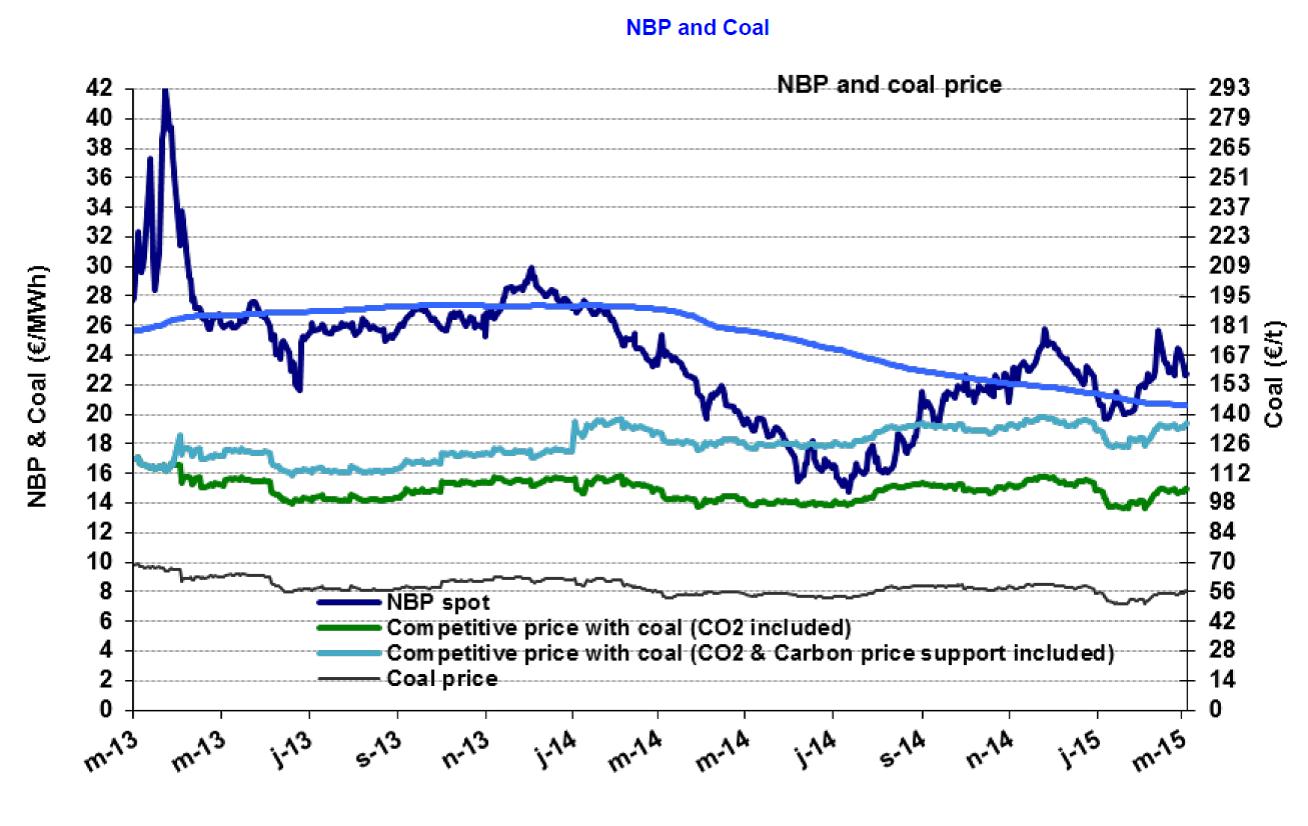

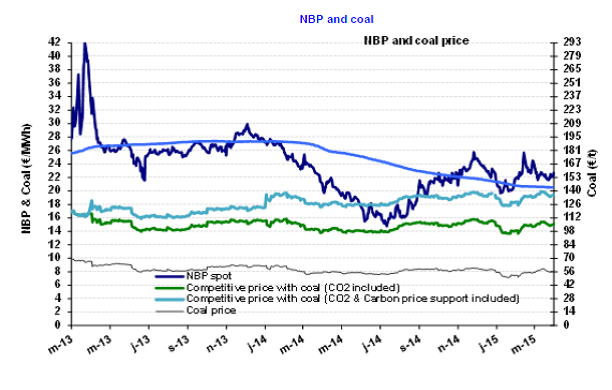

NBP: Long-term and spot prices converging in 2015?

The NBP price averaged €22.3 /MWh ($7.1/MBtu) in March, down 4.5% over February. The average for winter 2014-15 was roughly the same (€22.5/MWh), lower by 16% than that of the previous winter. So concerns over supply (Russia versus Ukraine, uncertainty over Groningue, the storage capacity at Rought) have not had a structural effect on prices.

The NBP price averaged €22.3 /MWh ($7.1/MBtu) in March, down 4.5% over February. The average for winter 2014-15 was roughly the same (€22.5/MWh), lower by 16% than that of the previous winter. So concerns over supply (Russia versus Ukraine, uncertainty over Groningue, the storage capacity at Rought) have not had a structural effect on prices.

In upcoming months, the market is anticipating an average price of €21.5/MWh ($6.7/MBtu) for next summer and €24/MWh ($7.6/MBtu) for next winter. Based on the current forecasts, these levels are moving towards convergence with the prices of oil-indexed contracts. If the trend persists and convergence occurs, this would represent a break with the situation observed since 2009. Between 2009 and 2014, the indexed prices served as a ceiling for the NBP, whose prices were systematically lower.