhere because of various factors.